August 25, 2025

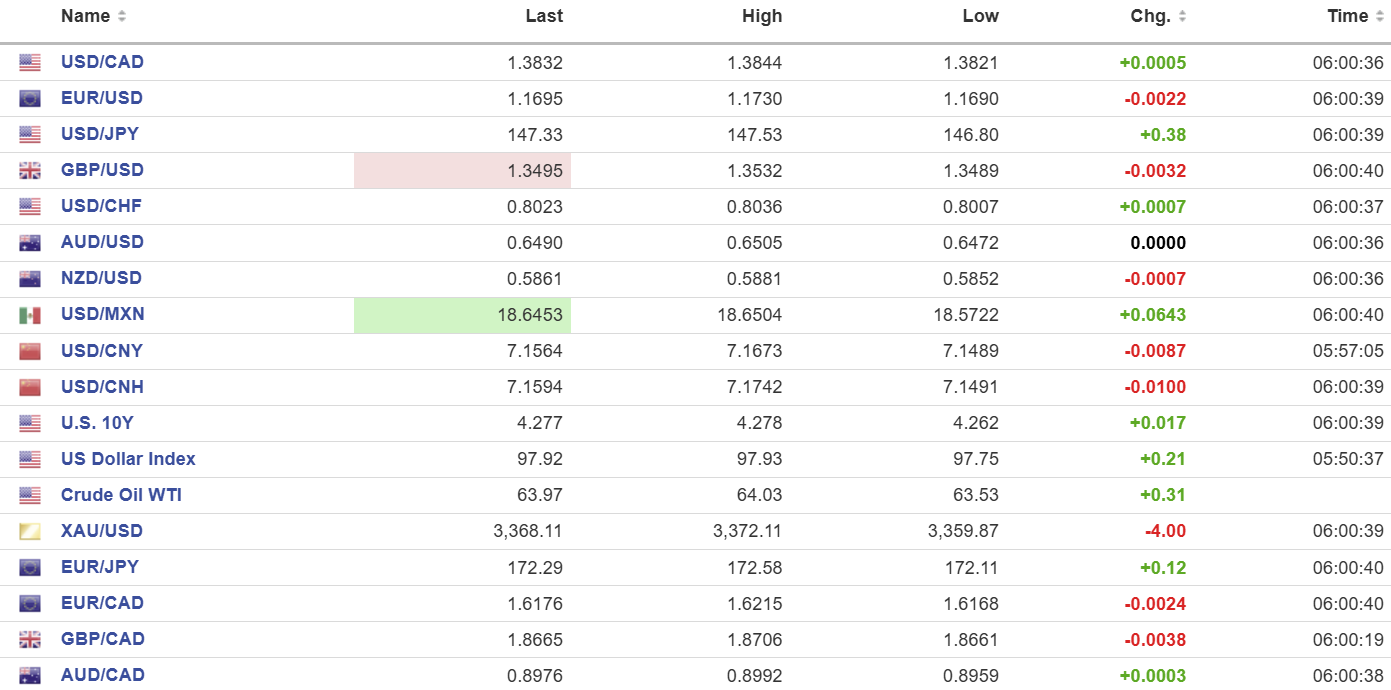

USDCAD open 1.3832, overnight range 1.3818-1.3844, close 1.3829

USDCAD was on the verge of breaking higher when Fed Chair Jerome Powell flipped from hawkish to dovish. Instead of fearing an inflation spiral from Trump’s tariffs, he now believes that what inflation is caused by tariffs will be “short-lived.” The US dollar plunged and USDCAD dropped in sympathy.

Prime Minister Mark Carney announced Friday that effective September 1, he would remove retaliatory tariffs on US imports not covered by the Canada US Mexico Agreement on trade (CUSMA). Canada’s counter-tariffs on US aluminum and steel will remain. The move is viewed as an “olive branch” to Trump in hopes of jumpstarting trade talks.

WTI oil prices climbed in a 63.53-64.19 range, and they are at the top of that band in NY. Ongoing concerns about supply disruptions from Russia due to sanctions and Ukraine attacks on oil infrastructure combined with broad US dollar weakness are supporting gains.

Today’s US data—Chicago Fed National Activity Index, New Home Sales, and Dallas Fed Manufacturing Index—will be a non-event.

It is also the last week of summer before the school year kicks off, and many market participants are on holiday.

USDCAD Technical Outlook:

The intraday technicals turned bearish Friday with the move below 1.3902 then 1.3850 and are looking for a decisive break below 1.3815 to extend losses to test the 100-day moving average at 1.3780

The medium-term picture is bullish. A series of higher lows stretching back to the end of July and slowly strengthening momentum indicators are pointing toward a retest of 1.3950 as long as support at 1.3750 holds.

For today, USDCAD support is 1.3805 and 1.3780. Resistance is 1.3860 and 1.3890. Today’s Range: 1.3780-1.3880

Powell Blinks and Greenback Sinks

Fed Chair Powell appears to have “blinked” in the face of Trump’s relentless campaign of insults and slurs that were meant to embarrass the Fed chair into cutting rates. Mr. Powell used his keynote speech at Jackson Hole to pivot from leaving rates unchanged due to tariff-fueled inflation risks to saying the base case was for inflation to have “relatively short-lived” impacts. That comment sank the US dollar and drove the 10-year Treasury yield down from 4.342% pre-speech to 4.242% post-speech. Equities soared and gold rallied.

Taking Stock

Asian equity markets did not seem very enthusiastic except for China’s which rallied hard. Japan’s Topix closed with a gain of 0.15% while Australia’s ASX 200 was flat. Hong Kong’s Hang Seng rose 1.94%.

As of 5:20 am PDT, European bourses are in negative territory. The French CAC-40 Index is down by 0.73% and the German DAX has lost 0.25%. The UK FTSE 100 is closed. S&P 500 futures have lost 0.32% while the US 10-year Treasury yield is at 4.287%. Gold (XAUUSD) is 3370.02 and the US Dollar Index (DXY) is 97.91

EURUSD

EURUSD spiked higher Friday and is sitting near the bottom of its 1.1685-1.1730 overnight range. Prices peaked after German Ifo business climate improved modestly, rising to 89.0 from 88.6 in July. The current situation was weaker, suggesting that Germany’s economic recovery remains weak. ECB policymaker Ollie Rehn said that “inflation is for now in a good place. Any insurance cut just for its own sake wouldn’t be necessary.”

GBPUSD

GBPUSD traded in a 1.3484-1.3532 range but the gains failed to overcome resistance at 1.3600 which has contained all rallies since July 23. Broad US dollar weakness and concerns of a slower pace to BoE rate cuts may limit the downside in the near term. UK markets were closed today.

USDJPY

USDJPY is trading in a 146.80-147.53 range, after plunging from 148.78 Friday. The losses were fueled by Powell’s pivot towards cutting US rates coupled with BoJ Governor Kazuo Ueda’s suggestion of BoJ rate hikes this year. Ueda said wages are rising and labour shortages are a pressing “economic issue,” which analysts say means rate hikes this year.

AUDUSD

AUDUSD traded sideways in a 0.6472-0.6505 range after rallying from 0.6415 on Friday. Traders are looking to the release of the RBA minutes from the August 12 meeting for further insight into the interest rate outlook. Analysts expect the RBA to be more aggressive with rate cuts for the rest of the year.

USDMXN

USDMXN plunged after the Powell pivot, and prices are at the top of its 18.5722-18.6474 overnight range. USDMXN remains underpinned by yield differentials favouring Mexico over the US and by speculation that Banxico takes a slower pace to rate cuts.

USDCNY

PBoC fix: 7.1161 vs exp. 7.1551 (Prev. 7.1321)

Shanghai Shenzhen CSI 300 rose 2.08% to 4469.22

The shift back into stocks from deposit accounts by households and institutional accounts continued to drive stocks higher. Optimism increased after the Powell pivoit in Jackson Hole.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics