September 2, 2025

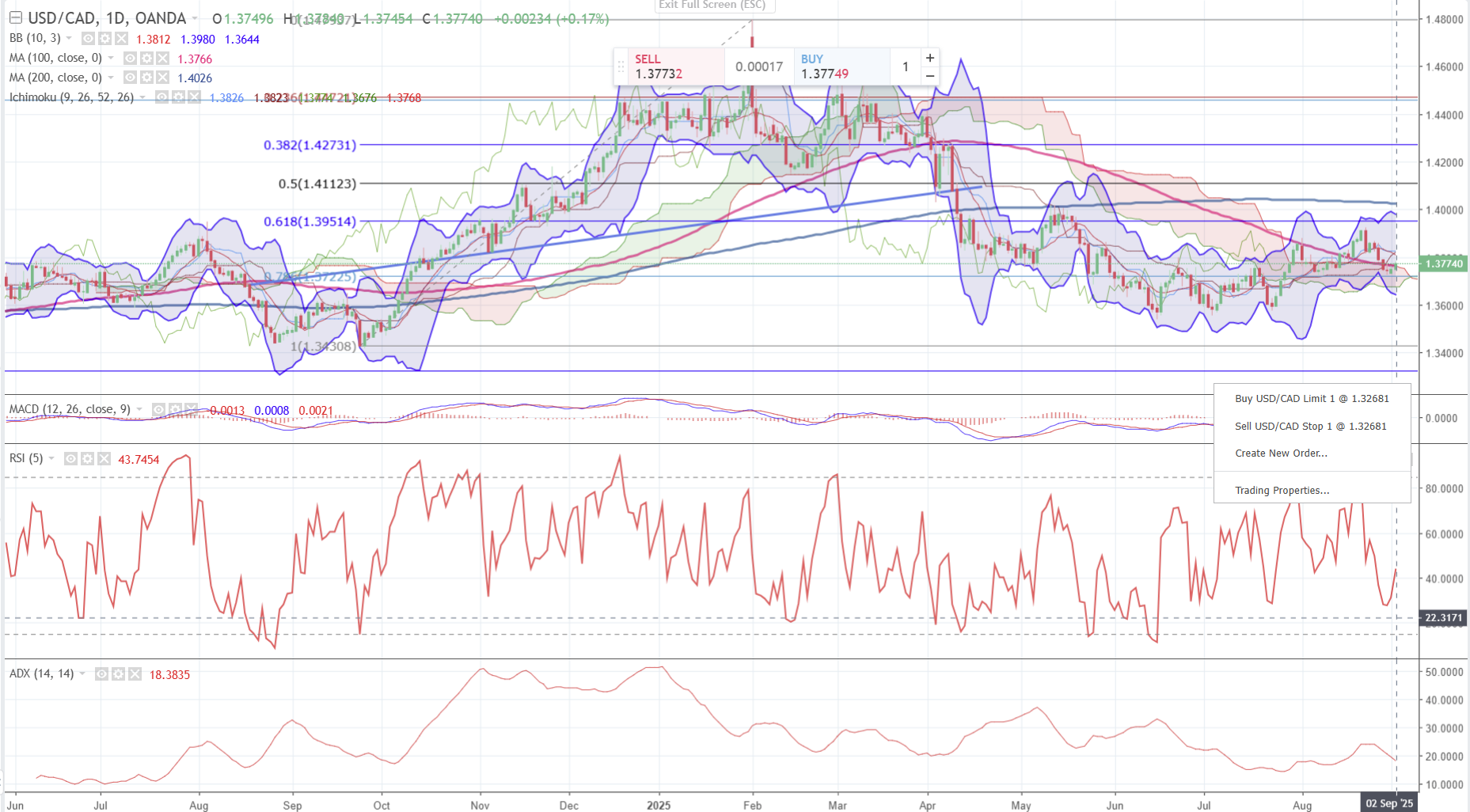

USDCAD open 1.3776, overnight range 1.3728-1.3796, Aug. 29 close, 1.3749

USDCAD is feeling perky to start September as a mix of broad US dollar strength an weak domestic data underpin prices. Friday’s Canadian GDP data showed how the country is coping with US tariffs, and it is not pretty. GDP shrank 1.2% y/y mainly due to a 27% plunge in exports in Q2.

The slowing economic growth will likely force the Bank of Canada to cut rates by 25 bps to 2.5% on September 17. The outlook for lower Canadian rates caused CAD/US 10-year yield spreads to widen to from -85.1 on Friday to -90.1 this morning.

WTI rallied from 63.63 to 65.93 with prices bolstered by news that Ukraine drone strikes knocked 1.1 million b/d or Russian crude off-line. Fears of additional targeted energy infrastructure attacks are supporting prices. Meanwhile India reaped a $12.6 billion windfall from buying discounted Russian crude.

Gold prices surged to another record rising to 3508.54 before dropping to 3477.61 on profit-taking. The gold rally is fueled by the prospect of rapidly falling US rates.

USDCAD Technical Outlook:

The intraday technicals are modestly bullish above 1.3740 and bumping up against a week-long downtrend line at 1.3790. A topside break targets 1.3850 while a failure suggests a test of support at 1.3721.

The medium-term picture is bearish below 1.3810 which is guarding Fibonacci resistance at 1.3950. A decisive break then close below 1.3730 would target 1.3640.

For today, USDCAD support is 1.3740 and 1.3710. Resistance is 1.3790 and 1.3820. Today’s Range: 1.3730-1.3820

It’s Embarrassing

The US Court of Appeals in Washington ruled that Trump exceeded his authority by using emergency legislation, specifically the Emergency Economic Powers Act, to impose sweeping tariffs on imports in a 7-4 ruling. Then the judges kicked the can down the road and gave the White House until October 14 to appeal the ruling. The judges ignored Treasury Secretary Bessent, warning that declaring the tariffs illegal would cause “dangerous, diplomatic embarrassment.”

NFP Looms Over Today’s Data

US ISM Manufacturing PMI along with ISM prices paid, employment, and new orders components are due today. The Manufacturing PMI will likely show a negative impact from Trump’s tariffs while a weak employment index will support calls for a Fed rate cut, which is widely expected.

Taking Stock

Asian equity indexes were uninspired to start the month and finished on a mixed note today. Japan’s TOPIX closed 0.61% higher while Hong Kong’s Hang Seng lost 0.47% and Australia’s ASX 200 fell by 0.30%.

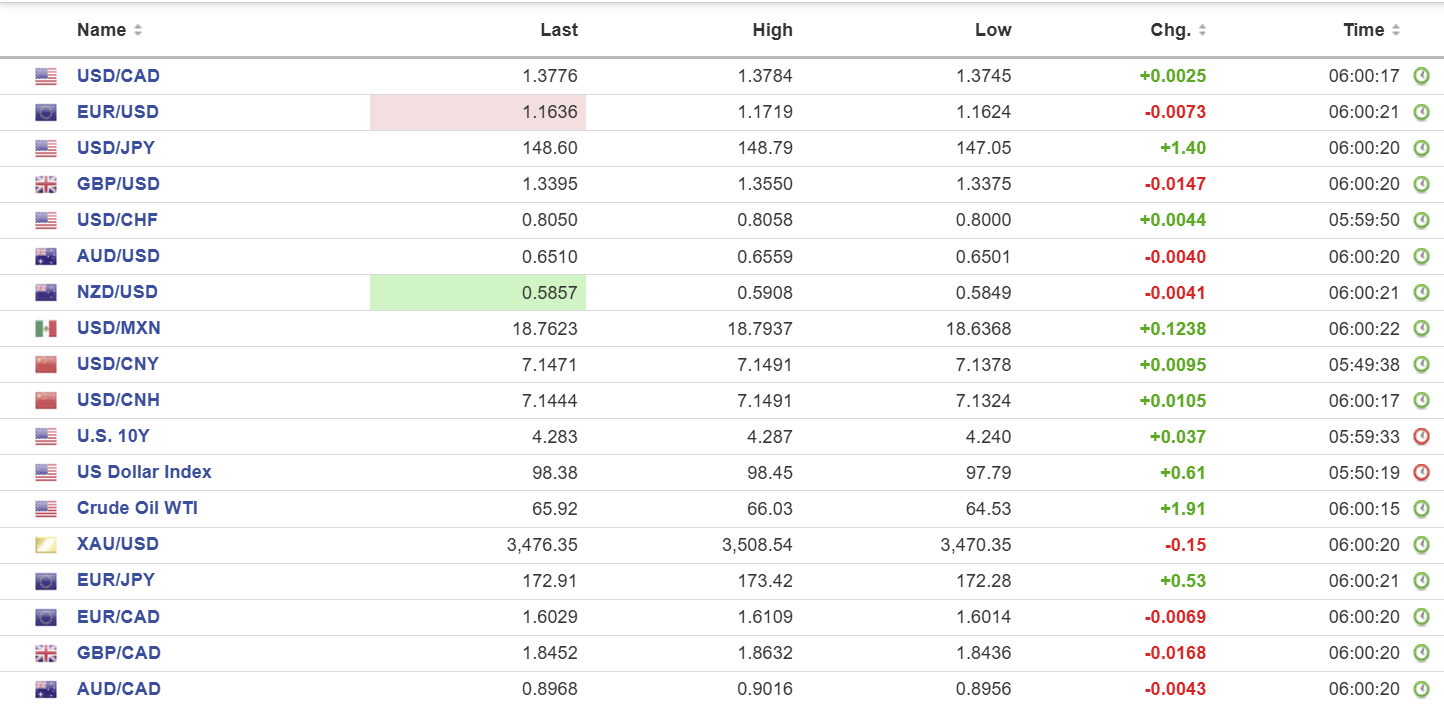

As of 5:20 am PDT, the German DAX is down 1.57%, the French CAC 40 is down by 0.35% and the UK FTSE 100 has dropped 0.61%. S&P 500 futures have fallen by 0.92% and the US Dollar Index (DXY) is 98.35.

EURUSD

EURUSD started September on a positive note and rallied to 1.1736 on Monday after closing at 1.1685 on Friday, then plunged to 1.1634 today. The catalyst seems to be the surge in government bond yields, with the French 30-year bond rising to 4.21%, a 14-year high. Eurozone CPI rose 2.1% y/y (forecast and previous 2.0% y/y) while Core CPI was unchanged at 2.3%. The results will not do anything to stop the ECB from cutting rates on September 11.

GBPUSD

GBPUSD is getting spanked, falling to 1.3375 today after closing Friday at 1.3545 on rising UK debt concerns. Visions of the Liz Truss/Kwasi Kwarteng budget debacle are still fresh and traders are concerned about Chancellor Rachel Reeves’ upcoming autumn budget. That concern manifested into a surge in the 30-year Gilt yield to 5.69%, a 27-year peak and up from 5.34%.

USDJPY

USDJPY soared, rising from 146.79 yesterday to 148.62 today due to both somewhat hawkish comments from a BoJ official and rising 10-year US Treasury yields. Deputy Governor Ryozo Himino said that real interest rates are low even after three rate hikes. The US 10-year Treasury yield rose to 4.287% today from 4.223% on Friday.

AUDUSD

AUDUSD traded defensively in a 0.6501-0.6559 range, with prices weighed down by broad-based US dollar demand. Domestic data was not a factor.

USDMXN

USDMXN rallied from 18.6034 yesterday to 18.7937 today due to rising US interest rates and general US dollar strength.

USDCNY

PBoC fix: Monday 7.1072 vs exp. 7.1281 (Prev. 7.1030). Tuesday: 7.1089 vs exp. 7.1325 (Prev. 7.1072).

Shanghai Shenzhen CSI 300 rose 0.50% to 4523.71 on Monday. Shanghai Shenzhen CSI 300 fell 0.74% to 4490.45 on Tuesday.

NBS and Caixin Manufacturing PMI ticked higher in August, rising to 49.4 and 50.3 respectively.

Xi Jinping is hosting Russia’s Putin, India’s Modi, North Korea’s Kim Jong-un, and another 16 or so world leaders for a victory parade to celebrate China’s defeat of Japan.

Russia and China have signed a new agreement to build a pipeline to China.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics