September 12, 2025

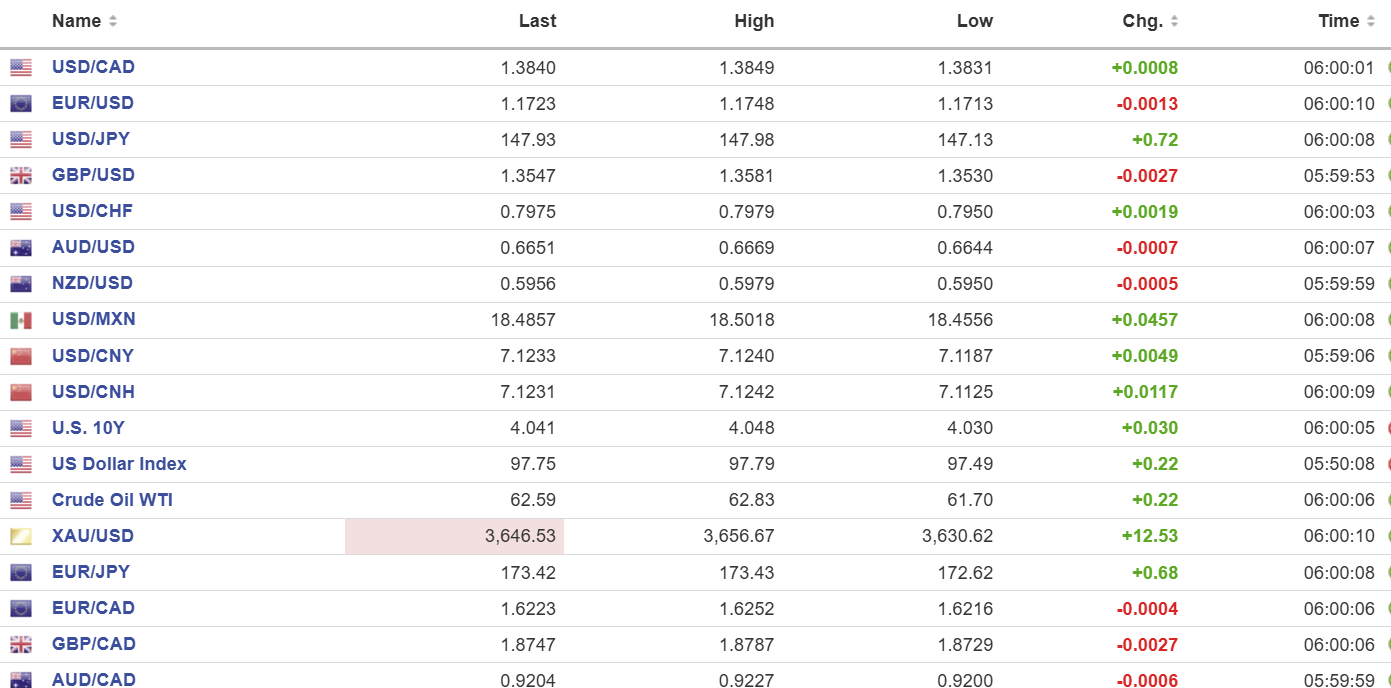

USDCAD open 1.3840 overnight range 1.3831-1.3849, close, 1.3834

USDCAD retreated from a major resistance area yesterday, but rather reluctantly. While the rest of the G-10 majors were amassing respectable gains against the greenback, USDCAD needed to be dragged lower.

The issue is that if the US dollar is being sold because the American economy is slowing, and job losses mounting, forcing the Fed to be more aggressive with rate cuts. Canada is in the same or even worse situation. Speculative short CAD positions are large (last week COT reported -109,000 contracts) and they have likely increased but the positioning is not at extreme levels yet. That means USDCAD could rise further.

The Canadian government announced it was fast-tracking plans to expand LNG Canada Phase 2 in Kitimat, BC, Ontario’s Darlington Nuclear Facility, the Port of Montreal, a copper min in Saskatchewan but failed to mention anything about an oil pipeline.

Canada Building Permits fell 0.1% m/m in July (forecast 4.0%) and Capacity Utilization is 79.3% in Q2 (previous 79.9%).

US Michigan Consumer Confidence is released at 7:00 am PDT.

USDCAD Technical Outlook:

The intraday technicals are bullish but yesterday’s failure to take out resistance in the 1.3900-10 area raises the risk of a profit-taking downside move. A break below 1.3820 targets 1.3780.

The medium-term picture iis neutral and suggests further consolidation in a 1.3760-1.3950 range with momentum indicators only mildly bullish.

For today, USDCAD support is 1.3830 and 1.3790. Resistance is 1.3910 and 1.3950. Today’s Range: 1.3810-1.3910.

The Ball is in the Fed’s Court.

Previously, yesterday’s US CPI data would have been enough to suggest that inflation was far from tamed. Food and energy prices were rising, and the more important Core-CPI rose for the third consecutive month. That’s not what the White House wants to hear, and Fed officials know it. Powell said that falling employment was the Fed’s main concern in his Jackson Hole remarks and policymakers like Bowman and Waller are all in favour of rate cuts. A 25 bp cut is all but confirmed for next Wednesday so traders are content to hear what Powell has to say in the press conference. That, and a lack of actionable US data, should ensure a rather subdued Friday trading session.

Taking Stock

Asian equity indexes closed higher. Japan’s Topix rose 0.06%, Australia’s ASX 200 rose 0.89%, and Hong Kong’s Hang Seng rose 1.16%.

As of 5:30 am PDT, European equities are negative, except for the UK FTSE 100 which has gained 0.36%. The French CAC 40 is down 0.27%, the German DAX has lost 0.11%, and S&P 500 futures are flat. The US Dollar Index (DXY) is 97.81, while Gold sits at 3638.75. The US 10-year Treasury yield is 4.064%.

EURUSD

EURUSD traded in a 1.1713-1.1748 range after yesterday’s ECB monetary policy meeting. The ECB left rates on hold, which was a universally expected outcome, and ECB President Lagarde sounded mildly hawkish, claiming that the deflationary process was over and that the risks to the economy were “more balanced.” Lagarde’s comments and the US data left the EURUSD uptrend from the beginning of August intact while prices are above 1.3400.

GBPUSD

GBPUSD is in the middle of its 1.3530-1.3581 range. A series of disappointing economic reports knocked the currency from its peak. GDP was flat in July, which was expected after rising 0.4% in June. Industrial and Manufacturing production reports both missed forecasts at -0.9% m/m and -1.1% m/m respectively. The UK trade deficit widened.

USDJPY

USDJPY bounced in a 147.13-147.98 range, and it is sitting near the top of that band. Traders are torn between falling US Treasury yields and domestic political drama which may delay a BoJ rate hike.

AUDUSD

AUDUSD extended its week-long rally and traded in a narrow 0.6649-0.6669 range. Prices are underpinned by broad US dollar weakness stemming from expectations for deeper and faster Fed rate cuts while the RBA leaves rates unchanged.

USDMXN

USDMXN consolidated yesterday’s losses in a 18.4556-18.5018 band after plunging from 18.6654 yesterday following the tame inflation and weak jobless claims data. Mexico is planning to hike tariffs on Chinese cars to 50% as well as products from other Asian nations in a move designed to curry favour with Trump.

USDCNY

PBoC fix: 7.1019 vs exp. 7.1081 (Prev. 7.1034)

Shanghai Shenzhen CSI 300 fell 0.57% to 4522.00

China Vice Premier He Lifeng meets with US Treasury Secretary Scott Bessent in Spain next week.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics