June 20, 2025

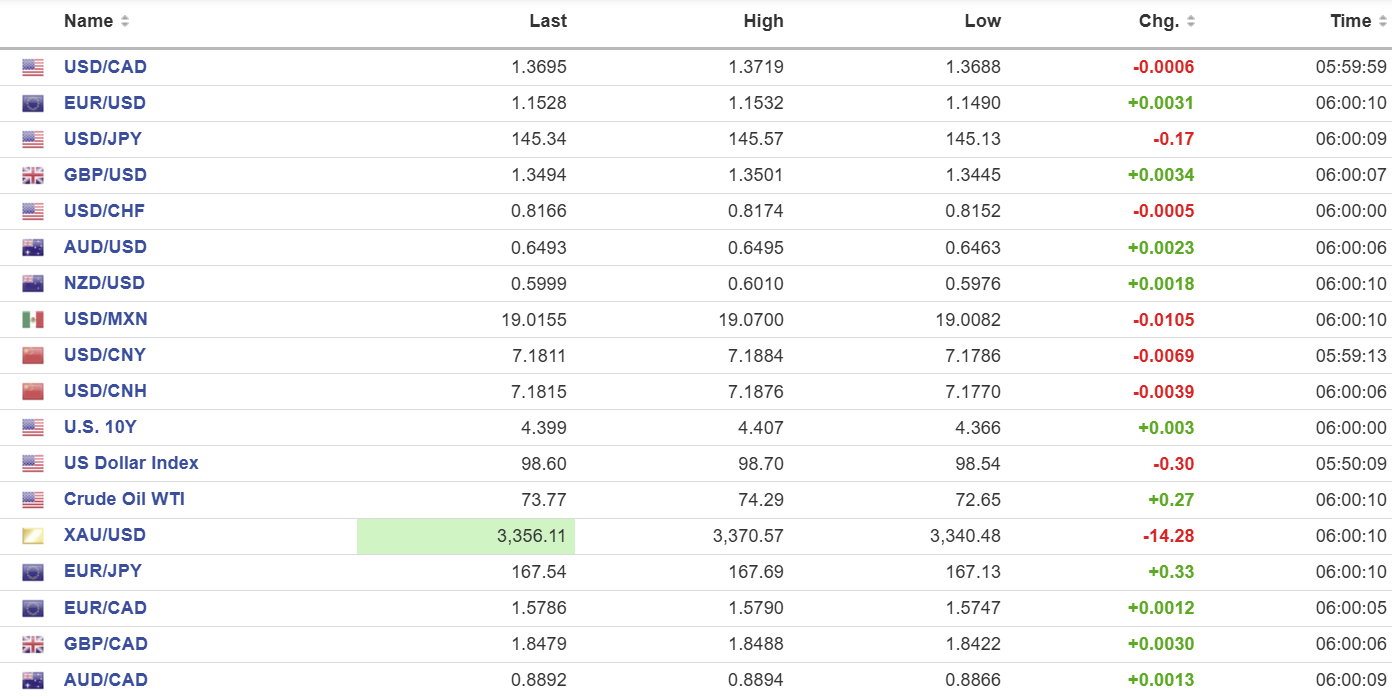

USDCAD: open 1.3696, overnight range 1.3688-1.3719, close 1.3700

USDCAD traded sideways overnight. Trump appears to have decided to delay intervening in the Israel/Iran war for two-week’s which has bolstered risk sentiment, somewhat. But why? It’s not like Trump is selling condo’s and advertising the date they go on sale. In military circles, it is not considered good form, or even smart to give your enemy the date and time of an attack.

Investors know that as well and they are likely to remain on the defensive into the weekend in case, Trump changes his mind.

Prime Minister Carney plans a Canadian response to Trump’s tariffs with a matching counter-tariff to the 50% that the US puts on Canadian steel and aluminum imports. In addition, imports from all other nations without a free trade agreement will rise to 100%.

There are $1.34 billion of 1.3700-1.3710 option strikes rolling off at 10:00 am.

Canada retail sales data for April rose 0.3% m/m (forecast 0.4% m/m, vs March 0.8%) but Core-retail sales fell 0.3% (forecast 0.2%). Industrial Product Prices and Raw Materials prices indices were weaker than expected but USDCAD did not react.

In the US, the Philadelphia Fed Manufacturing Index fell -4 (forecast -1 (previous -4).

USDCAD Technical Outlook: The intraday technicals are bullish above 1.3650 and looking for a break above 1.3745 to test resistance at 1.3800. The uptrend is supported by modestly bullish momentum indicators.

Longer term, the USDCAD outlook is bearish below 1.3800 which guards the longer-term downtrend at 1.4000, although the rising ADX suggests the bearish trend is weakening. USDCAD is appears to want to consolidate within a 1.3600-1.3800 range.

For today, USDCAD support is 1.3650 and 1.3610. Resistance is 1.3750 and 1.3800. Today’s Range 1.3650-1.3750

Markets in Brief

Fed Governor Christopher Waller upset global markets in NY when he said that not only did he think tariffs would not boost inflation, but the Fed could also cut rates as early as July.

China’s PBoC leaves 1 and 5 year LPR rates unchanged at 3.0% and 3.5%, respectively

Iran Foreign Minister Abbas Araghchi said his government rejected talks with the US saying the Americans were already involved in attacking his country. Despite that, French President Macron said that France, the UK, and Germany will present Iran with a “comprehensive negotiation offer,” safe in the knowledge that the Ayatollah only wants to eradicate Israel and not their countries.

WTI oil prices slide to 73.86 from 74.29 on the news that Trump will delay attacking Iran but are still up 9% since Israel’s first strike on Iran’s nuclear facilities. Citibank analysts warn that a loss of 1.1 million barrels-per-day of Iranian crude would boost prices by about 15-20%.

Gold (XAUUSD) fell to 3340.48 before rebounding to 3356.37 in early NY trading. The shiny metal has fallen 94.27 since Monday’s peak due to a mix of profit-taking and a lack of contagion from the Iran/Israel war.

Stock Taking

Asian equity indexes traded softer in the absence of a Wall Street lead do to the Juneteenth holiday. Japan’s Topix fell 0.75% while Australia’s ASX 200 lost 0.21%. Hong Kong traders were in a perky mood and the Hang Seng index closed with a gain of 1.26%.

European traders are feeling a bit of relief after Trump delayed intervening in Iran and from Fed Governor Wallace comment about a July rate cut. The German DAX extended earlier gains and is up 1.56%, the French CAC 40 popped up 0.98% and the UK FTSE 100 index has risen 0.49% S&P 500 futures turned a loss into a 0.22% gain, as of 5:53 am PDT. The US 10-year Treasury yield is 4.44%.

EURUSD

EURUSD benefited from the positive shift in risk sentiment and rose from 1.1490 to 1.1535 in early NY trading. German producer prices data was a tad better than expected but still weak. The unsettle situation in the Middle East

GBPUSD

GBPUSD shrugged off the latest BoE monetary policy decision and caught a bit of a bid overnight, after risk sentiment improved. GBPUSD climbed from 1.3493 to 1.3501 on improved risk sentiment overnight. UK Retail Sales were sharply weaker than expected in May with the headline number falling 1.3% compared to the forecast for a 1.7% increase.

USDJPY

USDJPY traded in a 145.13-145.57 range with prices supported by the shift to positive risk sentiment. However, gains were capped due to a slight increase in Core inflation which rose to 3.7% from 3.5% in April.

AUDUSD

AUDUSD traded sideways in a 0.6463-0.6495 range on improved global risk sentiment. NZDUSD markets were closed for a holiday. Price action for both currency pairs is dictated by US developments and Trump’s plans for Iran.

USDMXN

USDMXN is giving back some of yesterday’s gains as prices slid from 19.0709 to 19.0217 in NY. The retreat is all due to broad US dollar weakness

USDCNY

PBoC fix: 7.1695 vs exp. 7.1801 (prev. 7.1729)

Shanghai Shenzhen 300 rose 0.09%% to 3846.64

PBoC leaves 1-year and 5-year Loan Prime Rate (LPR) unchanged at 3.0% and 3.5%, respectively

China sends 46 military aircraft into Taiwan airspace to protest US politicians meeting with Taiwanese Defence Minister Wellington Koo and because a UK Navy ship transited the Strait of Taiwan.

FX HIGH, LOW, OPEN (as of 6:00 AM ET)

FX data source: Yahoo Finance / Bloomberg / OANDA. Charts: Insert image or URL if applicable.

–