June 23, 2025

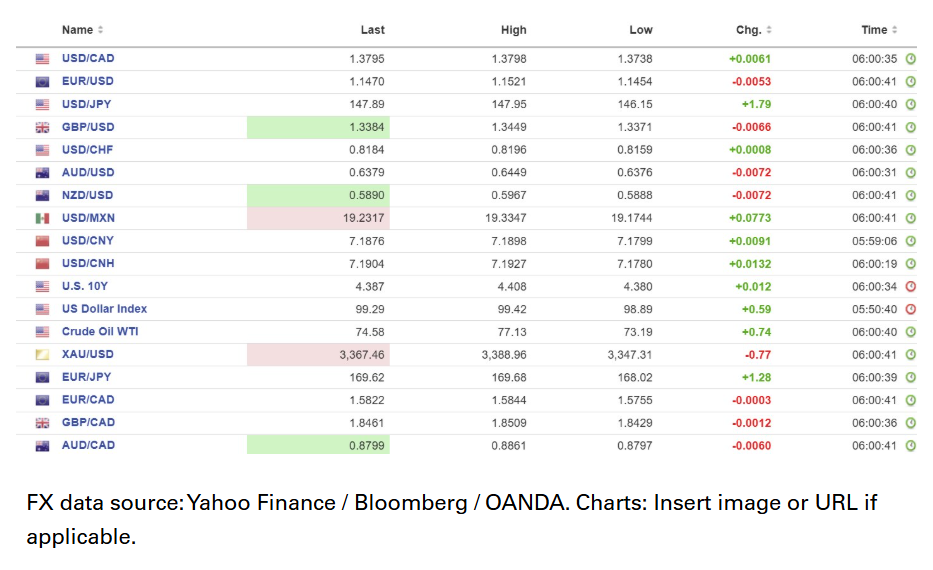

USDCAD: open 1.3795, overnight range 1.3738-1.3798, close 1.3735

USDCAD is trading with a bid due to broad-based US dollar strength. The US attack on Iranian nuclear infrastructure raised fears of Iranian retaliation which could include closing the Strait of Hormuz. In addition, Trump’s veiled threat of a “regime change” in Iran raised fears of an escalating conflict. On the plus side, Canada has plenty of oil and the Loonie may see some benefit from higher crude prices.

On the other hand, Trump’s tariffs have not gone away and BoC Governor is deeply concerned about the inflationary impact on a struggling economy.

Traders are looking ahead to Wednesday when inflation data is due. Canada CPI is expected to rise 0.5% m/m in May. Friday brings the April GDP data and it is expected at 0% (March 0.1%).

Today’s US economic calendar contains S&P Manufacturing PMI and existing home prices.

USDCAD Technical Outlook: The intraday technicals are bullish but mildly overbought with USDCAD in an uptrend channel bound by 1.3710-1.3805. A topside break targets1.3850.

The medium term technicals suggest the rally is a correction unless prices break above the 100 and 200 day moving averages at 1.4041 and 1.4034 respectively.

For today, USDCAD support is 1.3740 and 1.3710. Resistance is 1.3810 and 1.3850. Today’s Range 1.3730-1.3820

Markets in Brief

Add Iran’s Fordo, Natanz, and Isfahan nuclear sites to the list of Things That Go Bang in the Night. The US Air Force dropped a reported 14 GBU-57 Massive Ordnance Penetrators, which effectively set back Iran’s nuclear weapon program by ten years.

Iran’s Ayatollah Khamenei is irate and spewing vitriol at Trump and all things American. It’s nothing he hasn’t been saying since 1979, but unfortunately, Iran’s ability to retaliate with anything other than words has been seriously degraded by Israel’s IDF.

President Trump is also chirping the Ayatollah, saying, “It’s not politically correct to use the term, ‘Regime Change,’ but if the current Iranian regime is unable to MAKE IRAN GREAT AGAIN, why wouldn’t there be a regime change??? MIGA!!!”

The US air raids on Iran have overshadowed the upcoming Fed Chair Powell testimony on Tuesday, as traders shift their focus from economic data and interest rates back to geopolitical tensions.

Richmond Fed President Thomas Barkin and San Francisco Fed President Mary Daly contradicted Governor Christopher Waller’s comments suggesting the case for a July rate cut. Both bank presidents argued there was no urgency to ease monetary policy and that it was too early to make a call about the impact of tariffs on inflation.

WTI oil prices climbed steadily last week as traders anticipated a US attack on Iran’s nuclear sites, rising from 67.84 last Monday to close at 73.88 Friday. Prices spiked to 78.39 in early Asia but have since erased almost all of the overnight gains. The initial spike was due to concerns Iran would close the Strait of Hormuz, which would impact 20% of the world’s crude supply. That hasn’t happened due to Iran’s desire not to annoy China, its biggest oil customer, and because there are a couple of US carrier strike forces in the area.

Gold (XAUUSD) rallied from 3364.79 to 3388.96 in a knee-jerk reaction to the US attack but gave back those gains. And sits at 3362.44 in NY. Traders are now in wait-and-see mode.

Stock Taking

Wall Street closed Friday with small losses, and Asian equity indexes followed suit. Stocks dropped sharply at the Asian open but recovered a large part of the losses by day’s end. Australia’s ASX 200 and Japan’s Topix fell 0.36%, while Hong Kong’s Hang Seng Index rose 0.67%.

European traders are breathing easier after Iran failed to respond to the US attack. The German DAX is down 0.52%, the French CAC 40 index has lost 0.72%, and the UK FTSE 100 is down 0.20%. S&P 500 futures are up flat. (as of 5:30 am PDT) .The US 10-year yield dropped to 4.342% from 4.389% at the open.

EURUSD

EURUSD plunged to 1.1454 from Friday’s close of 1.1524 at the Asia open. Prices popped to 1.1520 after the German economy returned to growth in May. Composite PMI rose to 50.4 (forecast 49, previous 48). S&P Global economists wrote, “There is a decent chance Germany could finally break out of the frustrating stop-start growth pattern it’s been stuck in for the past two years – one quarter of growth followed by another of contraction.” However, prices dropped again after Eurozone PMI data was weaker than expected.

GBPUSD

GBPUSD traded like its European counterpart and for similar reasons. GBPUSD dropped from 1.3447 to 1.3397 then rallied back to 1.3450 before UK data drove prices down to 1.3371. S&P economists wrote that although the UK economy remained in a sluggish state at the end of Q2, “business conditions have continued to improve, which reduced recession fears.”

USDJPY

USDJPY rallied steadily overnight, rising from 146.09 to 147.95 in early NY trading. The surge in oil prices (Japan is a huge importer of crude) more than offset any safe-haven demand for yen due to the US action in Iran. Traders ignored the improvement in the Manufacturing PMI index from 49.4 in May to 50.4 in June.

AUDUSD

AUDUSD suffered from safe-haven demand for US dollars and traded negatively in a 0.6376–0.6449 range. Australian Manufacturing PMI was 51, as expected. NZDUSD traded like its antipodean cousin in a 0.5888–0.5967 range.

USDMXN

USDMXN traded higher last week and extended the gains overnight in a 19.1744–19.3347 range. Geopolitical issues and a somewhat hawkish Fed, combined with the odds of a 50 bp rate cut at Thursday’s Banxico meeting, are underpinning prices.

USDCNY

PBoC fix: 7.1710 vs exp. 7.1914 (prev. 7.1695)

Shanghai Shenzhen 300 rose 0.36% to 3857.90

PBoC leaves 1-year and 5-year Loan Prime Rate (LPR) unchanged at 3.0% and 3.5%, respectively

FX High, Low, Open (as of 6:00 AM ET)