October 7, 2024

- Weak starts on cautious note ahead of US inflation data Thursday.

- Oil grinds higher on supply concerns

- US dollar consolidates Friday’s gains.

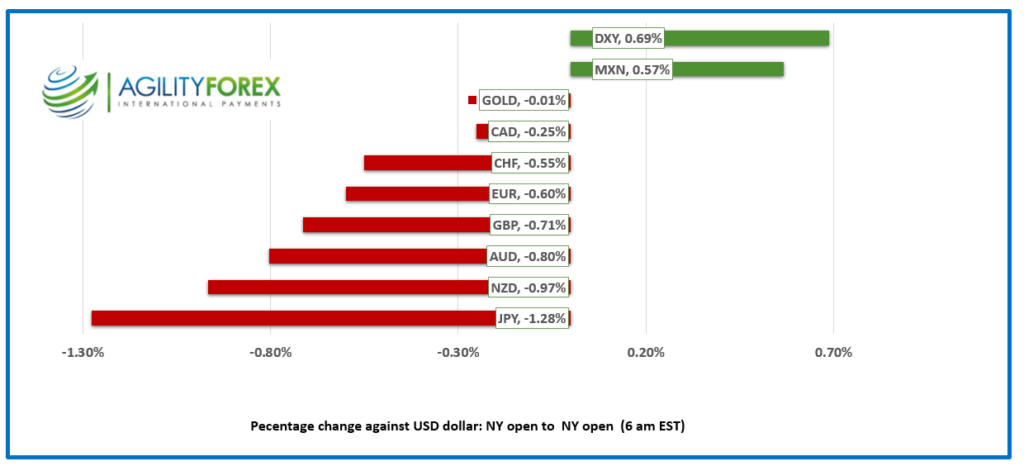

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3590, overnight range 1.3568-1.3599, previous close 1.3576

USDCAD rallied Friday as Friday’s US jobs report underscored the economic disparities between the Canadian and US economies. The US economy is motoring ahead despite a few speed bumps while the Canadian economy is crashing into pot-holes. Bank of Canada Governor Tiff Macklem’s “made in Canada” interest rate policy is going to be put to the test. Canada’s economic growth is fueled by government spending and the only sector adding new jobs is the government. Inflation is at the BoC target and expected to fall further. All of that points to the BoC cutting rates by 50 bps on October 23. If so, USDCAD will test 1.3750.

WTI oil prices remain bid in a 73.63-76.42 range due to ongoing supply disruption concerns from the middle east. In addition Ukraine is claiming it struck a large oil terminal in Russian occupied Crimea.

Ther are no Canadian economic reports today,

USDCAD technicals

The intraday USDCAD are bullish above 1.3560 and looking to break resistance in the 1.3610-1.3640 area to extend gains to 1.3690, then 1.3750. A break below 1.3560 suggests further 1.3490-1.3630 consolidation.

Longer term, USDCAD is in an uptrend above 1.3500 on the daily chart with a break above 1.3600 (200 day moving average) targeting the 100 day moving average at 1.3650. In addition a decisive breach of 1.3630 opens the door to further gains to 1.3750.

For today, USDCAD support is at 1.3560 and 1.3520. Resistance is at 1.3610 and 1.3630.

Today’s Range 1.3550-1.3630

Chart: USDCAD daily

Source: Investing.com

Greenback Rules—Others Drool

Friday’s stellar US nonfarm payrolls report rejuvenated the US dollar, which many pundits had written off ahead of expected jumbo Fed rate cuts and a slowing American economy. That isn’t happening, and it’s back to the drawing board. Traders are ignoring election politics while the Middle East war gives the greenback a bit of a bid. That won’t change today as there isn’t any top-tier data, although Fed speakers (Kashkari, Bostic, and St. Louis Fed President Musalem) might say something that catches markets by surprise.

Stocks Are Mixed Due to High Treasury Yields

The surge in the US 10-year Treasury yield from 3.70% on October 1 to 4.02% overnight has not put a damper on the enthusiasm for equities. Lingering positive sentiment from the previous Chinese fiscal and monetary stimulus continued to support Asian stock indexes. Hong Kong’s Hang Seng rose 1.60%, while the free-falling yen helped lift Japan’s Topix to a 1.68% gain. European bourses are mixed. The UK FTSE 100 is up 0.28%, while weak German data helped drive the German DAX down 0.24%. S&P Futures are down 0.47%.

EURUSD

EURUSD consolidated Friday’s losses in a 1.0955-1.0979 range. The breach of support at 1.1000 turned the technicals negative, and that level will revert to resistance. EURUSD is pressured by downgraded rate-cut risks from the Fed, while the ECB rate outlook remains unchanged. EURUSD will see support in the 1.0950 area today around the 10:00 am option expiry window as $3.1 billion of strikes expire. German factory orders fell 5.8% m/m in August (forecast -2%, previous -3.9%). Eurozone retail sales rose 2.0% m/m in August, as expected.

GBPUSD

GBPUSD traded poorly in a 1.3062-1.3135 range. Prices never recovered from dovish comments by Bank of England Governor Andrew Bailey last week, and Friday’s US jobs data merely exacerbated the losses. The break below 1.3210 snapped the September uptrend line, and further losses below 1.3000 target 1.2880.

USDJPY

USDJPY soared from 145.93 to 149.00 on Friday in the wake of the US jobs report and the spike in 10-year Treasury yields, then consolidated the rally in a 148.06-149.14 range overnight. USDJPY was already underpinned after last week’s comments by Japan Prime Minister Shigeru Ishiba, who said the economy wasn’t ready for further rate hikes. Friday’s NFP data threw fuel on the fire as it eliminated hopes that the Fed would repeat September’s 50 bp rate cut in November.

AUDUSD and NZDUSD

AUDUSD traded negatively in a 0.6777-0.6811 range following Friday’s post-NFP losses, in a subdued overnight session as Australian markets were closed for Labour Day. The TD-MI inflation gauge rose to 2.6% y/y from 2.5% in September.

NZDUSD is at the bottom of its 0.6136-0.6173 range. Traders are hoping that the government’s plan to fast-track 149 projects gives the economy a boost and provides support for the currency. Most economists predict that the slowing labor market and falling inflation will prompt the RBNZ to cut rates by 50 bps on Wednesday.

USDMXN

USDMXN consolidated Friday’s losses in a 19.1936-19.2934 range, and prices are in an intraday downtrend while below 19.6300. Prices are being pressured due to rapidly fading US recession fears following Friday’s US nonfarm payrolls data.

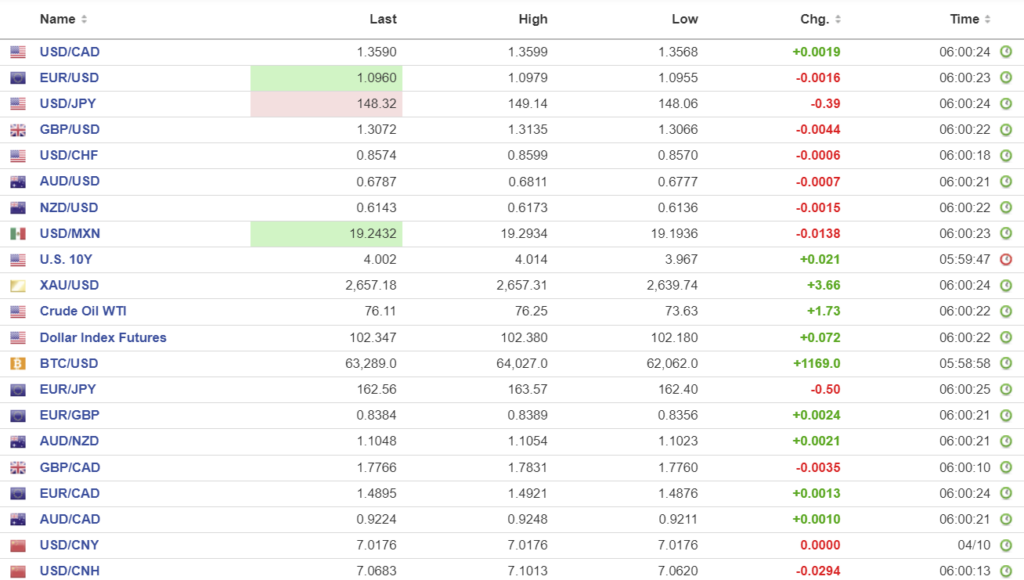

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

Still Closed PBoC fix: unchanged 7.0074 (prev. 7.0101)

Shanghai Shenzhen CS! 300 closed at 4017.85 (as of September 30)

China is on the last day of its Golden Week holidays and the stock market may have more upside when it opens tomorrow. That’s because Goldman Sachs analysts are predicting stocks could rise another 15-20% if Chinese authorities deliver on the stimulus promises.

Chart: USDCNY and USDCNH

Source: Investing.com