May 10, 2024

- Canada adds 90,400 new jobs in April

- Better-than-expected UK data underpins GBP.

- US dollar opens lower-Gold and MXN outperform.

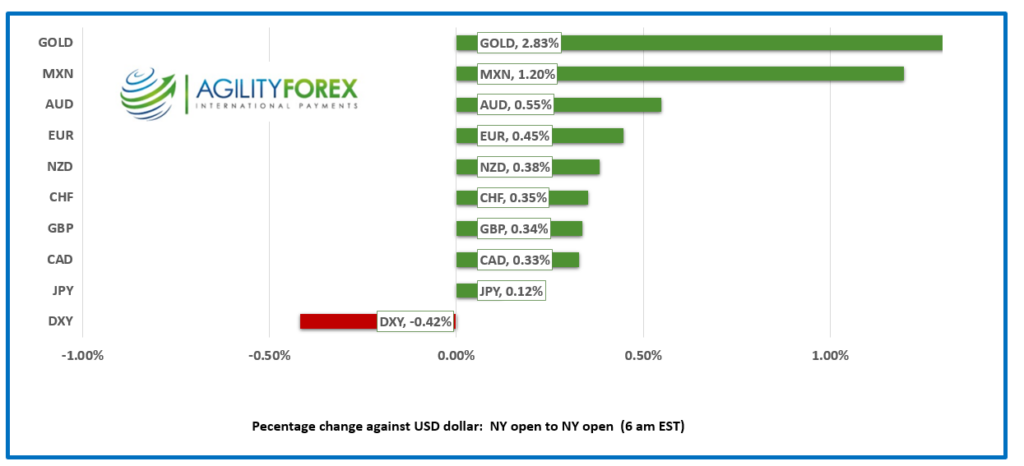

FX at a Glance

Source: IFXA/RP

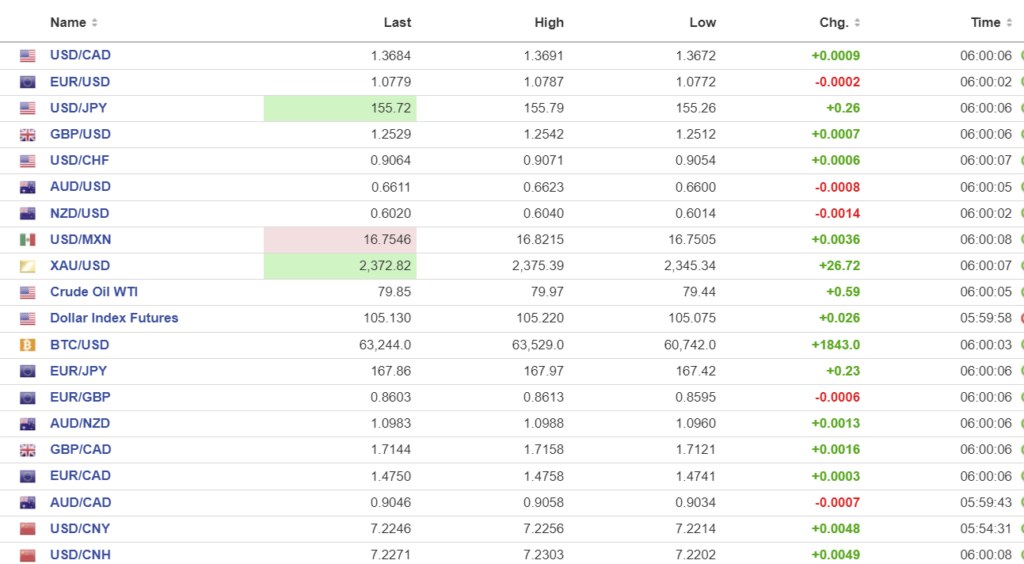

USDCAD Snapshot: open 1.3684, overnight range 1.3634-1.3691, close 1.3679

The Canadian economy is a job-creating machine. Canada gained 90,000 new jobs in April, which included another 25,500 jobs in the already bloated public service sector. The unemployment rate was unchanged at 6.1%. BoC officials may take note of the 4.7% increase in average hourly wages which could delay a further drop in inflation if those wage increases force companies to raise prices. USDCAD dropped to 1.3634 from 1.3687 on the news but has since bounced to 1.3655.

Yesterday, USDCAD dropped on the back of rekindled Fed rate cut hopes after weekly jobless claims rose more than expected which suggested higher rates were finally accelerating the normalization of the job market. However, the results are a bit dodgy as the rise in claims coincided with the NY city school spring break (public school workers such as bus drivers are allowed to apply for benefits during winter and spring breaks). Traders must have forgotten that Fed Chair Powell and his colleagues are adamant that it will take longer than expected for inflation to fall to its 2.0% target.

USDCAD Technicals

The intraday USDCAD technicals are bearish while trading below 1.3690 and looking for a move below 1.3650 to extend losses to 1.3610. A break above 1.3690 targets 1.3760.

The daily chart is bullish. The uptrend line from January 1 is intact above 1.3590 which is guarded by support in the 1.3650-60 area which represented previous bottoms.

For today USDCAD support is at 1.3650 and 1.3610. Resistance is at 1.3710 and 1.3760. Today’s range is 1.3630-1.3730.

Chart: USDCAD daily

Source: DailyFX

“A Little Less Conversation”

That’s what markets may be saying after a rash of Fed policymakers hit the rubber chicken circuit today. Fed Governor Lisa Bowman (voter), Minneapolis Fed President Neel Kashkari (non-voter), Dallas Fed President Lorie Logan (non-voter), Chicago Fed President Austan Goolsbee (voter), and Fed Vice Chair Michael Barr (voter) are speaking throughout the day.

Yesterday, San Francisco Fed President Mary Daly said that it may take more time to return inflation to target, which is also what Fed Chair Powell and other FOMC policymakers have been saying. That suggests that the euphoria over yesterday’s weekly jobless claims number will fade quickly.

Equity markets

Asian equity indexes closed with gains across the board, led by a 2.30% rise in the Hong Kong Hang Seng index. Japan’s Nikkei 225 index rose 0.41% while Australia’s ASX 200 gained 0.35%. European bourses are well into the green. The French CAC 40 index and UK FTSE 100 indexes are up 0.84%, and S&P 500 futures are up 0.37%. Gold (XAUUSD) surged 2.83% from yesterday’s opening level.

EURUSD

EURUSD drifted in a 1.0772-1.0787 band due to renewed Fed rate cut speculation. The ECB monetary policy accounts from the April meeting reveal further hints that rates will be cut in June. The ECB is more confident about that downward path of inflation than worried about upside risks.

GBPUSD

GBPUSD extended yesterday’s gain and traded in a 1.2512- 1.2542 range. The currency pair is underpinned by yesterday’s Bank of England decision that left rates unchanged and raised hopes of interest rate cuts in the next few months. Today’s April GDP data dampened the euphoria. April GDP grew at 0.4% in March, well above the 0.1% expected and February’s GDP result was revised higher (0.2% from 0.1% m/m). GDP grew 0.6% q/q and 0.2% y/y. BoE Chief Economist Hu Pill said that it would “ill-advised” to just focus on the June meeting. He said he is focused on the underlying inflation components, not the headline rate.

USDJPY

USDJPY is trading robustly and is at the top of its 155.26-155.79 overnight range in early NY. Traders seem to be ignoring the US 10-year Treasury yield which is steady at 4.475%, despite being well -below yesterday’s 4.56% peak. There was little to no impact from a weak Eco watchers survey which showed Current conditions falling to 47.4 in April from 49.8 in March.

AUDUSD and NZDUSD

AUDUSD consolidated Thursday’s gains in a 0.6600-0.6623 range The prospect of weaker economic growth and the dovish tilt to the RBA suggest limited upside in the short-term.

NZDUSD is near the bottom of its 0.6014-0.6040 overnight range as it consolidates yesterday’s post-US data rally. The NZ Manufacturing index rose 2.1 to 48.9 in April but remains in contraction territory.

USDMXN

USDMXN fell sharply yesterday, dropping from 16.9563 at the NY open to 16.7742 by the end of the day then consolidated the move in a 16.7505-16.8215 range overnight. The sell-off was due to the US weekly data and Banxico’s decision to leave interest rates unchanged at 11.00%. The central bank raised its inflation forecasts for the next six quarters.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

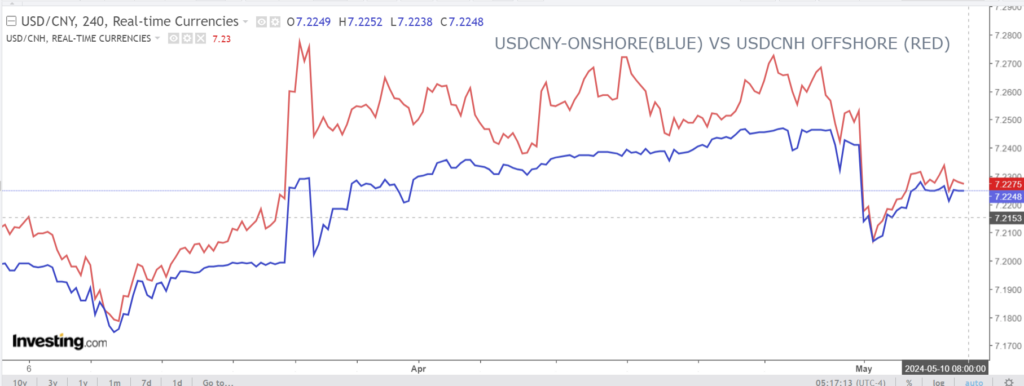

China Snapshot

PBoC fix: 7.1011 vs exp. 7.2102 (prev. 7.1028)

Shanghai Shenzhen CSI 300 rose 0.05% to 3666.28.

US to announce new tariffs which will include electric vehicles, batteries, and solar cells.

China pondering a dividend tax waiver for individual investors on HK stocks bought via Stock Connect,

Chart: USDCNY and USDCNH

Source: Investing.com