October 27, 2023

- Fed favourite-Core-PCE rises 3.7% as expected.

- Wall Street may open in positive territory.

- US dollar is still bid but opens on a mixed note.

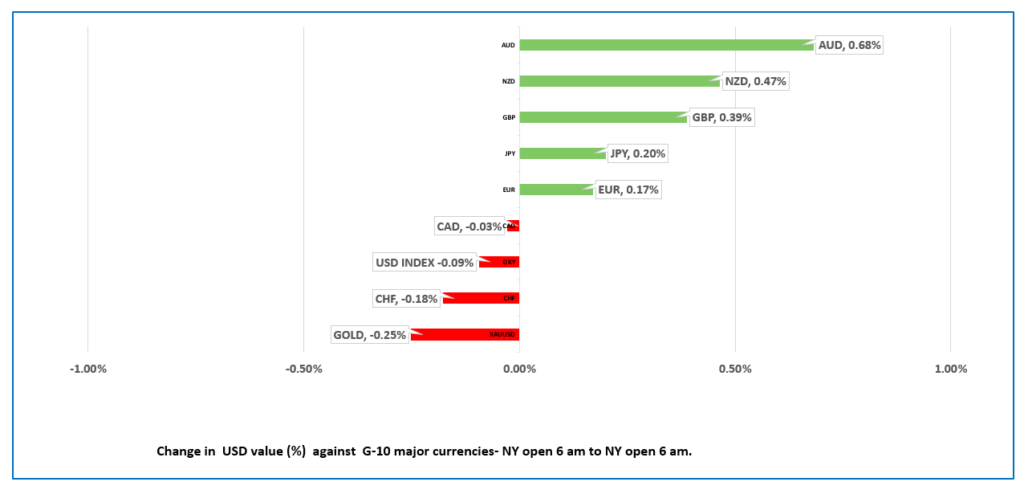

FX at a Glance

Source: IFXA/RP

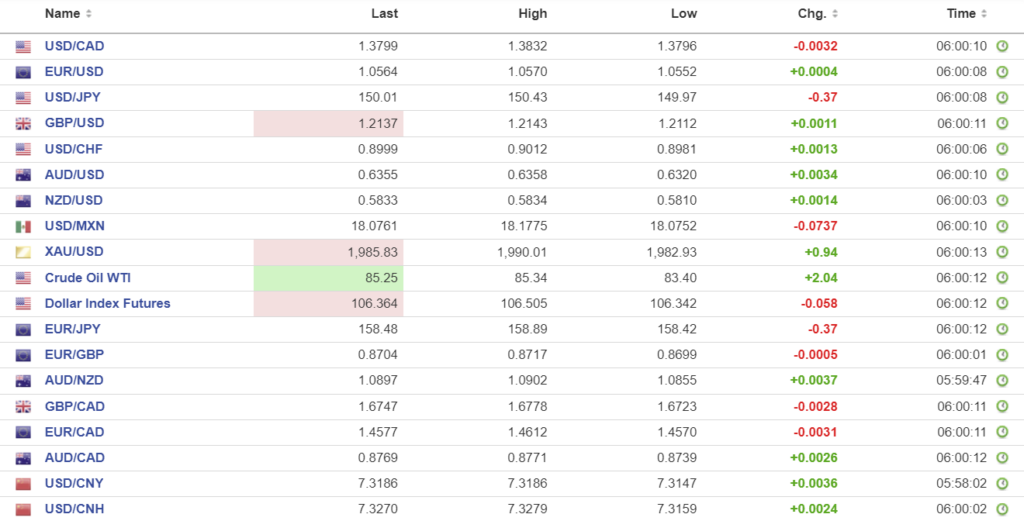

USDCAD Snapshot: open: 1.3793-97, overnight range 1.3796-1.3832, close 1.3832

USDCAD drifted aimlessly overnight and opened unchanged from yesterday. Prices are supported by the ongoing risk for a hawkish Fed outcome next Wednesday with at least one more Fed rate hike on the table while the Bank of Canada’s rate hike cycle may have ended.

USDCAD is a passenger on the FX bus. It’s direction is determined by risk sentiment; US Treasury yields S&P 500 performance and occasionally WTI moves. That won’t change today.

WTI oil prices are rangebound in a $82.00-$88.00/b as the risk of slowing global growth offsets Opec production cuts.

USDCAD Technicals:

The week-long USDCAD uptrend is intact above 1.3730 which was also the previous top and is now support. That level is guarding the October trend line which comes into play at 1.3620 and the July uptrend line which is at 1.3540. A break above 1.3860 targets 1.4000 while a move below 1.3770 puts 1.3730 in play.

For today, USDCAD support at 1.3770 and 1.373. Resistance at 1.3860 and 1.3920. Today’s expected trading range is between 1.3770-1.3850

Chart: USDCAD 4 hour

Source: Daily FX

G-10 FX recap

FX traders took it easy overnight and banked some profits. The US dollar opened in New York on a mixed note compared to where it started on Monday. The Australian dollar is the big winner, gaining 1.04%, while the Swiss franc (down 0.83%) beat out the Canadian dollar (down 0.57%) for the biggest loser trophy.

Yesterday showcased the US economy’s robustness, with Q3 GDP exceeding expectations (actual 4.9% y/y), compared to the forecast of 4.2%. This performance throws a wrench in the narrative of the Federal Reserve engineering a soft economic landing and suggests that the economy is not even on its final descent.

However, it’s not all sunshine and unicorns out there, despite traders being in a mildly risk-positive mood. A new Psycho-Pact is forming. Russia entertained Hamas terrorists and Iran’s Deputy Foreign Minister, while China said it firmly supports Iran.

The US responded by bombing targets in Syria, used by Iran’s Revolutionary Guards.

Asian equity indexes took heart from news Amazon’s earnings were higher than expected and closed with solid gains. Japan’s Nikkei 225 index rose 1.27%, while Australia’s ASX 200 gained 0.21%. European bourses are mixed, while S&P 500 futures are up 0.46%. The US 10-year Treasury yield is 4.86% after falling from 4.95% yesterday.

The US Core-PCE price index rose 3.7% y/y as expected and a tick lower than the downwardly revised 3.8% result in August. The US dollar popped following the data but equity and bonds barely budged.

EURUSD is at the bottom of its 1.0535-1.0570 range, post PCE. The single currency is trading with a bearish bias after yesterday’s ECB meeting was uneventful. Today’s US data suggests US rates could still go higher while ECB rates may have peaked.

GBPUSD dropped to 1.2105 from an overnight peak of 1.2143 after the US PCE results. The contrast between US and UK economic growth and caution ahead of next week’s Bank of England meeting is weighing on the currency.

USDJPY traded in a 149.90-150.43 range with prices being undermined by Tokyo inflation data (September 3.3% vs August 2.8%) raising risks for the Bank of Japan to tighten policy next week by tweaking the yield curve control (YCC) cap.

AUDUSD traded with a mild bid in a 0.6320- 0.6358 range. The currency is supported by the latest Producer Prices Index report (Q3 1.8% q/q, vs Q2 0.5%) raises the risk of an RBA rate hike.

The Michigan Consumer Sentiment Index is expected to be unchanged at 63.

Source: Investing.com

China Snapshot

PBoC fix: today 7.1782, previous 7.1784.

Shanghai Shenzhen CSI 300 rose 1.37% to 3562.39.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com