Photo: wikimedia commons

- US NFP surge 531,000, Unemployment rate dips to 4.7%

- Canada employment rises higher than expected

- US dollar still bid after jobs data

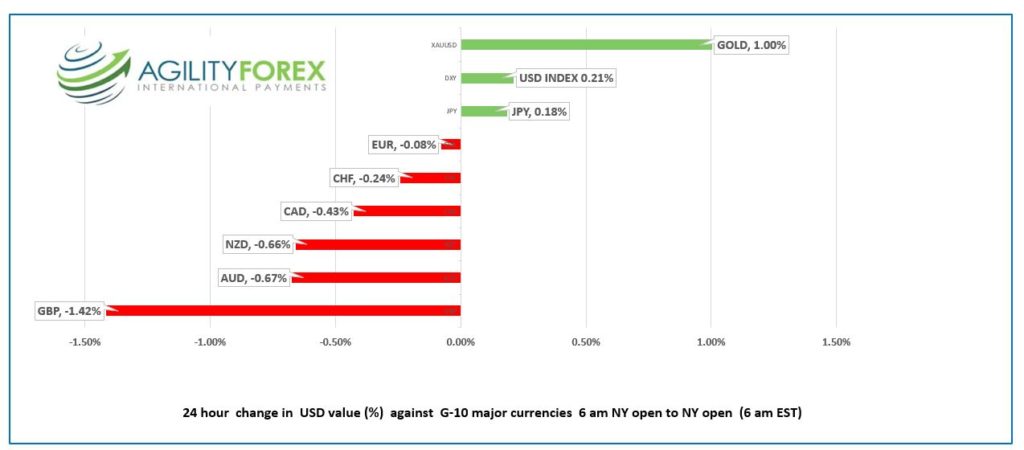

FX at a Glance:

Source: IFXA Ltd/RP

USDCAD Snapshot Open 1.2468-72, Overnight Range 1.2454-1.2478, Previous close 1.2460

USDCAD consolidated yesterdays gains and traded quietly overnight with prices supported by the drop in WTI oil prices from $84.85/b on Monday to $78.50/b, post FOMC and Opec meeting. Opec ignored President Biden’s request to raise production by 600-800 thousand barrels per day and stuck to their scheduled increase of 400,000 barrels for December. That news should have boosted crude prices but instead it sparked a profit-taking, “buy the rumour, sell the news” drop. Prices have since bounced to $79.82/b today.

Canada added 31,200 jobs in October, compared to the consensus forecast for a 19,300 gain while the unemployment rate dipped to 6.7%, which is still 1.0% above the pre-pandemic level. USDCAD retreated on the news.

As usual, domestic data takes a back seat to US economic reports and the better than expect nonfarm payrolls data supports the view the Fed will be forced to raise interest rates as early as May 2022.

Technical view: The intraday USDCAD technicals are bullish above 1.2390 after breaking the September 2021 downtrend with the move above 1.2380 on Tuesday. The 1.2500 area will be sticky as former support reverts to resistance. A decisive break above 1.25 50 suggests further gains to 1.2660. A move below 1.2390 points to further 1.2300-1.2500 consolidation.

For today, USDCAD support is at 1.2430 and 1.2400. Resistance is 1.2500 and 1.2520. Today’s range 1.2430-1.2505.

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The US added 531,000 new jobs in October, easily beating the forecast of 425,000. The US dollar was mixed after the news, but US equity futures rallied. Even so, the results are too close to the FOMC meeting to do much to change the current rate hike view.

The major Asia equity indexes closed with losses led by those in China, thanks to more property company woes. Australia’s ASX 200 was the outlier and posted a 0.39% gain. European bourses are extended earlier gains, post NFP, with the French CAC 40 gain of 0.96%, leading the charge. DJIA and S&P 500 futures have notched a 0.36% increase. WTI oil prices gained 0.97% and gold is close to unchanged. US 10-year Treasury yields traded in a 1.52%-$1.554% band, as of 5:50 am PT.

EURUSD at the bottom of its overnight 1.1516-1.1562 range. ECB policymakers Luis de Guindos and Yannis Stournaras said inflation pressures were temporary which reinforced the ECB’s dovish outlook. Weaker than expected German Industrial Production data (actual -1.1% m/m vs forecast 1.0%) and soft Eurozone Retail Sales (actual -0.3%m/m vs forecast 0.2%m/m) didn’t help sentiment. The intraday EURUSD technicals are bearish below 1.1580.

GBPUSD continues to be punished after the Bank of England (BoE) left interest rates unchanged despite broad hints to the contrary by Governor Bailey and Chief Economist Huw Pill prior to the meeting. A defensive Mr. Bailey claimed his comments were just a “conditional statement.”

GBPUSD extended Thursday’s losses and fell from 1.3507 to 1.3426 , with EU/UK Brexit issues and the threat that the UK triggers Article 16, undermining the currency pair.

USDJPY spiked to 114.02 from 113.85 after the NFP results but those gains were quickly erased.

AUDUSD is at the bottom of its 0.7370-0.7407 range after the RBA Quarterly Statement on Monetary Policy reaffirmed the central bank’s dovish outlook. NZDUSD retreated due to broad US dollar demand.

Chart of the Day: S&P 500

Source: Saxo Bank

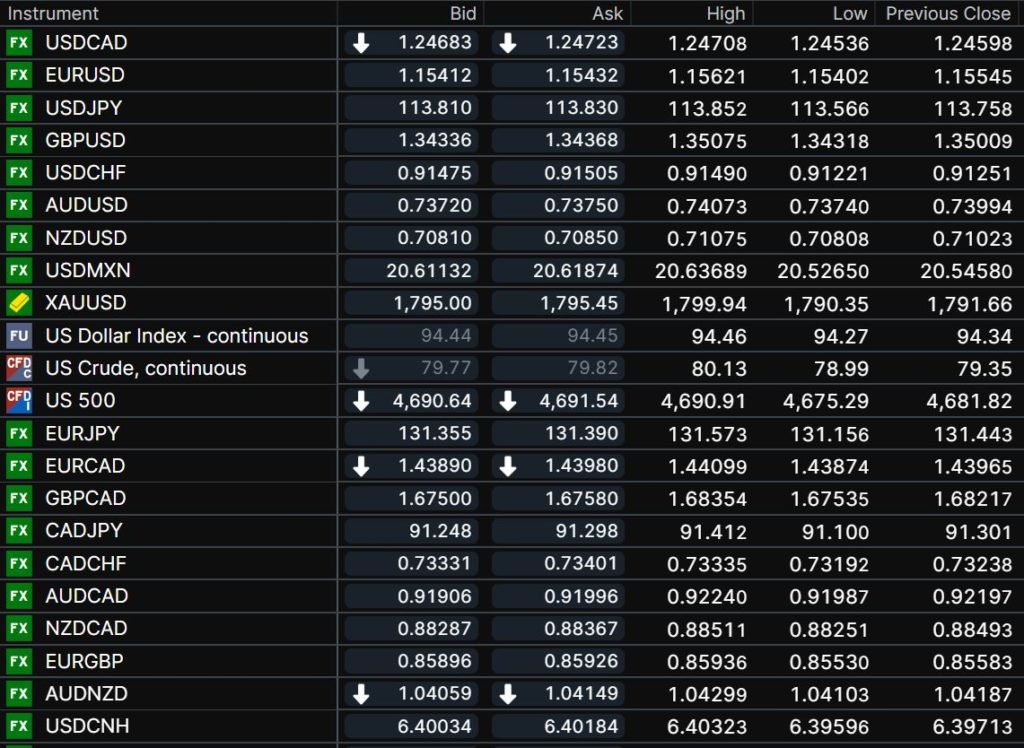

FX open, high, low, previous close

Chart: Saxo Bank

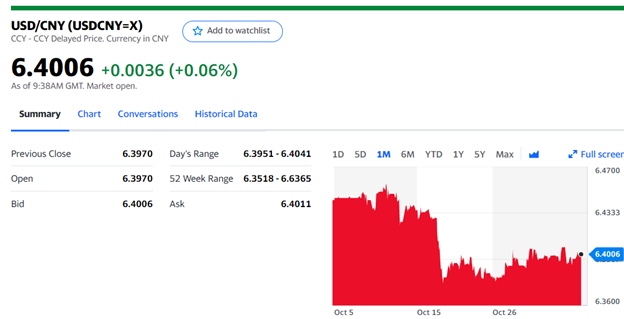

China Snapshot

Today’s Bank of China Fix 6.3980, Previous 6.3943

Shanghai Shenzhen CSI 300 rose 0.99% to 4,868.74

Another property group (Kaisa Group) missed payments and share trading was halted. Company planning to sell projects in Shanghai

JPMorgan cuts China Q4 GDP forecast to 4.0% from 5.0% due to energy issues and rising Covid cases.

Chart: USDCNY 1 month

Source: Yahoo Finance