Photo: BingAI

July 18, 2023

- Canada Core-CPI falls more than expected.

- US Retail Sales expected to rise 0.5% m/m in June.

- USD opens mixed after choppy, but narrow overnight session.

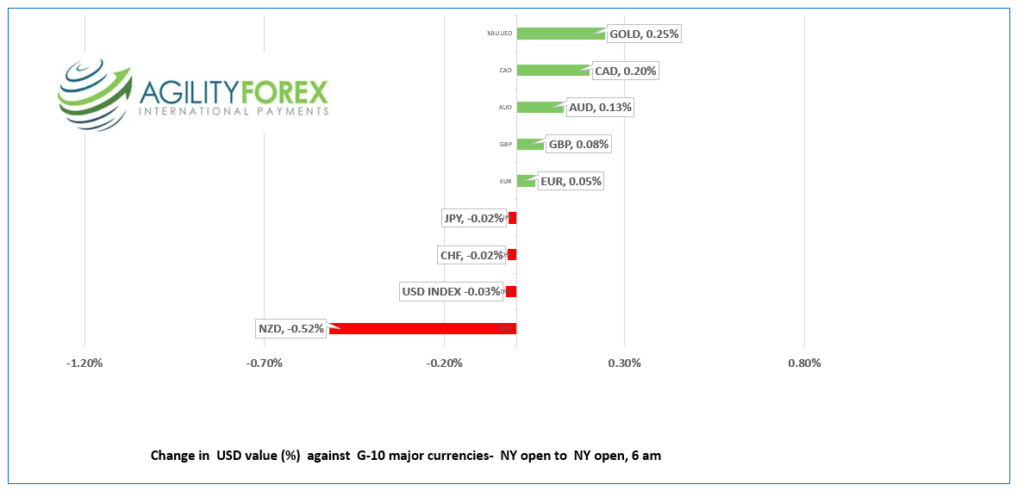

FX at a glance:

Source: IFXA Ltd

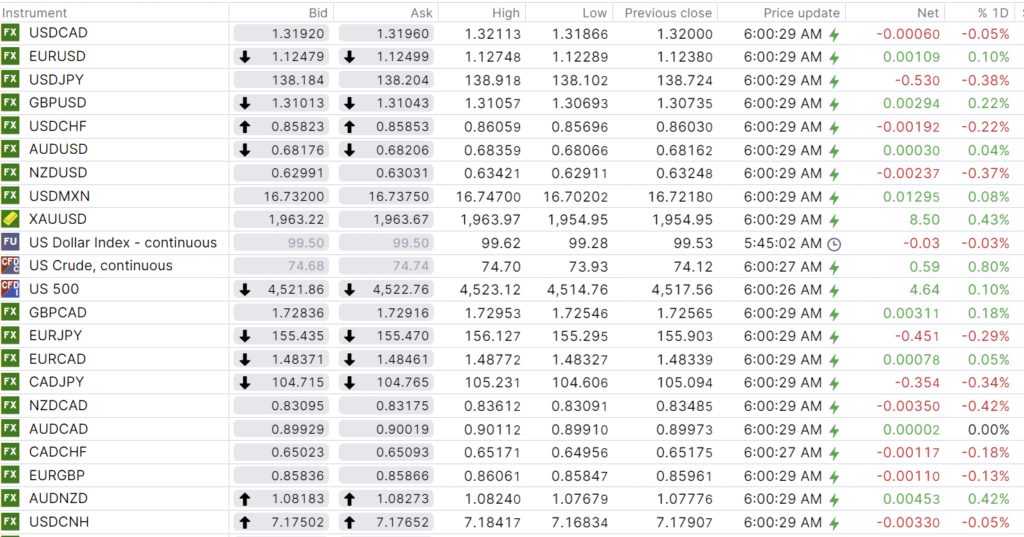

USDCAD Snapshot: open 1.3192-96, overnight range 1.3187-1.3234, close 1.3200

Statistics Canada reported June CPI rose 2.8% y/y (May 3.4%) while Bank of Canada Core CPI rose 3.2% (3.7% in May).

However, inflation is one statistic with so many moving parts, policymakers, and economists cherry pick pieces of data to form conclusions.

For instance, Statistics Canada said that if you exclude gasoline, CPI would have been 4.0%. The Bank of Canada excludes fruits, vegetables gasoline, fuel oil, natural gas, mortgage interest, intercity transportation, and tobacco products to come up with its Core-CPI reading of 3.2%.

Confused? You should be. It is to the BoC’s advantage to muddle the inflation file so that they can justify whatever actions they are taking in the interest of price stability.

The headline reading of 2.8% y/y strongly suggests that the BoC erred when they decided to hike rates by 25 bps as inflation is now within the BoC targeted range of 1-3%.

Canadian Raw Materials and Industrial Product prices were also lower than expected.

USDCAD dipped then rallied on the news, perhaps because with headline CPI sitting inside the mandated inflation target band, the BoC’s next move is to cut rates.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish. Friday’s rally above 1.3160 negated the steep, short-term downtrend from July 7, but the more gently sloped downtrend from July 10 is intact while prices are below the 1.3220-1.3230 area. A top[side break puts 1.3300 in play.

Longer term, USDCAD is in a 1.3040-1.3500 range with the March 2023 downtrend line trying to guide prices below the long term uptrend line (from May31, 2021) at 1.3040.

For today, USDCAD support is at 1.3160 and 1.3100. Resistance is at 1.3240 and 1.3305. Today’s range 1.3170-1.3260.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

It is a typical summer market. A rash of top-tier data is attempting to motivate traders ahead of central bank meetings and cold beer on a hot patio. The beer will win out.

US Retail Sales are rose 0.2% (forecast 0.5%) and ex-autos rose 0.2% m/m (forecast 0.3%). The results failed to spark much interest in FX markets while S&P 500 futures drifted slightly lower.

EURUSD traded with a bullish bias in a 1.1229-1.1275 range with prices getting an added boost by the drop in US Treasury yields. Eurozone HICP data is on tap Thursday, and it will determine if EURUSD breaks above 1.1300, or retests 1.1150.

GBPUSD traded sideways, albeit with a modest bid, in a 1.3069-1.3109 range. Traders are cautious ahead of Wednesday’s inflation data. CPI is expected to fall to 8.%2 from 8.7% y/y, while Core-CPI is expected to be unchanged at 7.1% y/y.

USDJPY nearly fully-reversed yesterday’s move and dropped from 138.92 to 138.10. The decline coincided with the US 10-year Treasury yield falling to 3.764% today from 3.813% at yesterday’s close.

AUDUSD chopped noisily in a 0.6807-0.6836 after the minutes from the July 4 RBA monetary policy meeting showed policymakers were indecisive about the need for another rate increase in July. Thursday’s employment data may be the key.

NZDUSD traded with a negative bias, falling from 0.6342 to 0.6291 ahead of Wednesday’s Q2 CPI data (forecast 5.9% y/y vs 6.7% previously)

Also on tap: Capacity Utilization, Industrial Production, Business Inventories, and NAHB Housing Market Index.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

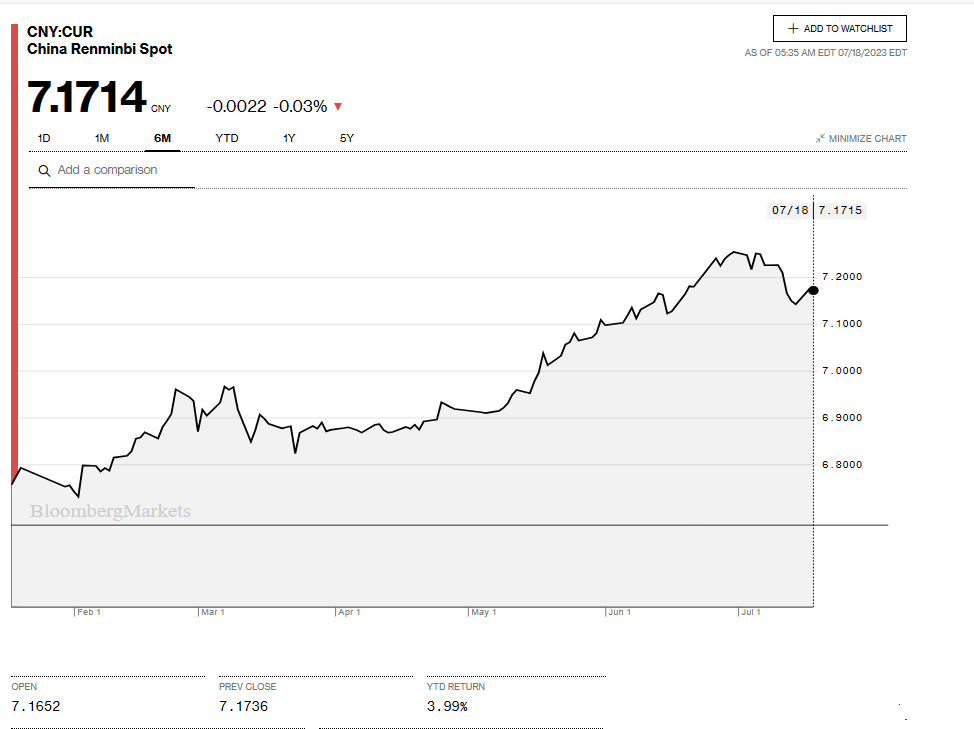

China Snapshot

Bank of China Fix: 7.1453 expected 7.1704, Previous 7.1326

Shanghai Shenzhen CSI 300 fell 0.32% % to 3854.94.

China Commerce Ministry, attempting to support consumption in home appliances, furniture and textiles, announced it would support companies to develop green household products. No one was impressed.

Chart: USDCNY 6 month

Source: Bloomberg