Photo: openclipart.org

June 9, 2023

- Canada loses 17,000 jobs

- Market now expects Fed to “skip” a June rate hike.

- US dollar opens lower compared to Thursday, but firms in overnight.

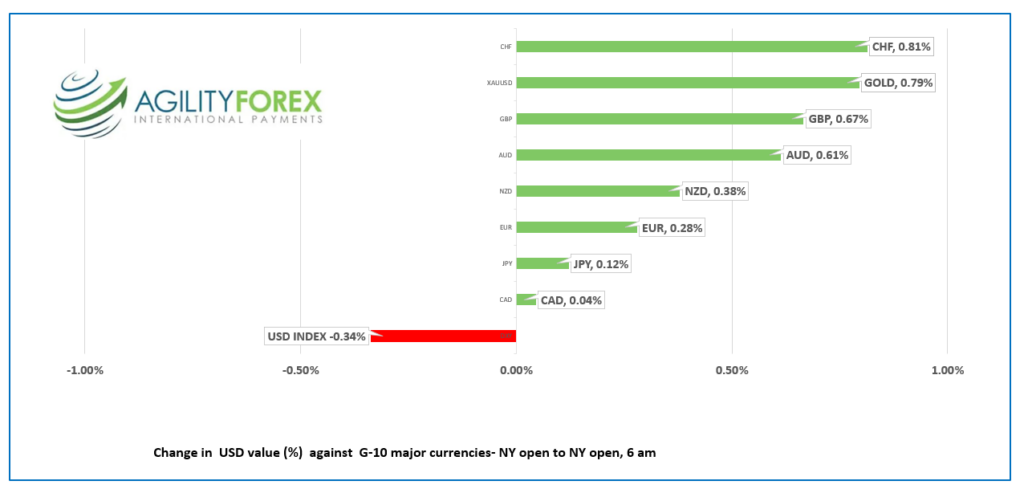

FX at a glance

Source: IFXA Ltd/RP

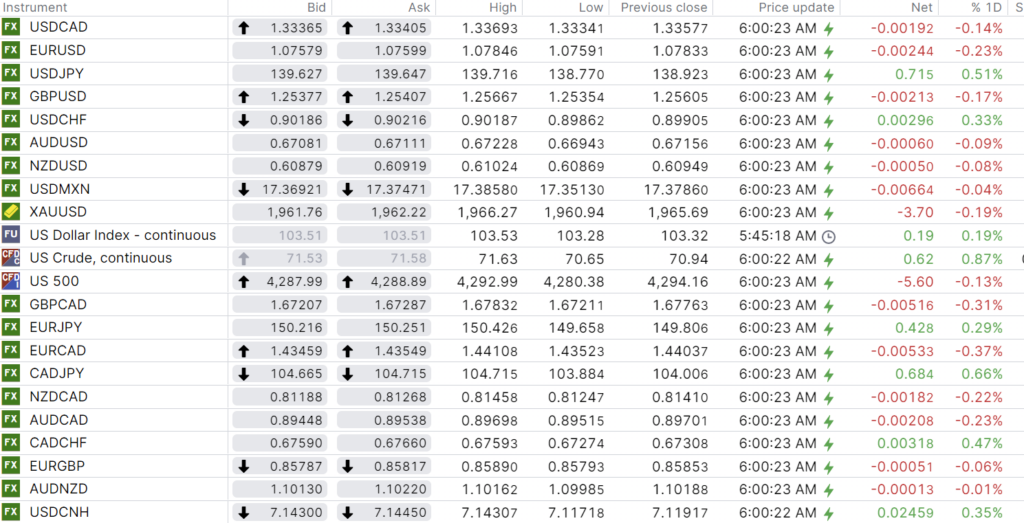

USDCAD Snapshot: open 1.3336-40, overnight range 1.3334-1.3369, close 1.3358

USDCAD bounced inside yesterday’s range. Prices are supported by Wednesday’s surprise BoC rate hike, but the downside was limited by sliding oil prices.

BoC Deputy Governor Paul Beaudry said the rate increase was needed because their forecasts were out to lunch. Not really. He said, “excess demand in the Canadian economy is more persistent than we thought, and this increases the risk that the decline in inflation could stall.” Beaudry also expressed concerns about buyers returning to the housing market despite the rate hikes and the low unemployment rate. He concluded by emphasizing that interest rate risks lean towards the upside.

Those upside risks may have eased slightly after today’s somewhat disappointing Canadian employment report. Canada lost 17,300 jobs in May while the unemployment rate rose to 5.2% from 5.0%. The details suggest the report isn’t all that bad. The number of private and public sector employees rose 22,200, while those self-employed fell 39,000. Nevertheless, USDCAD popped to 1.3357 from 1.3328 on the news.

WTI oil prices fell sharply yesterday, losing over 5% at one point, because of rumours of a US/Iran nuclear deal. The White House denied the story and WTI rose from a low of $69.20/b in the afternoon to $71.63 at the NY open.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish inside a minor downtrend channel between 1.3290 and 1.3390. A break below the bottom targets 1.3250 then 1.3180. A topside move suggests a retest of 1.3460, then 1.3490.

Longer term, the USDCAD downtrend from March is intact while prices are below 1.3630 while the uptrend line from May 2021 is intact above 1.3030.

For today, USDCAD support is at 1.3330 and 1.3280. Resistance is at 1.3380 and 1.3410.

Today’s range 1.3280-1.3380.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Donnie Trump has gotten his comeuppance. The orange-haired narcissist has become the first former president to face criminal charges. It also raises the possibility that if Republican’s win the White House in 2024, Biden will suffer a similar fate.

Ukraine has launched a highly-telegraphed offensive to reclaim its Zaporizhzhia territory, which was seized by Russia during the 2022 invasion. The country is taking decisive action to regain control and restore its territorial integrity.

The RBA and BoC hiked rates because inflation remained stubbornly elevated. Swiss National Bank Chairman Thomas Jordan also chirped about “stubborn inflation” and the need to get it lower, leading to speculation of a 25 bp rate hike on June 22.

The US May inflation data is Tuesday, and it will determine if the Fed skips a rate hike on June 14. Yesterdays rise in weekly US jobless claims boosted the odds to 77.1% (FedWatch tool) for an unchanged outcome.

EURUSD has been trading within a narrow range of 1.0758-1.0785, supported by speculation that the Fed may “skip” a rate hike next week, while the ECB is expected to raise its benchmark rate by 25 bps. With no significant US data available, the market is likely to engage in range trading today, albeit with a slightly bullish bias.

GBPUSD has experienced a trading range of 1.2535-1.2567, largely influenced by the overall sentiment towards the US dollar. Some analysts argue that GBPUSD may be nearing its peak, considering that the market has already factored in the next 100 bps of tightening. Furthermore, renewed demand for EURGBP is expected to exert downward pressure on the currency.

USDJPY has seen a decline from 139.72 to 138.77 due to profit-taking triggered by discussions of a potential “skip” in rate hikes by the Fed, coupled with a decrease in the US 10-year Treasury yield from 3.81% to 3.75% yesterday.

AUDUSD has rallied from 0.6694 to 0.6723 following the release of lower-than-expected Chinese CPI and PPI data. This has led to speculation that the PboC might implement interest rate cuts next week. Additionally, the weakening of the US dollar across the board has provided support to the Australian dollar.

No major US economic reports are scheduled for release today.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

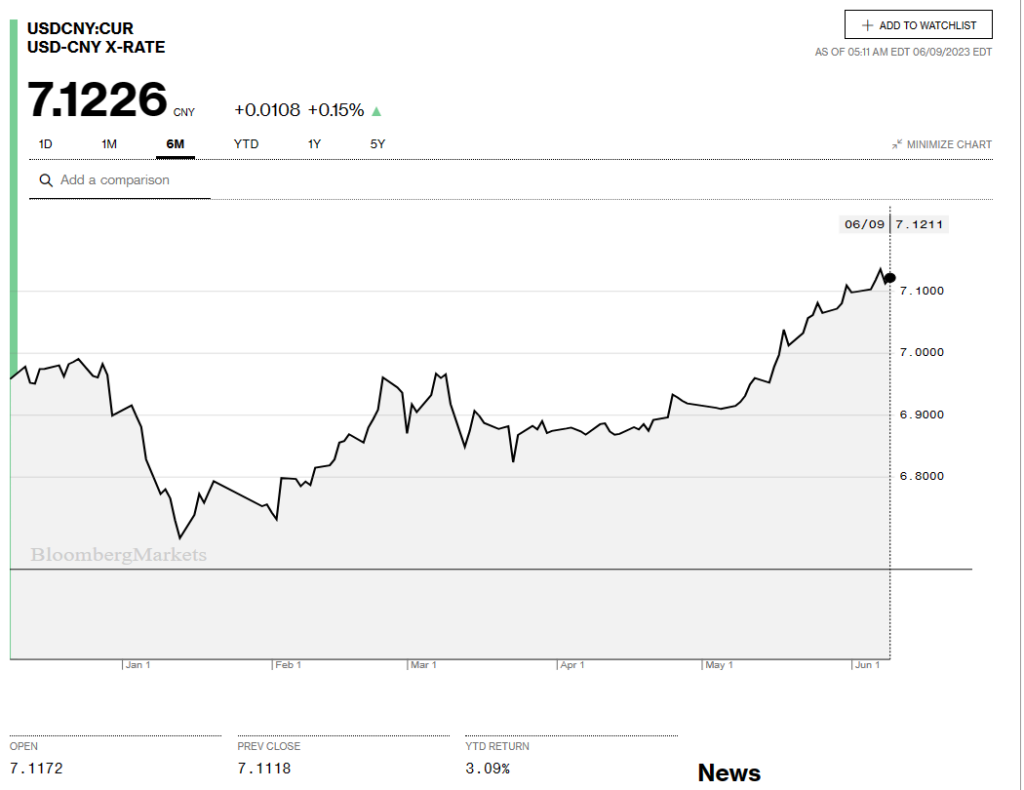

China Snapshot

Bank of China Fix: 7.1115, previous 7.1280

Shanghai Shenzhen CSI 300 rose 0.43% to 3836.70.

May CPI 0.2% y/y (forecast 0.3%, previous 0.1%)

May PPI -4.6% y/y (forecast -4.3%, previous -3,6%) Lower commodity prices behind the drop in PPI.

The low Chinese inflation numbers have analysts speculating that the PboC will cut interest rates as soon as next week.

Chart: USDCNY 6 month

Source: Bloomberg