December 21, 2019

USDCAD open 1.3135-39 (6:00 am EST) Overnight range 1.3124-1.3139

Canadian retail sales fell 1.2% in October. Traders expected a 0.5% gain and took their frustrations out on the Loonie. USDCAD soared to 1.3179 from 1.3142, prior to the news. According to Statistics Canada, “The decline was primarily attributable to lower sales at motor vehicle and parts dealers and at building material and garden equipment and supplies dealers.”

US Q3 GDP rose 1.7% q/q unchanged from the previous result while PCE -Prices were as expected.

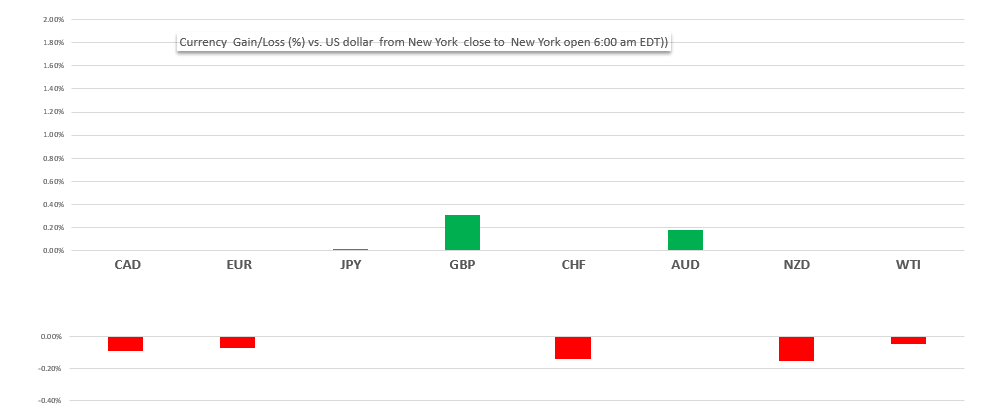

FX markets traded sideways ahead of the Christmas holidays. Drama was kept to a minimum and FX volatility following economic data was muted. The US dollar opened on a mixed note. GBP led EUR and CAD lower, while AUD, NZD, JPY and CHF, notched small gains.

FX Market Snapshot

Change in currency value against the US dollar from NY close to NY open

Source: Saxo Bank/IFXA

GBPUSD was lifted off its overnight low of 1.3009 by higher than expected Q3 GDP growth, which rose 1.1% y/y compared to 1.0% forecast. Prices were further underpinned by an improvement in December Consumer Confidence (actual -11 vs forecast -14) Q3 Business investment was flat. The news lifted GBPUSD to 1.3044 in early New York trading. The Chancellor of the Exchequer announced Andrew Baily would be the next Governor of the Bank of England, effective March 16, 2020. Traders are waiting for the latest UK vote on Boris Johnson’s Brexit plan, today.

EURUSD broke below the bottom of its overnight 1.1115-1.1113 range in New York trading, and hit 1.1087, mostly due to sales of EURGBP. Eurozone economic data wasn’t a factor. The intraday technicals turned bearish with the move below 1.1115, suggesting further losses toward 1.1060.

USDJPY continued to consolidate gains sparked by this week’s rally in US 10-year Treasury yields. They rose from 1.826% last Friday to 1.94% today. November National CPI rose 0.5% y/y, beating forecasts for just a 0.2% increase.

AUDUSD and NZDUSD traded in narrow bands. Both currencies are supported by the recent China/US trade developments.

Oil prices retreated, with WTI oil falling from $61.16 to $60.94 on profit-taking ahead of the weekend. The break of $61.00 snaps the December 12 uptrend line, and a further move below $60.70/b suggests additional losses to $60.30/b. Nevertheless, prices are underpinned by improved global growth prospects following the Phase 1 trade news and Opec production cuts.

USDCAD continues to consolidate losses after falling through 1.3140 support on Wednesday. Firm inflation data and reduced risks for Bank of Canada rate cuts are undermining the currency pair. Today’s weak retail sales data suggests further 1.3100-1.3200 consolidation.

Traders will be watching for today’s US Michigan Consumer Sentiment Index (forecast 92 vs previous 92) to support a “steady as she goes” Fed monetary policy.

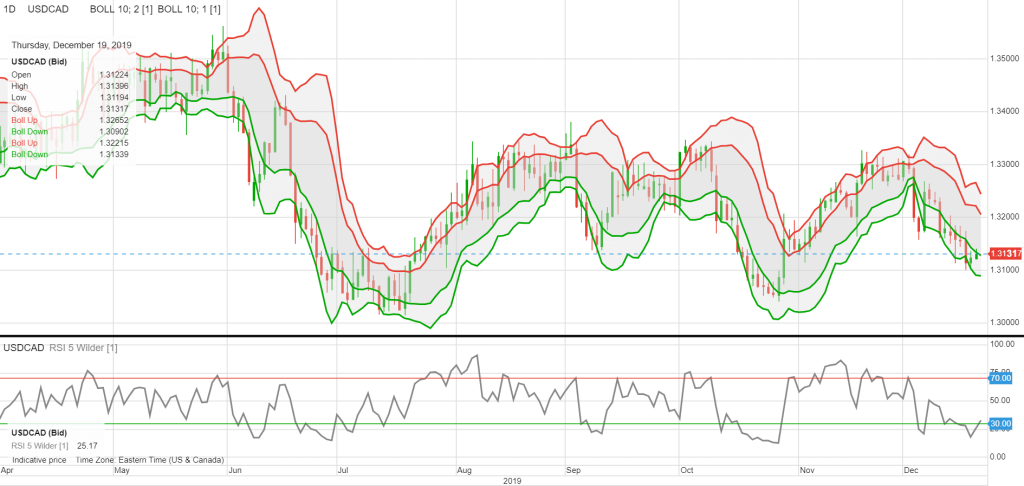

USDCAD Technical View

The intraday technicals are still bearish while prices are below 1.3180. However, support in the 1.3100-05 area was tested yesterday, and it held. Prices have drifted higher but need to break above 1.3180, to negate the downside threat, for the short term. A move above 1.3180 targets 1.3240. Longer term, USDCAD remains in a 1.3000-1.3500 range, and while prices are below 1.3250, the bias is for further weakness. For today, support is at 1.3110 and 1.3090. Resistance is at 1.3180 and 1.3210. Today’s Range 1.3130-1.3210

Chart: USDCAD daily

Source: Saxo Bank