Source: hdclipartall.com

- Canada August GDP unchanged from July

- Equity market sell-off weighs on risk sentiment

- US dollar opens higher across the board compared to close

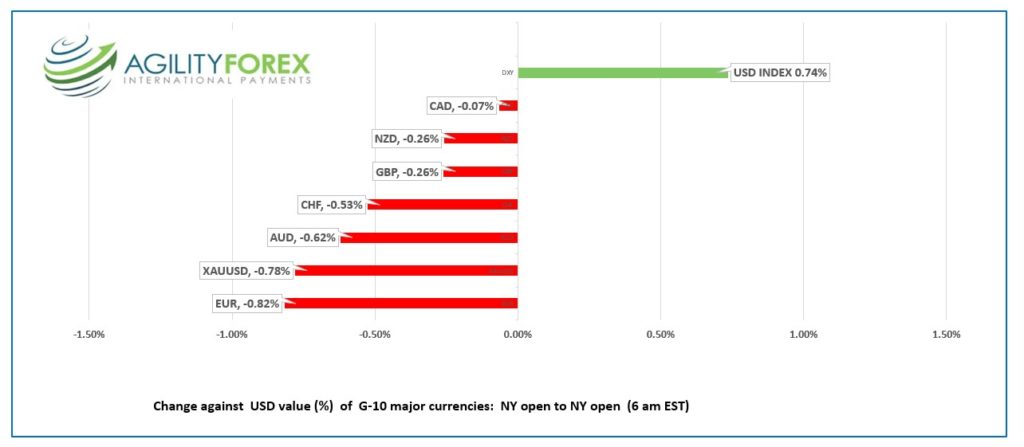

FX at a glance:

Source: IFXA Ltd/RP

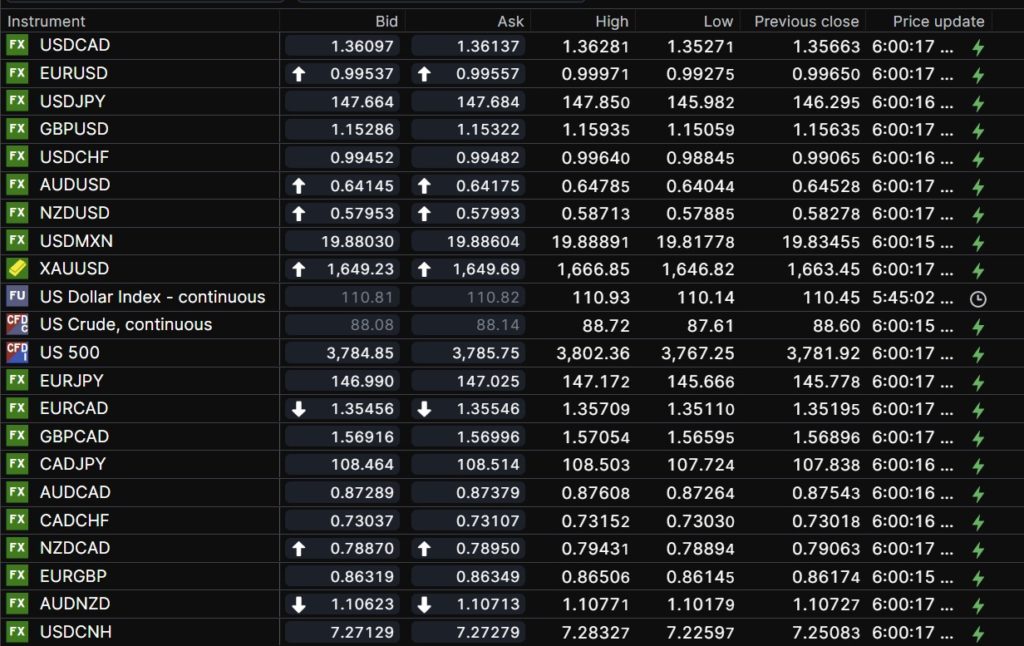

USDCAD Snapshot: open 1.3610-14, overnight range 1.3527-1.3628, close 1.3566

USDCAD direction continues to be at the whim of US dollar sentiment but is underpinned by the BoC’s dovish rate hike on Wednesday. Governor Tiff Macklem tapped the rate hike brakes and surprised markets with a 50 bp bump after hinting that another 75 bps was appropriate.

Statistics Canada wrote, “Real gross domestic product (GDP) edged up 0.1% in August, following a slight (+0.1%) increase in July. Growth in services-producing industries (+0.3%) was partially offset by a decline in goods-producing industries (-0.3%), as 14 of 20 industrial sectors increased in August.”

USDCAD barely budged on the news.

Meanwhile, Fed Chair Jerome Powell, and Vice Chair Lael Brainard have not indicated a pause in hiking US rates, despite market wishes to the contrary. Traders have downgraded the terminal rate for Fed funds from 5.0% a week ago to 4.75% today.

The combination of the dovish BoC and hopes for a Fed rate hike pause have capped USDCAD gains in the 1.3650 area with fears that the Fed pause is merely a pipe dream limiting downside.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3630, looking for a move below 1.3560 to test support in the 1.3490-1.3500 area. A decisive break below 1.3490 sets the stage for a move to 1.3360. A break above 1.3630 targets 1.3660 then 1.3730.

For today, USDCAD support is at 1.3570 and 1.3510. Resistance is at 1.3630 and 1.3660. Today’s range: 1.3550-1.3630

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

You can’t keep the US dollar down or Donald Trump from Twitter. Elon Musk closed the deal for Twitter, fired the CEO and CFO, and if he delivers what he said in May, would reinstate Trump’s Twitter account.

Global markets were choppy, skittish, and digesting a somewhat divided ECB’s dovish rate hike in the face of tech stock turmoil, falling Treasury yields ahead of the usual month-end portfolio rebalancing drama. So, when in doubt, buy US dollars.

Asian equity indexes slumped with selling pressure exacerbated by Amazon predicting sharply lower sales in Q4. Chinese markets were hard hit on speculation of even tighter controls of US technology exports to China, and the Hang Seng shed 3.66%. The Nikkei 225 and ASX 200 indices were down 0.88% and 0.87% respectively.

European bourses opened defensively and are all in negative territory led by a 0.61% drop in th4e German Dax. The firming US dollar knocked WTI and gold prices lower.

The US 10-year Treasury yield fell from 4.07% yesterday to 3.911% in Asia overnight before rallying to 4.006% in NY.

US Personal income increased 0.4% in September and Personal Consumption expenditures rose 0.6% which were higher than expected

Bank of Canada and ECB policymakers proved they were really doves in hawk feathers after both central banks delivered dovish rate hikes.

EURUSD bopped and weaved, chopped, and churned around the release of the ECB policy statement and press conference, managing to rally from 0.9946 to 1.0042, before retreating to close at 0.9965. The single currency traded in a similar fashion overnight but in a 0.9928-0.9997 range, opening in NY at 0.9945. Essentially, the ECB meeting was meaningless for FX traders as long as they took Thursday off.

The ECB raised rates 75 bps as expected but no longer indicated that rate hikes would continue at the next” several meetings.” That wasn’t what traders wanted to hear and bullish EURUSD sentiment evaporated, underpinning the US dollar in the process. There was plenty of Euro area economic data, but it was ignored by FX traders.

GBPUSD dropped from its peak of 1.1594 in Asia to 1.1506 in Europe before rebounding to 1.1538 in NY EURGBP selling pressure have supported GBPUSD. Traders are concerned that the recently delayed but upcoming financial statement will include tax hikes and spending cuts which would worsen the economic outlook.

USDJPY traded in a 145.98-14785 range overnight. The Bank of Japan surprised no one with another dovish monetary policy statement and continues to forecast inflation below 2.0%.

AUDUSD and NZDUSD rallied early in Asia then retreated to session lows in NY due to renewed US dollar demand.

There are a lot of US economic reports today including Personal Income Expenditures price index, Pending Home Sales, and University of Michigan Consumer Sentiment.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

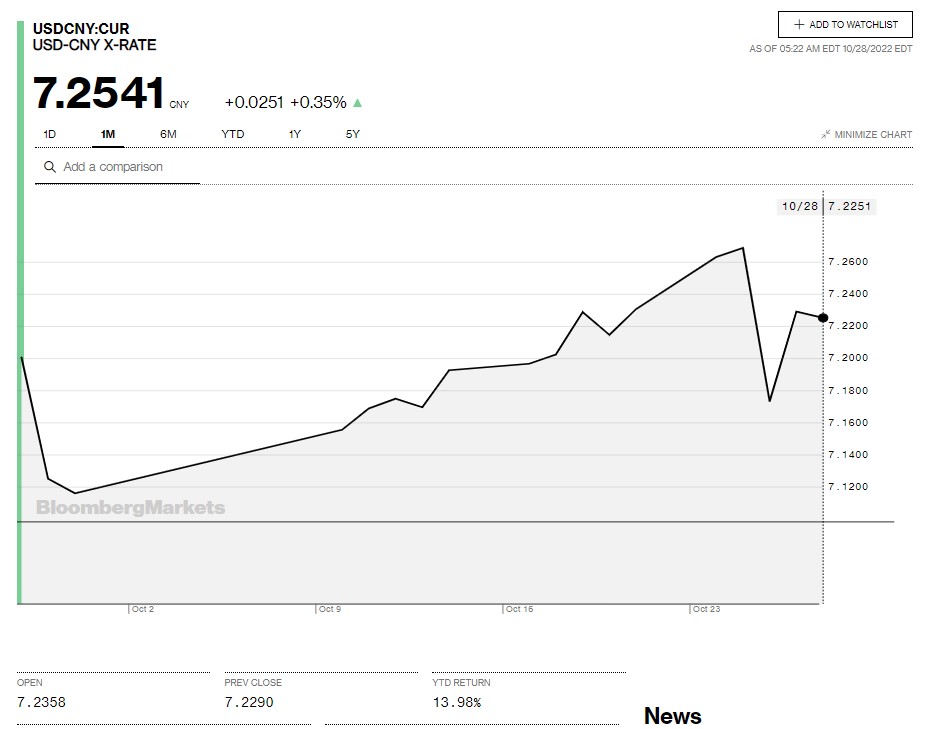

China Snapshot

Today’s Bank of China Fix: 7.1698, previous 7.1570

Shanghai Shenzhen CSI 300 fell 2.47% to 3541.33

Chart: USDCNY 1 month

Source: Saxo Bank