Source: Franks Red Hot

- Canadian inflation hits 30 year peak

- US shoppers return with a vengeance

- US dollar drops as risk aversion fades

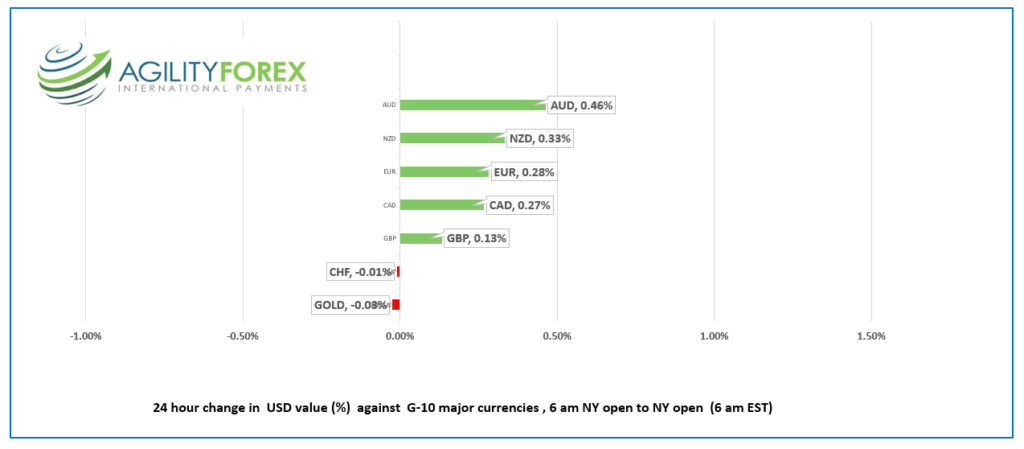

FX at a Glance

Source: IFXA Ltd/RP

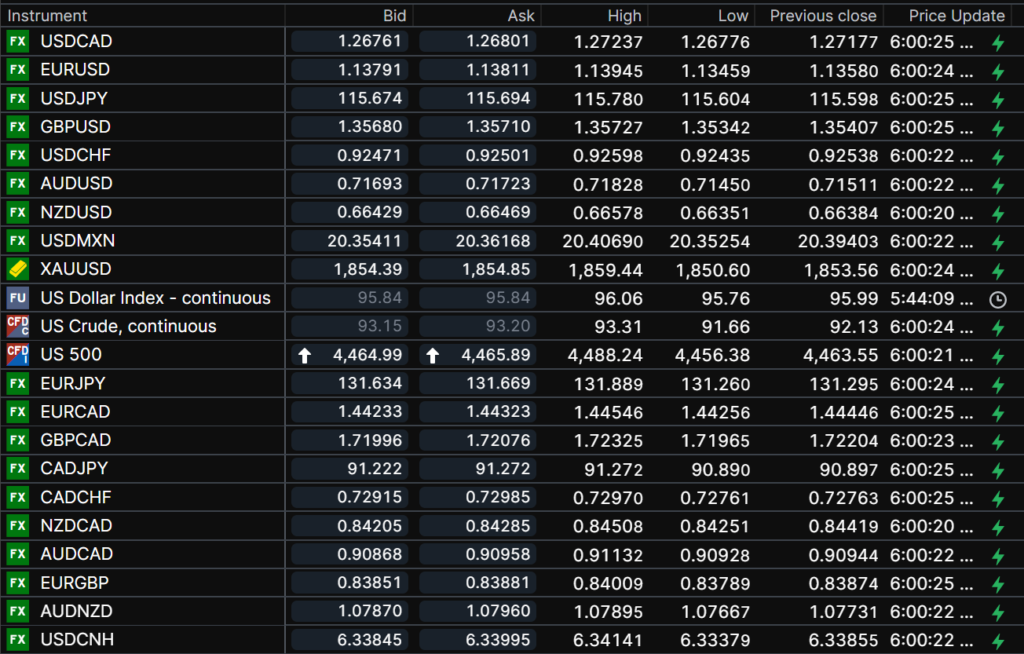

USDCAD Snapshot: Open 1.2681-84, Overnight Range-1.2666-1.2724, previous close 1.2718

USDCAD squeezed modestly lower following the sizzling Canadian inflation report. However, a higher than expected rebound in US January Retail sales shifted the focus to the American interest rate outlook and USDCAD reversed the move.

Statistics Canada said, “Canadian inflation surpassed 5% for the first time since September 1991, rising 5.1% on a year-over-year basis and up from a 4.8% gain in December 2021.” The report noted that “prices rose in all major components on a year-over-year basis, with shelter prices (+6.2%) contributing the most to the all-items increase.

BoC Deputy Governor Timothy Lane speaks about “Central Bank Decision-Making in Turbulent Times.” The previous title, “how to look independent while waiting for FOMC decisions,” was rejected.

USDCAD direction will be at the mercy of Russia and Ukraine headlines and S&P 500 price action.

Technical view: The intraday technicals are bearish with the break below support at 1.2710, targeting 1.2500 if strong support in the 1.2640-50 area gives way. A failure to move below support suggests additional 1.2640-1.2840 consolidation. Longer term, USDCAD has an upward inside a 1.2500-1.3000 range.

For today, USDCAD support is at 1.2640 and 1.2610. Resistance is at 1.2730 and 1.2770. Today’s Range 1.2640-1.2730

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

It is going to be a busy day against the backdrop of simmering geopolitical tensions. Russia may have pulled a few soldiers from the front lines, but President Putin is steadfast in his demand that Ukraine cannot be allowed to join NATO. President Biden continues to stoke tension by saying a Russian invasion of Ukraine is still a possibility.

US Retail Sales are doubled expectations and US import and export prices rose as well. The news adds fuel to arguments that Fed rate hikes need to be aggressive.

This afternoons release of the FOMC minutes may be anti-climatic as a series of policymakers have provided updated outlooks since the January 26 meeting.

EURUSD retreated following the Retail Sales data but remained inside its 1.1345-1.1395 range. Prices are underpinned by the mildly better risk tone and from some slightly hawkish comments from ECB policymakers. Latvia’s Central Bank Governor said a rate hike this year is “likely” while Isabel Schnabel. warned about acting too late on inflation.

Chart: EURUSD 4 hour

Source: Saxo Bank

GBPUSD stayed in its overnight 1.3534-1.3573 range following the US data. Prices are underpinned after UK inflation reached a 30 year peak of 5.5% y/y in January compared to5.4% y/y in December. Headline and core PPI along with the Retail Price Index, were also better than forecast reinforcing calls for a series of BoE rate hikes in 2022.

Chart: GBPUSD daily

Source: Saxo Bank

USDJPY traded dropped to 115.43 following the US data, after peaking at 115.78 in Asia. Safe haven demand for yen due to Russia and Ukraine is helping to cap gains while the US 10 year Treasury yield above 2.0% provides support. BoJ Governor Kuroda justified the Bank’s decision to buy an “unlimited” amount of 0.25% yielding bond because the decision was made amid the “unusual” market situation.

AUDUSD rallied to 0.7182 from 0.7145 on broad US dollar weakness. Prices may have received some support after RBA Deputy Governor Guy Debelle vaguely hinted at higher rates in 2022.

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.3463, previous 6.3605

Shanghai Shenzhen CSI 300 rose 0.39% to 4617.99

Jan CPI 0.9% y/y vs. Exp. 1.0% y/y (Prev. 1.5% y/y), Jan CPI 0.4%m/m vs. Exp. 0.5% (Prev. -0.3%m/m)

Jan PPI 9.1% y/y vs. Exp. 9.5% (Prev. 10.3% y/y

PBoC Governor Yi Gang says he expected economy to return to potential in 2022. He plans to keep an accommodative monetary policy

US Trade Representative says the Phase One agreement did not meaningfully address American concerns with China’s state-led non-market policies

Chart: China 1 month

Source: Saxo Bank