Source: Pixabay

- Chirping by Fed hawks and Fed doves unsettles traders

- Oil slides on recession fears, China covid

- US dollar finishing week on mixed note-CAD lags Antipodeans

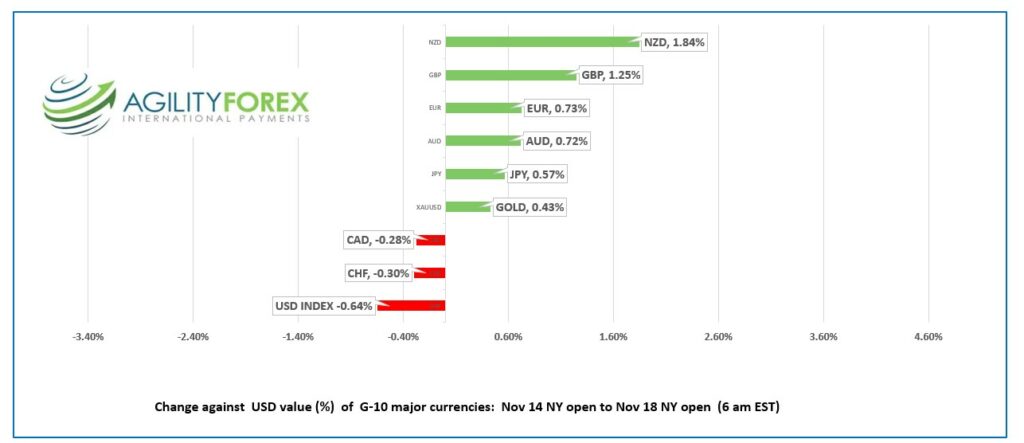

FX at a glance: Change since Monday NY open

Source: IFXA Ltd/RP

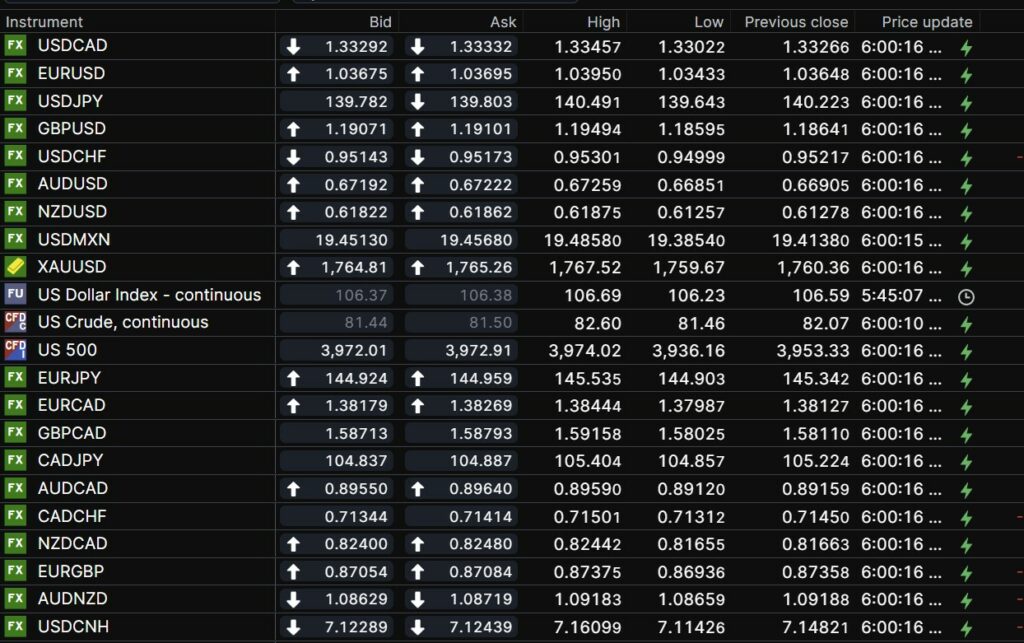

USDCAD Snapshot: open 1.3329-33, overnight range 1.3302-1.3351, close 1.3327

USDCAD continues to do the risk sentiment shuffle-one step backwards, two steps forward. Price action is driven by the S&P 500 index moves with Canadian economic data and Bank of Canada comments mostly dismissed.

USDCAD is underpinned by the slide in WTI oil prices which fell from $89.21/b on Monday to $80.96/b overnight, a 9.2% drop. Oil prices are weighed down by increased US recession ears along with concerns about reduced China demand due to rising covid cases in that country.

Canada Industrial Production and Raw Materials Price index data is ahead, but as usual will not be a factor for traders.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3360, looking for a drop below1.3300 to extend losses to 1.3220. A topside break targets 1.3410, which if broken suggests a retest of 1.3570.

Longer term, the mid-August uptrend line is intact at 1.3220 and Fibonacci retracement levels of the October-November range suggest a move above 1.3390 will extend gains to 1.3680.

For today, USDCAD support is at 1.3290 and 1.3240. Resistance is at 1.3390 and 1.3450

Today’s range 1.3290-1.3390

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

It has been a choppy, volatile week for markets and the US dollar opened Friday with losses compared to Monday. The Canadian dollar and Swiss franc were outliers, losing 0.28% and 0.30% respectively.

The S&P 500 futures are trading at 3973.00, slightly above the mid-point of this week’s S&P 500 range of 3906.54-4028.84.

The US 10-year Treasury yield is 3.801% as of 6:30 am ET and traded in a 3.671%-3.906% range this week.

Contradictory Fed comments were responsible for the bulk of the volatility. The week started on a hawkish note after Fed Governor Christopher Waller pushed back against a rate hike pause saying “we still have a long ways to go. These rates are going to stay — keep going up — and they’re going to stay high for a while until we see this inflation get down closer to our target.”

He had a change of heart Wednesday when he said, “the data of the past few weeks have made me more comfortable considering stepping down to a 50-basis-point hike,” in December and possibly to smaller quarter-point increases after that.”

Uber-hawk St Louis Fed President James Bullard countered Waller’s comments Thursday saying that rate hikes have had only a limited impact on inflation, but market pricing suggests inflation is expected in 2023.

Markets may be better served next week when Fed officials’ mouths are too full of turkey to spout any economic forecasts.

North Korea fired another ICBM missile that landed 200 kilometers off Japan. Traders didn’t care.

EURUSD traded in a 1.0334-1.0395 range. ECB President Christine Lagarde reiterated her promise to bring inflation to the 2.0% medium term target in a timely manner. She warned that the risk of a recession has increased but despite that, rates need to rise higher. The EURUSD technicals are bullish above 1.0250 but need to break resistance in the 1.0500 area to extend the rally.

GBPUSD rallied from 1.1860 to 1.1950 in Europe then slid to 1.1910 in NY. Traders shrugged of yesterday’s UK budget as the major measures were telegraphed in advance. Retail Sales rose 0.6% m/m in October which easily beat Septembers 1.5% decline and helped underpin prices. The GBPUSD technicals are bullish above 1.1790 which if broken targets 1.1500.

USDJPY traded in a 139.64-140.49 band. Prices dropped from the peak to the low in Asia following the news of the North Korean missile, then chopped about in that range before opening in NY at 139.80. Japan’s October CPI surged to 3.7% y/y compared to the 2.7% expected.

NZDUSD rallied from 0.6126 to 0.6187 in anticipation that the RBNZ raises rates by 75 bps next week. AUDUSD gains lagged the NZDUSD performance, rising from 0.6685 to 0.6726.

There are only second-tier US economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

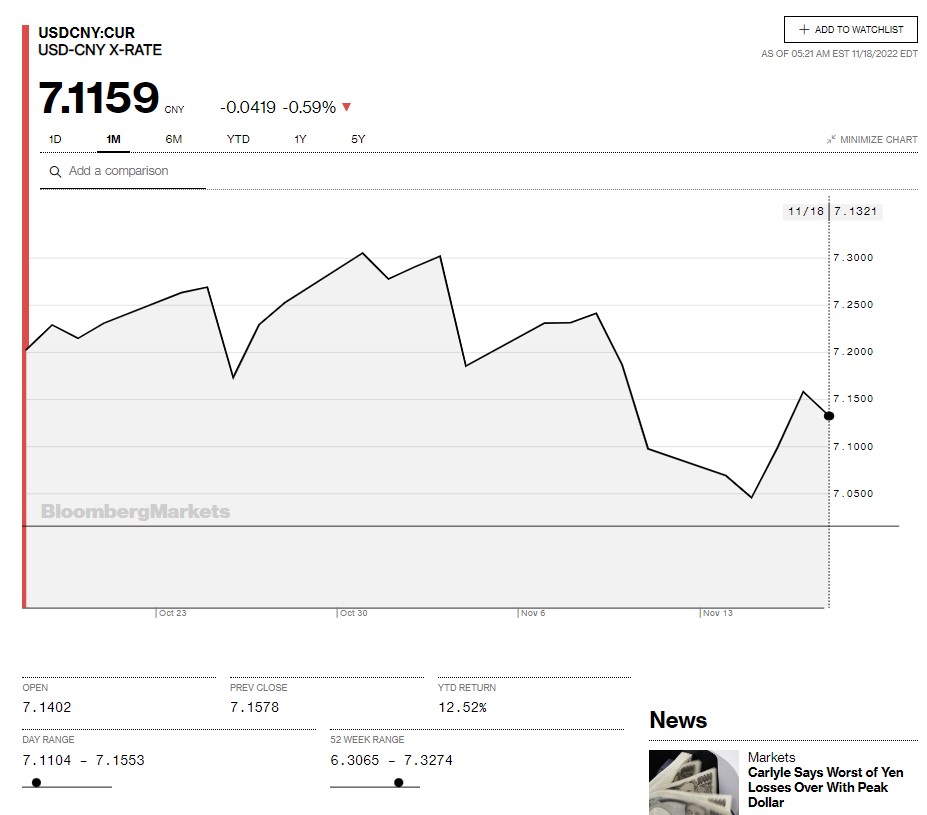

China Snapshot

Today’s Bank of China Fix: 7.1091, previous 7.0655

Shanghai Shenzhen CSI 300 fell 0.45% to 3801.57

China new daily Covid cases rise above 24,000.

China National Health Commission told local authorities to avoid “irresponsible loosening” of covid restrictions, which should put the “China easing pandemic restrictions” story to rest, for the time being.

Chart: USDCNY 1 month

Source: Bloomberg