Source: Pixabay

- Rising covid cases and protests in China spook markets

- Global equity indexes start week with small losses

- US dollar gets a safe-haven boost

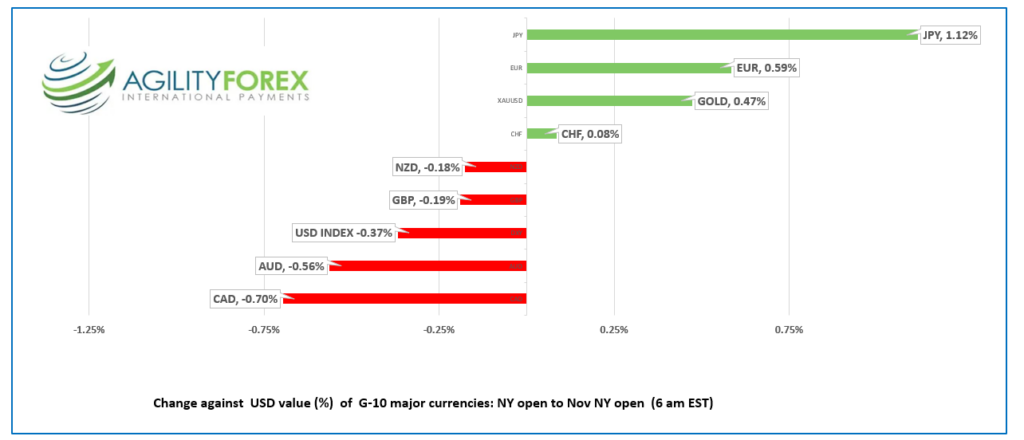

FX at a glance:

Source: IFXA Ltd/RP

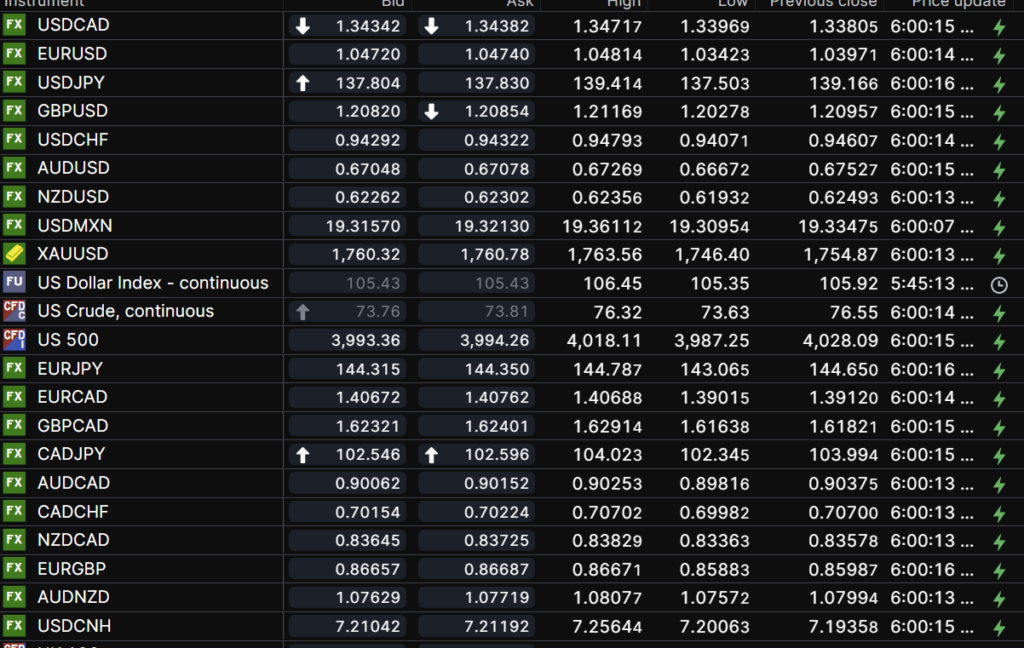

USDCAD Snapshot: open 1.3434-38, overnight range 1.3397-1.3472, close 1.3381

USDCAD jumped on fresh risk aversion due to both civil unrest and rising covid cases in China. China is dealing with demonstrations in many cities as people are sick and tired of Xi Jinping’s restrictive covid policies.

USDCAD got an added lift from sharply lower WTI oil prices which dropped from $82.15/barrel last Tuesday to $73.63/b overnight. The prospect of fresh crude supply from Venezuela and weaker demand from China is weighing on prices.

The price action will be choppy, but range bound ahead of Fed Chair Powell’s speech on Wednesday and the US and Canadian employment reports Friday.

USDCAD Technical outlook

The intraday USDCAD technicals are modestly bullish after break above 1.3410 overnight and looking for a break above 1.3490 to extend gains to 1.3570. A move below 1.3400 targets 1.3360 then 1.3310

Longer term technicals are unchanged from Friday. The USDCAD uptrend from June 2021 is intact while prices are above 1.2780, while the downtrend from October 2022 is intact below 1.3540.

For today, USDCAD support is at 1.3390 and 1.3360. Resistance is at 1.3490 and 1.3530.

Today’s range 1.3390-1.3470

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FX and equity markets started the week on the defensive, hampered by the directionless and mixed close from US markets on Friday.

Risk aversion sentiment is running rampant. But those fears are not expected to hamper Cyber-Monday sales. Analysts are prediction the week en and cyber-Monday sales will top $9.0 billion, on the heels of the $9.12 billion spent on “Black Friday.”

Asian markets were unnerved by news of mass anti-Covid restriction protests in China amidst another spike in new daily cases to 40,052. The protests are hitting close to home for Apple (AAPL:NASDAQ) as it is expected to lose production of 6 million iPhones or about $7.2 billion in revenue.

Traders are ignoring escalating missile attacks by Russia on Ukraine with leaders such as UK’s Rishi Sunak saying,“We will stand with Ukraine for as long as it takes.” Ukraine President Zelensky would prefer less standing and more shooting.

Asian equity makrets closed with losses and European bourses are in negative territory led by a 0.88% drop in the German Dax. S&P 500 futures are down 0.53%, while WTI oil lost 3.13% since Friday’s close.

EURUSD dipped in Asia then rallied from 1.0342 to 1.0496 underpinned by hawkish comments from ECB officials. Dutch central bank President Klaas Knot suggested that rate hikes will continue despite recession risks. Traders are awaiting Wednesday’s German and ECB inflation reports.

GBPUSD bounced in a 1.2028-1.2117 band despite some concerns GBPUSD is may be due for a correction. Some analysts are suggesting that the BoE peak interest rate pricing is too high.

USDJPY slid from 139.41 in Asia to 137.50 in Europe befor grinding back to 138.29 in NY. USDJPY dropped on widespread safe-haven demand for yen on news of the China unrest then bounced after the USD 10-year Treasury yield from 3.622% to 3.676% in NY.

AUDUSD gapped lower at the Asia open, falling from Friday’s close of 0.6753 to 0.6668 due to civil unrest in China and rising covid cases in that country. Weaker than expected Australian Retail Sales numbers didn’t help sentiment (acutal-0.2% m/m vs forecast 0.5% and September 0.6%).

The Dallas Fed Manufacturing Business Index (2nd tier data) is due.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

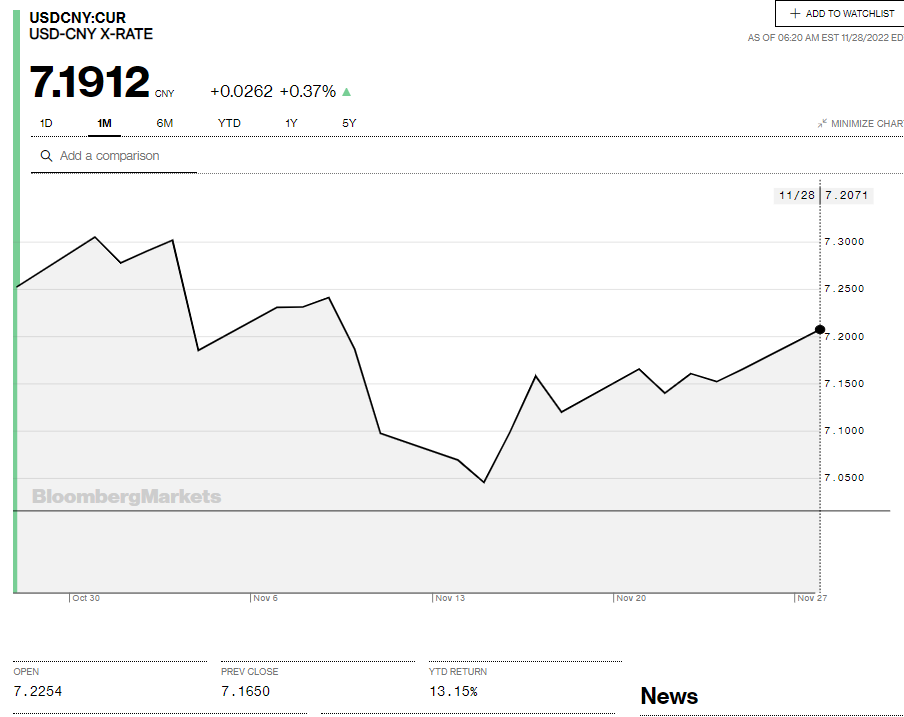

China Snapshot

Today’s Bank of China Fix: 7.1617, previous 7.1339

Shanghai Shenzhen CSI 300 fell 1.13% to 3733.24

China records 40,052 new Covid cases. Nevertheless, Chinese citizens have had enough with lockdown and other restrictions and are protesting in major cities.

In case you missed it: – PBoC cuts Reserve Requirement Ration by 25 bps, effective December 5 which is expected to release CNY 500 billion of long-term liquidity. PboC says weighted average for the RRR of financial institutions is 7.80%

Chart: USDCNY 1 month

Source: Bloomberg