Picture: Pixabay

- Turkey central bank slashes rates by 1.0% to cool inflation

- Weekly jobless claims as expected; Philly Fed higher

- US dollar opens lower, CAD underperforms

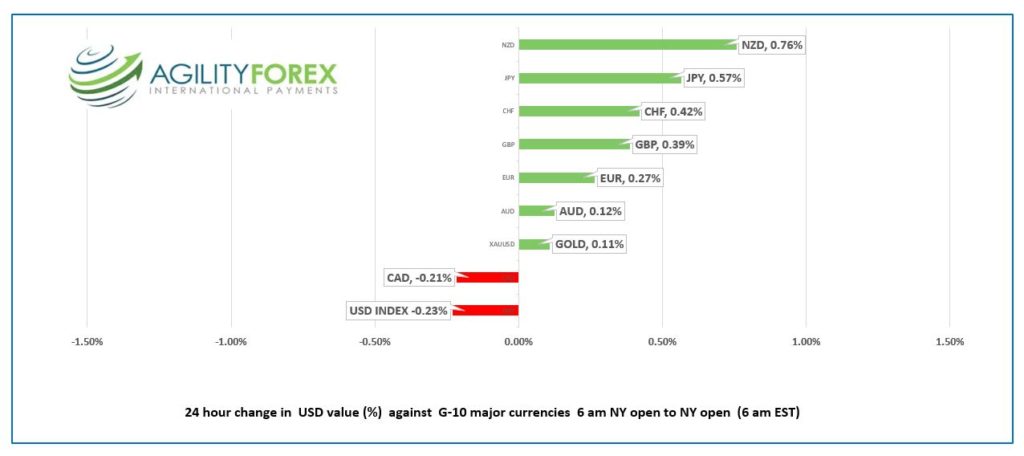

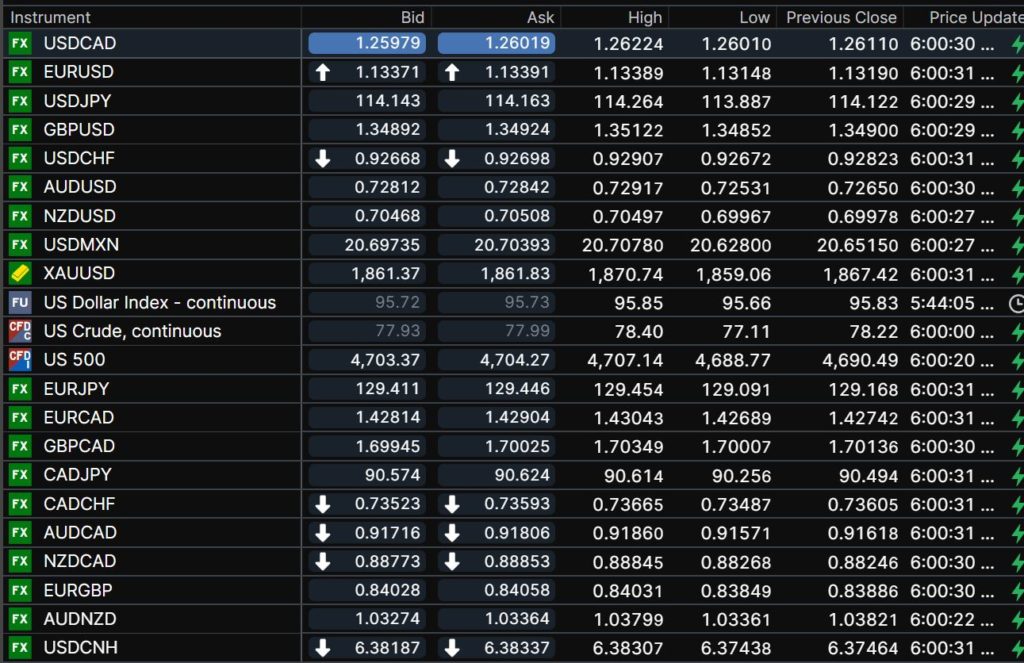

FX at a Glance:

Source: IFXA Ltd/RP

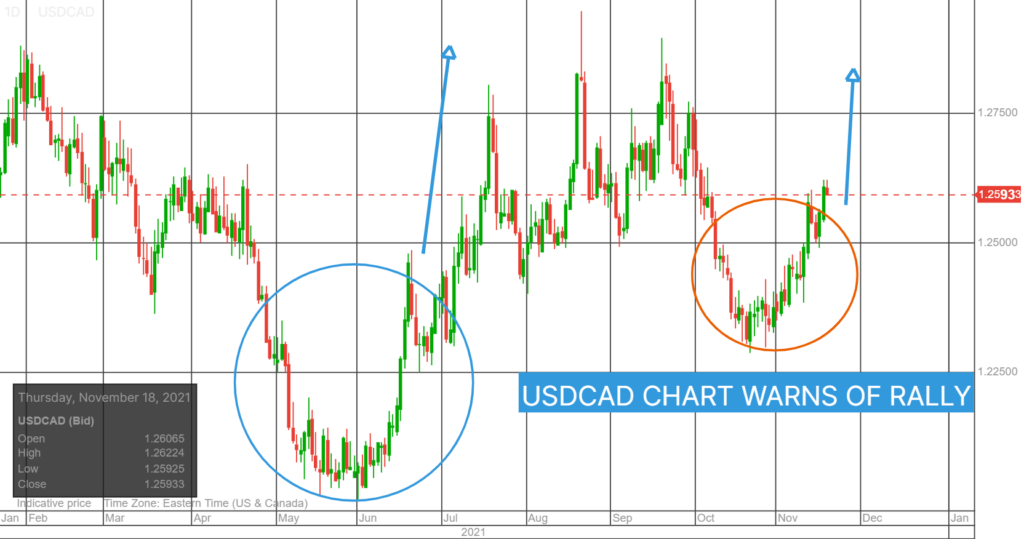

USDCAD Snapshot Open 1.2598-02, Overnight Range 1.2601-1.2622, Previous close 1.2611

USDCAD failed to benefit from data showing inflation rising to a near 20-year peak. Canada headline CPI rose 4.7% as expected and USDCAD rallied from 1.2548 pre-data to 1.2620 by the afternoon and closed at 1.2611.

The inflation data doesn’t jive with Central Bank reality. The BoC’s preferred measures of core inflation (trim. Medium, and common) were unchanged from September. BoC governor Macklem and Deputy governor Schembri delivered somewhat dovish messages this week which seemed to show policymakers remained unconcerned about soaring inflation.

The USDCAD rally was exacerbated by falling oil prices as WTI dropped from $80.24/barrel to $77.11/b in Europe overnight. Oil traders are spooked by IEA and Opec forecasts predicting markets will soon be oversupplied and talk that China and the US will release oil from Strategic Petroleum Reserves.

There are not any domestic economic reports of note on tap today, so USDCAD direction will be determined by oil price action, equities, and broad US dollar sentiment.

Technical view: The intraday USDCAD technicals are bullish. The break above 1.2520, followed by a move above 1.2605 suggests further gains to 1.2670 and 1.2760, which represent the 61.8% and 76.4% Fibonacci retracement levels of the September 20-October 20 range. The daily chart also suggests that a “cup and handle” formation is nearly complete which points to gains toward 1.2900.

For today, USDCAD support is at 1.2570 and 1.2530. Resistance is 1.2630 and 1.2670. Today’s range 1.2560-1.2640

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

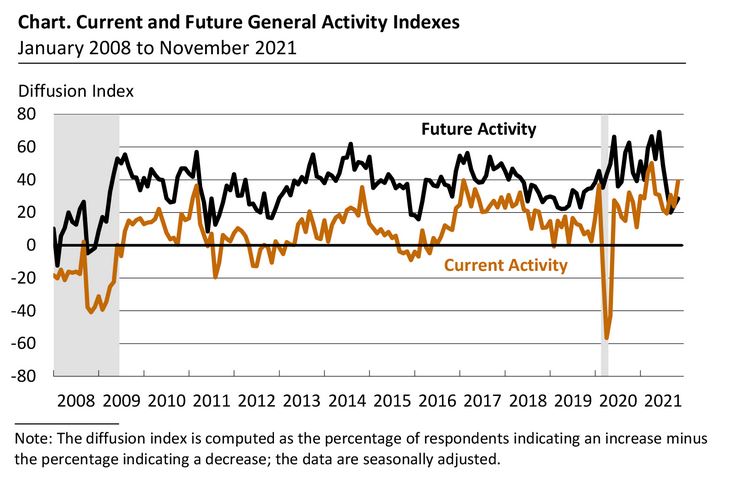

US weekly jobless claims were 268,000, virtually unchanged from the week before and the lowest level since March 14, 2020. The Philadelphia Fed Manufacturing Survey rose 15 points to 39.

Source: Philadelphiafed.org

The US dollar gave back some of this week’s gains in the overnight session, which was uneventful unless you had an interest in Turkish Lira and or Turkish interest rates. That’s because Turkish President Recep Erdogan insisted that the central bank cut interest rates to combat inflation, contrary to conventional wisdom. The Central Bank of Turkey complied and cut the one-week repo rate to 15% from 16%.

Asia equity traders followed Wall Streets lead and the major indexes closed in the red. Hong Kong’s Hang Seng Index seriously underperformed, losing 1.29% on talks of more regulatory interference in China. European indexes are mixed, and close to unchanged while S&P 500 and DJIA futures have ticked higher. Oil and gold prices are lower, and US the 10-year Treasury yield is steady at 1.605.

The US dollar continues to be underpinned by expectations for higher US interest rates sooner than previously expected. Chicago Fed President Charles Evans chimed in with his view that tapering will end in the middle of 2022, and that’s when the Fed will start thinking about raising rates. However, traders are expecting rate hikes sooner than that.

EURUSD drifted higher overnight, rising from 1.1319 to 1.1349, probably due to profit-taking as there were not any other catalysts for the gain. EURUSD sentiment is bearish due to expectations the ECB will significantly lag the rest of the G-7 in raising interest rates. Gains may be limited as Germany is expected to announce new COVID-19 restrictions today. The intraday technicals are bearish below 1.1350.

GBPUSD rallied in a 1.3490-1.3512 range and snapped a two-week downtrend with the move above 1.3440 yesterday. Prices continue to be supported by expectations for the BoE to raise rates in December. They got an added boost from news of progress in the EU/UK talks about the Northern Ireland border.

USDJPY topped out at 115.00 yesterday, and prices consolidated in a 113.89-114.26 range overnight. USDJPY is supported by steady to firm US Treasury yields. The Japanese government announced a $488 billion stimulus plan which was a tad higher than expected.

NZDUSD sharply outperformed against AUDUSD after NZ Q4 q/q inflation expectations were sharply higher than expected, rising to 2.96% from 2.27% previously. Traders now expect more aggressive tightening by the RBNZ.

Chart of the Day: USDTRY (Turkish Lira)

Source: Yahoo Finance.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

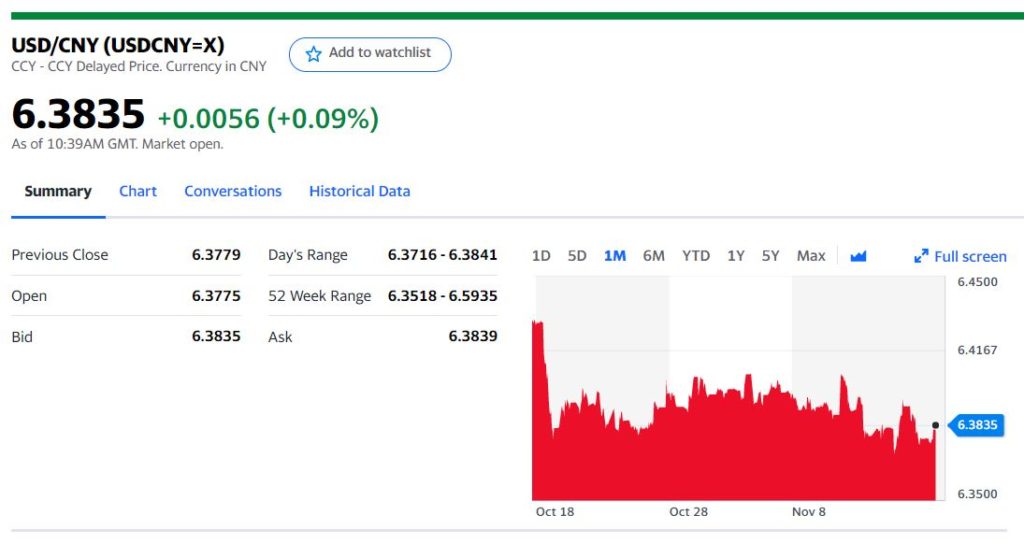

China Snapshot

Today’s Bank of China Fix 6.3803 Previous 6.3935

Shanghai Shenzhen CSI 300 fell 0.99% to 4,837.62

Biden/Jinping to have frequent talks over next four months

Chart: USDCNY 1 month

Source: Yahoo Finance