Image by DALL-E

December 6, 2023

- BoC will leave rates unchanged today.

- ADP employment change weaker than forecast.

- US dollar opens with small gains compared to Tuesday.

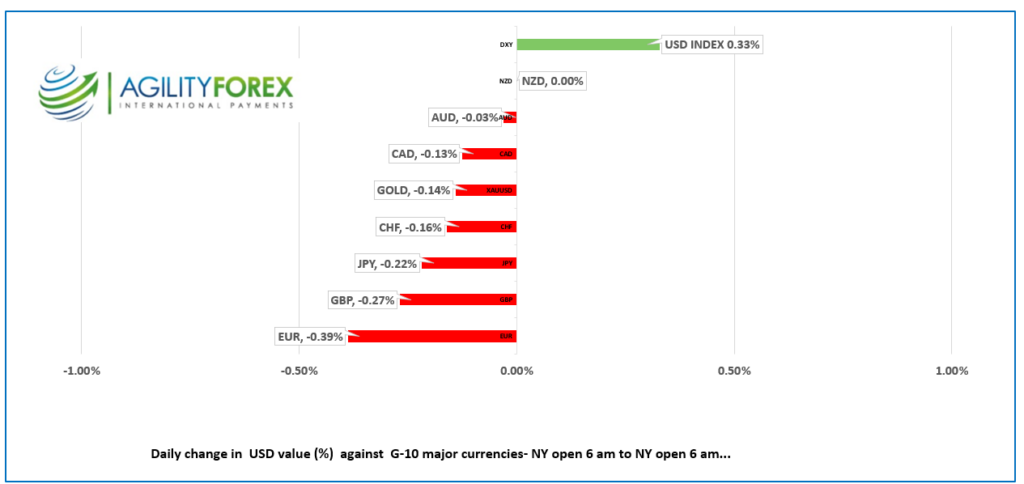

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3578-82, overnight range 1.3558-1.3595, close 1.3593

USDCAD drifted aimlessly in a narrow range with price action tracking US dollar sentiment ahead of this mornings Bank of Canada monetary policy statement.

The BoC is widely expected to leave rates on hold today. It is almost a certainty mainly because if the BoC was to announce a change, either higher or lower, Governor Tiff Macklem would defend the decision in person. But he isn’t having a press conference today, making the odds for a rate change, not quite none, but extremely slim. Expect hawkish guidance warning that higher interest rates are a possibility. If so, it will be ignored as recent economic data, and mortgage renewal risks mean rate hikes are history.

Opec’s credibility has sprang a leak. The cartel announced production cuts would be increased to 2.3 million bpd effective January 1, expecting a nice bump in prices. Instead it was their wallets that got bumped. WTI prices have dropped 9.4% since the announcement.

USDCAD Technicals:

The intraday USDCAD technicals are bullish while trading above 1.3540 and looking for a break above 1.3630 to extend gains to 1.3660. However, unless 1.3660 is broken decisively, the rally is merely a correction.

The USDCAD downtrend is intact below 1.3750 area which is meeting some resistance from the 100 day moving average in the 1.3570 area with the 200 day moving average sitting at 1.3502

For today, USDCAD support at 1.3530 and 1.3490. Resistance is at 1.3620 and 1.3660. Today’s range 1.3530-1.3630

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Yesterday’s JOLTS job openings survey delivered a wake-up call to the last vestiges of US interest rate hawks after it revealed that job vacancies had plunged to their lowest since 2001.

Today’s ADP employment change data drove the point home. ADP reported just 103,000 new jobs, well below the forecast of 130,000, and lower than last month’s downwardly revised 106,000 result.

Nevertheless, the ADP data track record for predicting NFP results is poor, so today’s results will only have a minor impact on trading.

FX markets are likely to remain rangebound until the FOMC meeting on December 13. The Fed will likely leave rates unchanged but talk tough to downplay rate cut expectations.

Bond traders are convinced that US rates have peaked. The US 10-year Treasury yield has given up all its gains since the beginning of September, reaching 4.171% yesterday and then dropping to 4.144, post ADP.

Asian equity indexes jumped aboard the rally bus with Japan’s Nikkei 225 index soaring 2.04%, while Australia’s ASX 200 gained 1.65%. European bourses are also posting gains, but to a lesser extent. The German Dax index is leading the pack higher with a 0.63% gain, while S&P 500 futures are up 0.35% as of 6:00 am PT.

EURUSD is see-sawing in a 1.0772-1.0802 band. Traders ignored the minor improvement in Euro area Retail Sales (actual 0.1% y/y in October vs forecast 0.2% m/m). FX trading is trading in a subdued manner with NFP and the FOMC meeting looming in the background.

GBPUSD is in the middle of its 1.2581-1.2614 band as soft UK Construction PMI (actual 45.5 in November vs forecast of 46.3 and October’s 45.6) acting as a drag on gains.

USDJPY slipped from close to its session peak following the ADP data, after trading in a 146.90-147.52 range overnight. USDJPY is in a downtrend channel between 144.30 and 147.90.

AUDUSD shuffled in a 0.6569-0.6627 band as weaker than expected Q4 GDP (actual 0.2% q/q vs forecast 0.4%) suggested that the RBA’s next move will be to cut rates.

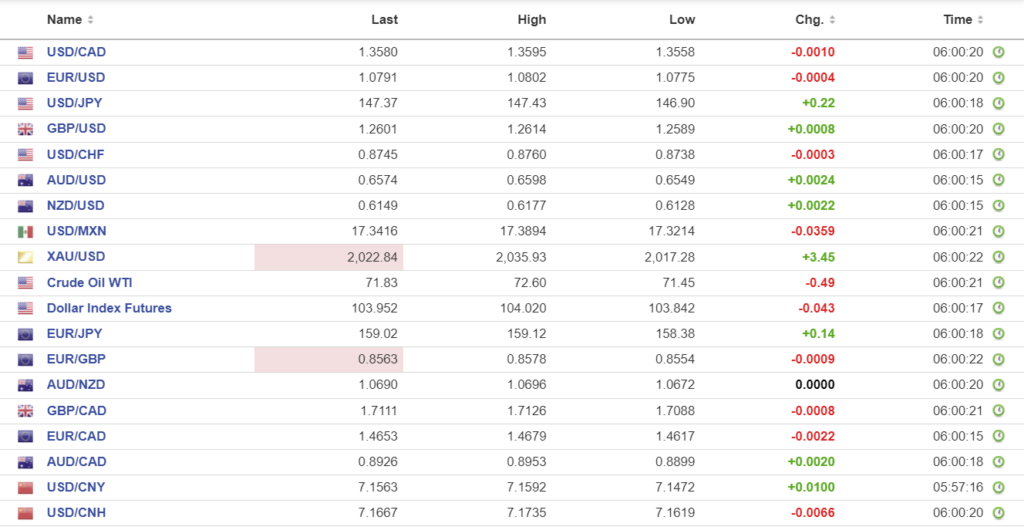

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1140, expected 7.1476, previous 7.1127.

Shanghai Shenzhen CSI 300 rose 0.16% to 3399.60.

Reuters reported that Chinese stat-owned banks intervened and sold USDCNY.

Chart: USDCNY and USDCNH

Source: Bloomberg