January 26, 2024

- Core-PCE inflation rises just 2.9% (forecast 3.0)

- Countdown to FOMC meeting begins.

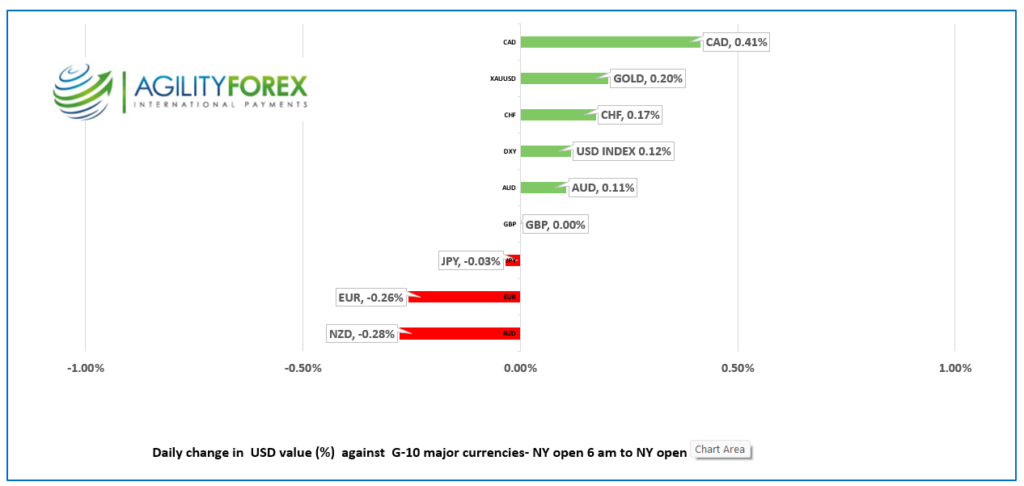

- US dollar rangebound-CAD outperforming.

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3447-51, overnight range 1.3415-1.3484, close 1.3477.

USDCAD rejected yesterday’s attempt to blow through resistance at 1.3556 after traders decided that improved global risk sentiment trumped divergent US and Canada economic growth paths. The American economy is robust, while the Canadian economy is stagnant. This mornings US PCE data showed inflation cooling more than anticipated which sparked additional USDCAD selling in anticipation that the Fed will be forced to cut rates sooner than they wanted. However, robust Q4 GDP growth seen yesterday, may temper the Fed’s enthusiasm. It’s a coin flip.

Firm oil prices may have also weighed on USDCAD, but the WTI rally appears to have stalled due to weak economic growth in China.

The UK suspended negotiations with Canada partly because of dairy quotas. The Canadian government has artificially boosted dairy costs for all Canadians by limiting imports in an effort to protect the Liberal voting Quebec dairy industry led by Saputo Inc. and Agropur Cooperative. The American government is also contesting the dairy quotas under the USMCA trade agreement.

USDCAD Technicals:

The intraday USDCAD technicals are bearish below 1.3490 (hourly chart) and the break below 1.3430 risks further losses to the 1.3350 area. The negative sentiment is encouraged following the move below the 50% Fibo retracement of the January range (1.3507) and the break below the 200 day moving average at 1.3470. A topside break suggest a retest of 1.3550.

Longer term, USDCAD just broke the January uptrend line at 1.3440 and if sustained, the focus will shift to the 1.3250 area. after its attempt to break out above 1.3550 failed yesterday.

For today, USDCAD support is at 1.3410 and 1.3370. Resistance is at 1.3470 and 1.3510. Today’s range is 1.3410-1.3490

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

The US economy was much stronger in Q4 than expected, and that stoked “soft landing” furor, which has been reinforced by today’s Core Personal Consumption Expenditures Price (PCE) index data. Core PCE rose 2.9% y/y (forecast 3.0% and 3.2% in November). Strong growth and falling inflation should encourage the Fed to reduce rates. However, it is a bit of a conundrum for FX traders. Do they buy US dollars due to strong economic growth or sell them because of an improvement in global risk sentiment and narrowing interest rate spreads. That question explains the mixed performance of the greenback since yesterday’s open.

The FOMC meeting is on Wednesday, which suggests markets will be choppy but range-bound as traders adopt a more cautious stance.

Asia equity indexes closed lower, with the Hong Kong Hang Seng index losing 1.60%, while Japan’s Nikkei 225 index fell 1.34%. Australian markets were closed. European bourses are perky. The French CAC 40 index is up 2.16%, and the UK FTSE 100 has gained 1.43%. S&P futures traders are less positive, and the index is flat.%. The US 10-year Treasury yield ticked down to 4.118% after closing at 4.132%.

EURUSD chopped about in a 1.0813-1.0901 range, with the low being seen after German GfK consumer confidence survey data fell more than expected (actual -29.7 vs. forecast -24.5). The ECB left rates and monetary policy unchanged, and according to President Christine Lagarde, said any discussion on rate cuts was “currently premature.” The EURUSD uptrend is intact while prices are above 1.0800, with a break above 1.0930 targeting 1.1000.

GBPUSD is at the top of its 1.2675-1.2759 band, following the PCE data and garnering additional support by EURGBP selling after the ECB did not aggressively push back against speculation of an April rate cut. Traders have priced in an 80% change that ECB rates will fall by 25 bps while UK rates may remain unchanged.

USDJPY chopped in a 147.491148.09 range. The minutes from the BoJ’s December 19 meeting revealed members saw a “need to continue deepening discussions on issues such as the timing of an exit from the current monetary policy and the appropriate pace of interest rate hikes thereafter.” But Tokyo inflation data muddied those waters. Core-CPI rose just 1.6% (forecast 1.9% and November 2.1%) and may delay any BoJ monetary policy moves.

AUDUSD traded quietly in a 0.6576-0.6597 band, with volumes lower than usual as Australia was closed for Australia Day. Prices rose to 0.6619 in NY , post PCE,

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1074, expected 7.1733, previous 7.1044.

Shanghai Shenzhen CSI 300 fell 0.27% to 3333.82.

Chart: USDCNY and USDCNH daily

Source: Investing.com