June 10, 2024

- EU Right-wing parties crush Greens.

- FOMC dot-plot and US CPI are key this week.

- US dollar keeps Friday’s gains.

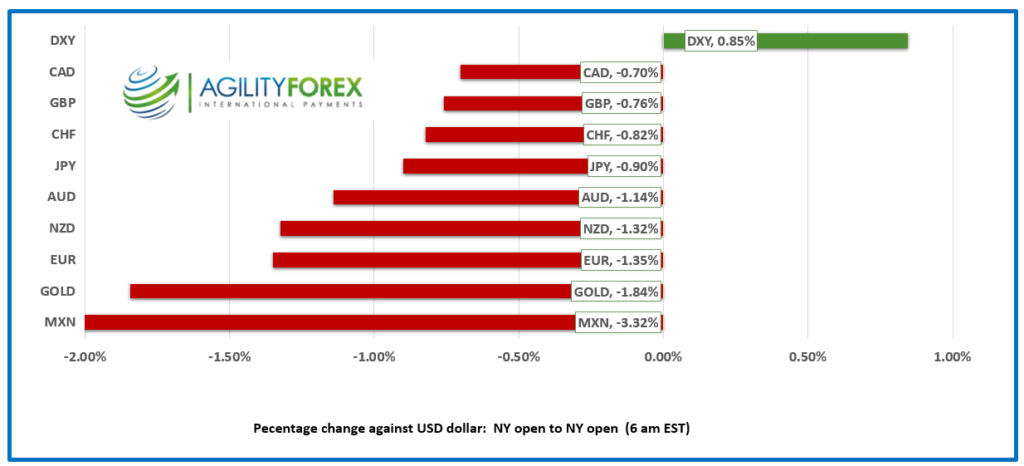

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3779, overnight range 1.3756-1.3779 close 1.3768

USDCAD rallied after Friday’s nonfarm payrolls report suggested the Fed would not be motivated to ease monetary policy any time soon. Traders ignored the Canadian jobs data (actual 27,700, forecast 22, 500, April -90,400) and rightly so as all the gains were part-time jobs, hardly evidence of a robust, job-creating economy. The CAD/US 10-year yield spread has widened to -94.3, in favour of the US, which is also underpinning USDCAD.

USDCAD is not getting any support from oil prices. WTI traded in a 75.27-76.00 range overnight due to increased middle east tensions but gains were limited du to Opec’s previously announced plans to begin phasing out oil production cuts starting in October.

The US and Canadian economic calendars are empty.

USDCAD Technicals

The USDCAD intraday technicals are bullish above 1.3750, looking for a decisive break above the 1.3790-1.3810 area to extend gains to 1.3850. A move below 1.3830 suggests a retest of 1.3710.

Longer term, Friday’s rally above 1.3710 snapped the downtrend line that had guided prices lower since May 16 and has hung a target on the 1.3850 area. A topside break would extend gains to 1.3900.

For today, USDCAD support is at 1.3740 and 1.3710. Resistance is at 1.3810 and 1.3850. Today’s range is 1.3740-1.3820.

Chart: USDCAD daily

Source: DailyFX

Wake-Up Call

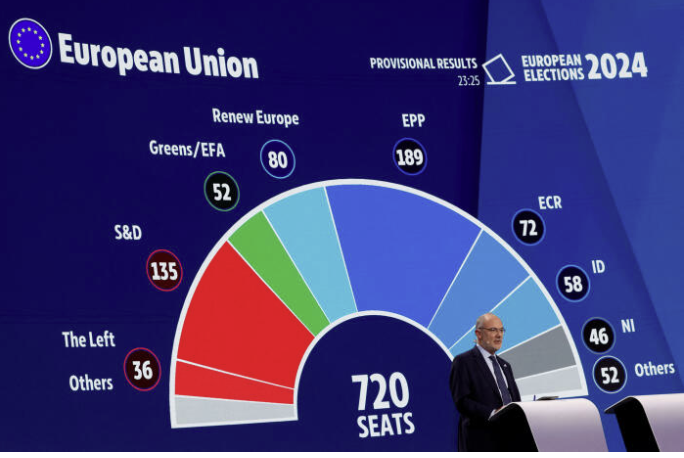

German and French Woke woke up to find that voters in both countries did not like them very much. The EU Parliament Green Party lost 28% of its seats as voters turned to populist parties (a populist party is any party more popular than a socialist party) like Marine Le Pen’s National Rally in France, Italy’s Brothers of Italy Group led by Italian Prime Minister Giorgi Meloni, and in Germany, Chancellor Olaf Scholz’s Social Democrats were thoroughly spanked. The results spooked equity traders. The French CAC-40 index plunged 2.18% while the German DAX fell 0.99%.

French President Macron called a snap election after his party’s humiliating loss, and pundits are speculating that Mr. Scholz’s coalition government will collapse long before the 2025 elections are due

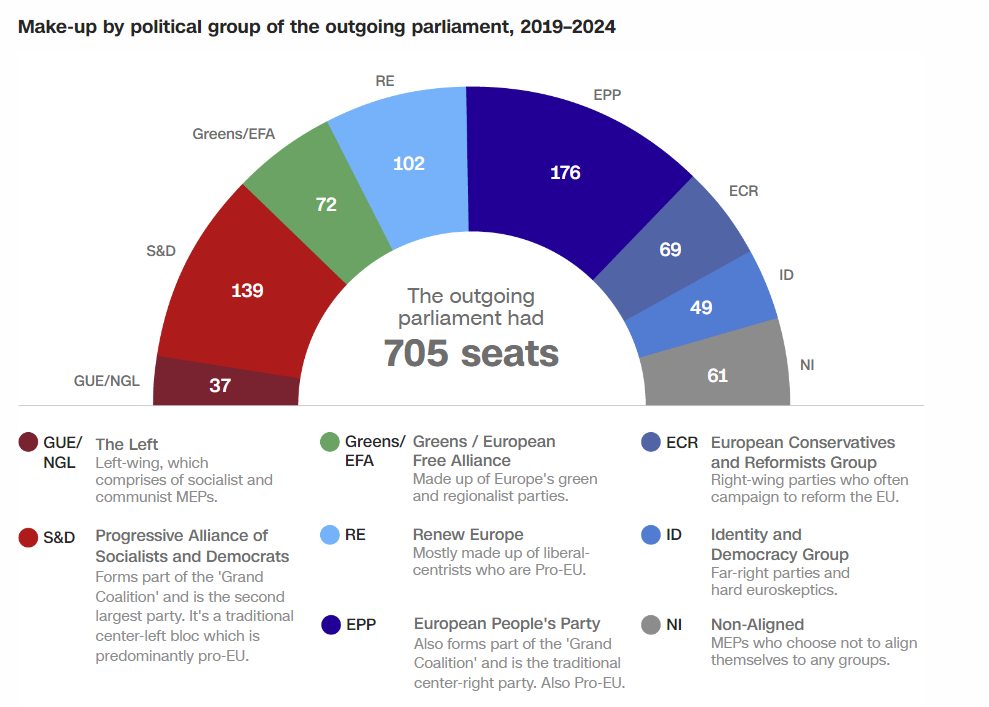

Before:

After:

Provisional results. Source: Le Monde.

Wednesday’s US CPI and FOMC are Key.

Friday The US reported that nonfarm payrolls rose by 272,000 jobs, far above the consensus forecast for a 185,000 increase, while blindsiding all 72 forecasters in a pre-payrolls Reuters survey. The results had something for those expecting unchanged rates and those hoping for a rate cut as early as September. Wednesday’s inflation numbers won’t settle the argument and the FOMC is likely to stay the course. Up until the Fed blackout period (when policymakers cannot talk publicly about policy), Committee members seemed united in their view that rates need to be restrictive for longer than expected, which suggests a tame FOMC statement and dot-plot guess.

Equity Markets Playing Defense

Holidays in China, Hong Kong, Taiwan, and Australia made for a slow start. Japan’s Nikkei 225 index climbed 0.92% supported by a soft yen. European bourses are deep in the red in the wake of the EU Parliamentary elections, and S&P 500 futures are down 0.22% due to ongoing fallout from Friday’s NFP data. The US 10-year Treasury yield is at 4.51% compared to Friday’s low of 4.245%.

EURUSD

EURUSD gapped lower, falling from 1.0817 at Friday’s close, opening at 1.0782 in Asia, then falling to 1.0734 in early NY trading. The European parliaments’ drift to the right, combined with the hot US NFP report on Friday and the risk of further US dollar strength from Wednesday’s US CPI and FOMC meeting, are weighing on the currency. The move below 1.0820 snapped the April uptrend line and suggests further losses to 1.0670.

GBPUSD

GBPUSD traded negatively in a 1.2688-1.2734 range. The currency was pressured by Friday’s US employment data but supported by EURGBP selling pressure following the EU elections. GBPUSD traders are focused on the upcoming UK elections on July 4. The intraday GBPUSD technicals are bearish and looking for a break below 1.2680 to extend losses to 1.2600.

USDJPY

USDJPY rallied sharply Friday and consolidated its gains in a 156.69-157.20 range overnight. Traders are cautious ahead of Friday’s Bank of Japan monetary policy meeting where policymakers are expected to slightly tighten monetary policy by announcing plans to reduce QE. GDP fell 1.8% y/y, a tad better than the -1.9% expected and last month’s 2.0% result, which is also slightly friendly for monetary policy tightening.

AUDUSD and NZDUSD

AUDUSD traded quietly in a 0.6576-0.6589 range overnight as it consolidated Friday’s losses in a quiet market as Australian and Chinese markets were closed for holidays. NZDUSD traded in a 0.6099-0.6115 band with traders content to await improved liquidity and Wednesday’s US data.

USDMXN

USDMXN rallied sharply in the wake of Friday’s NFP numbers, surging from 17.8076 to 18.4525 then extending those gains to 18.5019 before sliding to 17.4140 in early NY. The prospect of unchanged US rates for longer and the decisive Moreno party election victory are supporting prices. The Moreno Government won 83 of 128 seats in the Senate and 372 of 500 seats in the lower house.

BTCUSD (Bitcoin)

BTCUSD is licking its wounds after dropping from 71,879 to 68,866 on Friday, consolidating in a 69,101-69,798 range overnight. The uptrend line from May 10 is intact while prices are above 68,000.

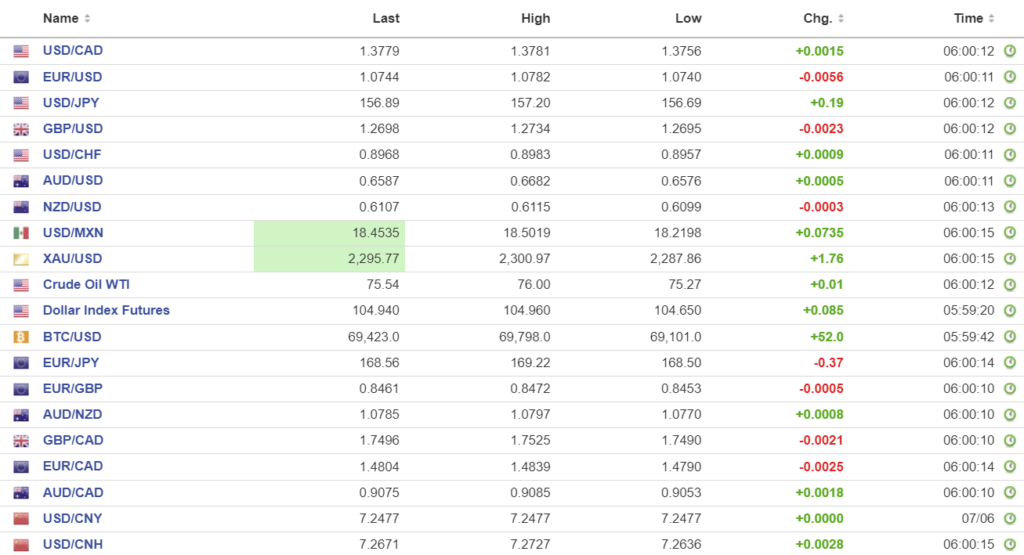

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

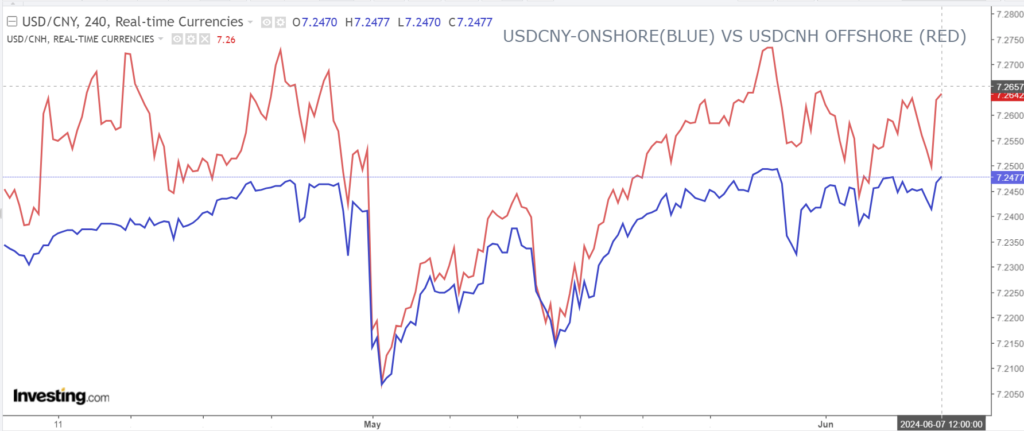

China Snapshot

PBoC fix: closed

Shanghai Shenzhen CSI 300 closed

Chart: USDCNY and USDCNH

Source: Investing.com