Source: Pixabay

- US PPI lower than expected, equity futures jump, greenback falls

- German ZEW Survey better than expected, improves risk sentiment

- US dollar opens on weak note-retreats from NY closing levels

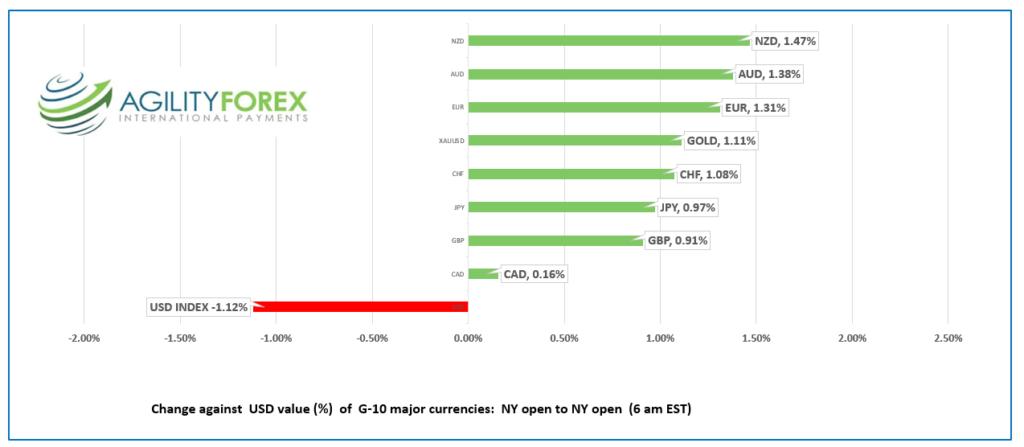

FX at a glance:

Source: IFXA Ltd/RP

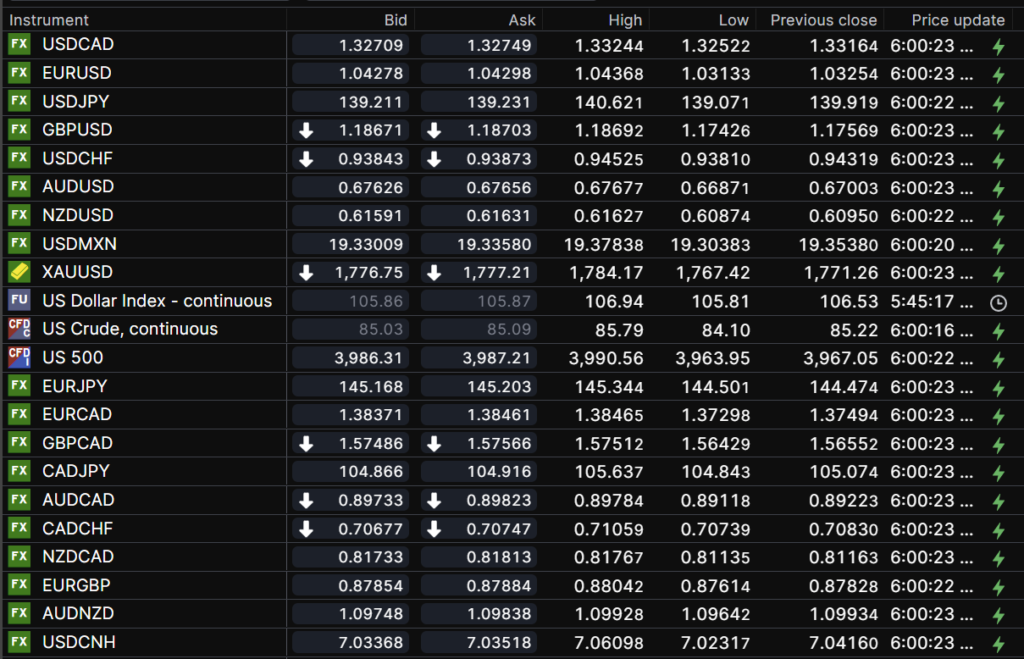

USDCAD Snapshot: open 1.3271-75, overnight range 1.3224-1.3324, close 1.3316

USDCAD direction continues to be driven exclusively by US dollar moves against the majors. Those moves were directionless in Asia, but the greenback went into a free-fall in Europe, which knocked USDCAD to its overnight low. Nevertheless, the price swings were just noise and inside the range since Friday.

Today’s US PPI data, ex food and energy rose 6.7%, easily beating the 7.2% forecast and September result. The results will encourage the narrative of as slowdown in Fed rate hikes.

WTI oil prices traded in a $84.10-$85.79/barrel range, sliding in Asia then rebounding in early NY trading to $85.48/b. Prices were pressured after Opec its forecast for global demand in Q4 alongside weaker than forecast Chinese data.

Today’s Canadian data includes September Manufacturing Sales and Wholesale Sales.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3330, looking for a break below 1.3250 to extend losses to the 1.3210- 1.3230 support zone. A break above 1.3330 targets 1.3390 while a move below 1.3210 sets the stage for a drop to 1.3000.

For today, USDCAD support is at 1.3210 and 1.3150. Resistance is at 1.3330 and 1.3370.

Today’s range 1.3190-1.3270

Chart: USDCAD 1 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US PPI data kicked off another “risk-on” rally. S&P 500 futures soared 1.6%, Treasury yields fell and the US dollar plunged. The reaction may be overdone as the Fed is not close to pausing rate hikes by merely entertaining 50 bp hikes, which used to be considered aggressive.

FX markets were subdued in Asia but perked up in Europe. Better than expected German and Euro area ZEW survey data combined with Fed Vice Chair Lael Brainard’s comments yesterday knocked the US dollar lower, although prices remained inside recent ranges.

The Biden-Xi Jinping meeting ended without fisticuffs which led to speculation that the US/China relationship would improve.

Yesterday, Fed Vice Chair Lael Brainard said that it was “probably appropriate to move to a slower pace of (rate) increases.” She said a slower pace allows the Fed to “assess more data and better able to adjust the path of rates to bring inflation down.”

So, she didn’t say anything new, and markets were already expecting a 50 bp hike on December 14. But it was a slow news day. Risk sentiment improved slightly and the 10-year Treasury yield slid from 3.869% overnight to 3.803% in NY today.

EURUSD drifted in a 1.0313-1.0327 range until Europe entered the fray, then soared to 1.0461 after the cooler than expected US PPI data. The rally got started followingbbetter than expected German and Euro area ZEW Survey results. German Economic Sentiment increased by 22.5 points to-36.7 and the Economic Situation improved by 7.7 points. The outlook is still negative, but things are looking up.

Eurozone Q3 GDP rose an “as expected” 0.2%, q/q. The EURUSD technicals suggest the break above 1.0330 paves the way for a test of resistance in the 1.0600 area, last seen in June.

GBPUSD mirrored EURUSD moves, rising from 1.1743 to 1.1988 with the US PPI data giving prices and added boost in NY. The UK ILO unemployment rate for the three months ending in September ticked higher, to a still robust, 3.6%, from 3.5% previously. UK pundits are making a big deal about Thursdays budget and the governments plans to address large deficits, but FX traders don’t seem to care. The UK technicals are bullish with the break above the 100-day moving average at 1.1654 setting up a rally towards 1.2000.

USDJPY traded in a 137.76-140.62 range , touching the bottom post-PPI. Today’s drop in the US 10-year Treasury yield to 3.773%, previous BoJ intervention, and hopes the Fed slows the pace of rate hikes are weighing on the currency pair/

AUDUSD traded sideways in Asia then rallied from 0.6687 to 0.6796 in NY. The gains were fueled by broad US dollar weakness in Europe. The minutes of the November 1 RBA policy meeting didn’t offer anything new. The bank is willing to pause or hike rates, depending upon circumstances.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

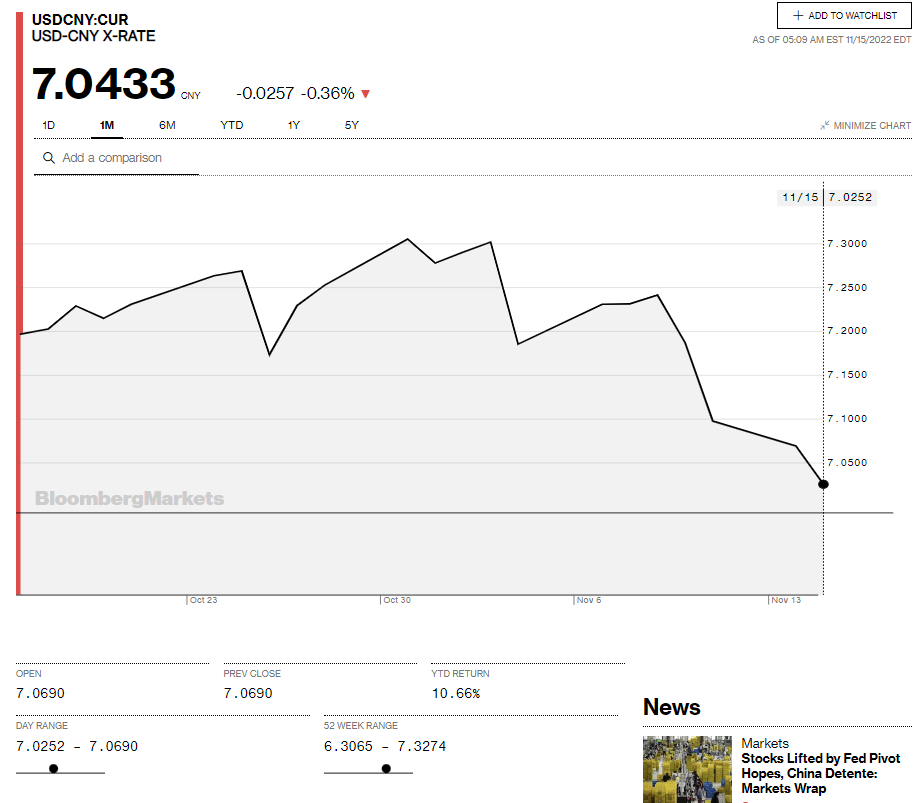

China Snapshot

Today’s Bank of China Fix: 7.0421, previous 7.0899

Shanghai Shenzhen CSI 300 rose 1.90% to 3865.97

PboC leaves rates unchanged.

Stocks supported by Biden-Xi Jinping meeting and yesterday’s announcement of support for property developers and home buyers.

October Industrial Production 5.0% y/y (forecast 5.2%, September 6.3%)

October Retail Sales -0.5% y/y (forecast 1.0%, September 2.5%)

Chart: USDCNY 1 month

Source: Bloomberg