Photo: Wikimedia

- FOMC minutes have something for Hawks and Doves

- European Union inflation 9.8% y/y (9.6% y/y in June)

- US dollar opens firm compared to Wednesday

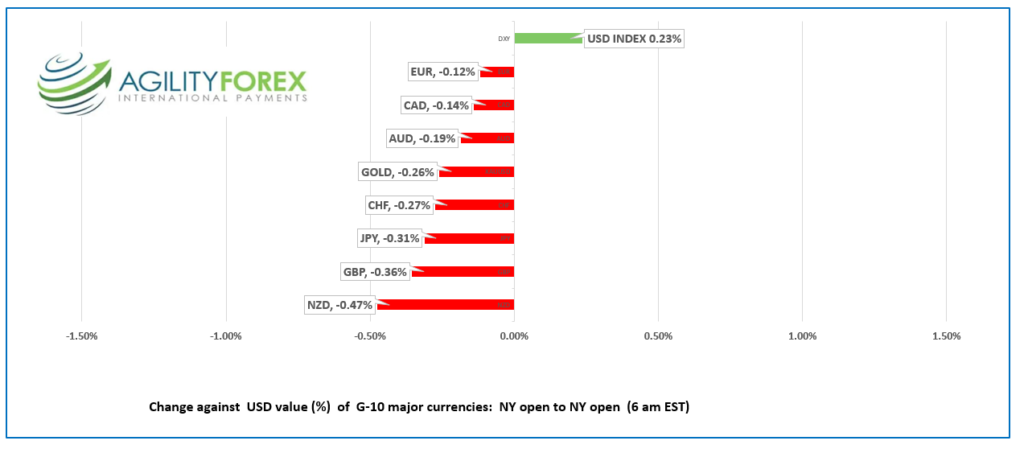

FX at a glance:

Source: IFXA Ltd/RP

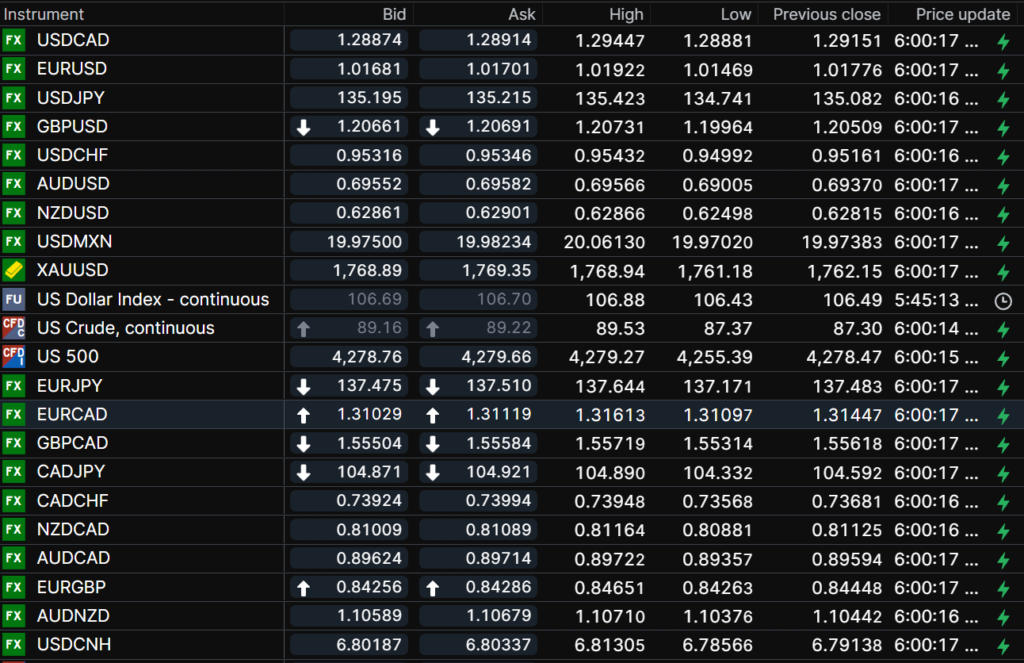

USDCAD Snapshot: open 1.2887-91, overnight range 1.2904-1.2945, close 1.2915

USDCAD is rangebound with price swings at the mercy of the prevailing US dollar sentiment, which is measured by S&P 500 moves. Equity traders are not convinced in any direction leaving USDCAD trapped in a 1.2850-1.2950 band.

Oil prices are not helping the currency either. WTI rallied from $86.20/barrel yesterday to $89.53/b overnight but remain well below last Friday’s peak of $94.70/b. Prices got a bit of a boost after the EIA reported US crude stocks dropped 7 million barrels in the week ending august 12. However gains were capped by concerns of slowing demand from China.

Canada Industrial Production fell 2.1% in July (forecast 1.0%) and Raw Materials Price index dropped 7.4%(forecast) but the results were ignored.

USDCAD Technical outlook

The intraday USDCAD technicals are directionless in a choppy 1.2850-1.2950 range. A topside break targets 1.3050 while a move below 1.2850 targets 1.2750. Fibonacci retracement analysis of the July/August range suggests a decisive break above 1.2912 puts 1.3030 in play, while a move below 1.2840 targets 1.2720.

For today, USDCAD support is at 1.2860, and 1.2830. Resistance is at 1.2940 and 1.2980. Today’s range: 1.2850-1.2930

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The FOMC minutes did not provide any clear direction. “Rates need to go higher until they don’t” sums up the message. Some participants worried the Fed could tighten more then necessary, while others suggested rates may need to reach a restrictive level and stay there. As usual, there were many pages of observations, comments etc, but the minutes are stale, and do not reflect the latest inflation or nonfarm payrolls data.

Wall Street rallied after the minutes, but the move didn’t last. The DJIA closed down 0.50%, the S&P 500 lost 0.72% and the Nasdaq fell 1.25%. The US dollar retreated briefly but recouped the losses by the NY close.

The FX overnight session was choppy with the greenback opening unchanged to weaker against the major G-10 currencies in NY. Asian equity indexes followed Wall Street lower, led by a 0.86% in Japan’s Nikkei 225 index.

European equity traders see things differently and a 0.70% increase in the German Dax is leading the way. S&P 500 and DJIA futures are modestly higher as are gold and oil prices. The US 10-year Treasury yield ranged in a 2.86 8%-2.913% band.

The major central banks are comfortably into rate hiking mode and 50 bps is the preferred size. The RBNZ hiked by that amount yesterday, Norway’s Norges Bank raised rates 50 bps today (to 1.75%) and analysts are debating whether the Fed ‘s next hike is 50 or 75 bps.

ECB policymaker Isabel Schnabel is setting the stage for an ECB hike of 50 bps. She said, “In July we decided to raise rates by 50 basis points because we were concerned about the inflation outlook,” “In July we decided to raise rates by 50 basis points because we were concerned about the inflation outlook. The concerns we had in July have not been alleviated… I do not think this outlook has changed fundamentally.”

US weekly jobless claims fell 2,000 to 250,000 after the previous weeks results were revised lower. The Philadelphia Fed Manufacturing Survey current activity index rose to 6.2 from -12.3 in July. FX markets did not react to the data.

EURUSD traded in a 1.0147-1.0192 range with prices underpinned by Eurozone inflation data. Eurostat reported “The euro area annual inflation rate was 8.9% in July 2022, up from 8.6% in June. A year earlier, the rate was 2.2%. European Union annual inflation was 9.8% in July 2022, up from 9.6% in June. A year earlier, the rate was 2.5%.” There are $3.2 billion of option expiries rolling off today at 10: am EDT.

GBPUSD opened at its overnight session low of 1.1996 in Europe, then climbed steadily reaching 1.2092, coinciding with the US dollar retreat during the European session. Yesterday’s UK inflation data fueled speculation the Bank of England would hike rates by 200 bps before May 2023, starting with a 50 bp increase in September. The news is overshadowed by looming recession concerns which are exacerbated by a rash of labour unrest across the country.

USDJPY dropped from 135.46 just before the FOMC minutes to 134.73 in early Asia trading. Those losses were recovered overnight due to higher US Treasury yields.

AUDUSD traded choppily in a 0.6901-0.6969 range due to shifting US dollar sentiment. AUDUSD lost ground after the Australia Bureau of Statistics reported the country lost 40,900 jobs which overshadowed news the unemployment rate dipped to 3.4% from 3.5%, the lowest level since 1974.

NZDUSD mirrored AUDUSD moves and is trading near the top of its 0.6250-0.6295 range.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

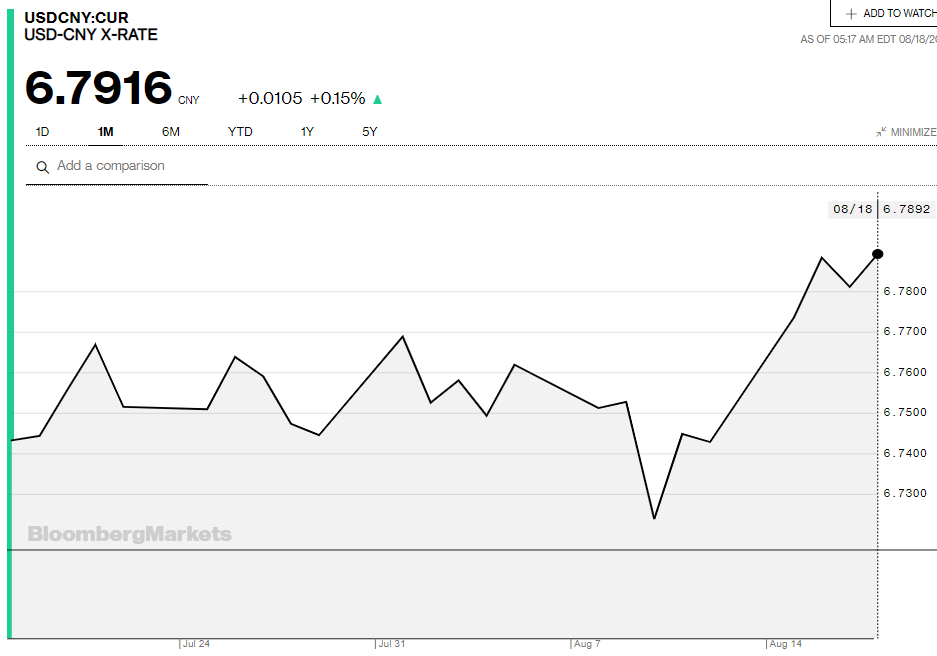

China Snapshot

Today’s Bank of China Fix: 6.7802, previous 6.7863

Shanghai Shenzhen CSI 300 fell 0.87% to 4,180.10

Goldman Sachs downgrades China 2022 GDP to 3.0% from 3.3%, while Nomura cuts 2022 GDP to 2.8% from 3.3% due to weak demand from government covid policies , ongoing property woes, and higher energy prices.

Chart: USDCNY 1 month

Source: Bloomberg