Photo: hdclipartall.com

February 2, 2023

- Dovish Fed hike roils markets-Powell seemed befuddled.

- BoE and ECB hike rates by 50 bps

- US dollar reeling after FOMC.

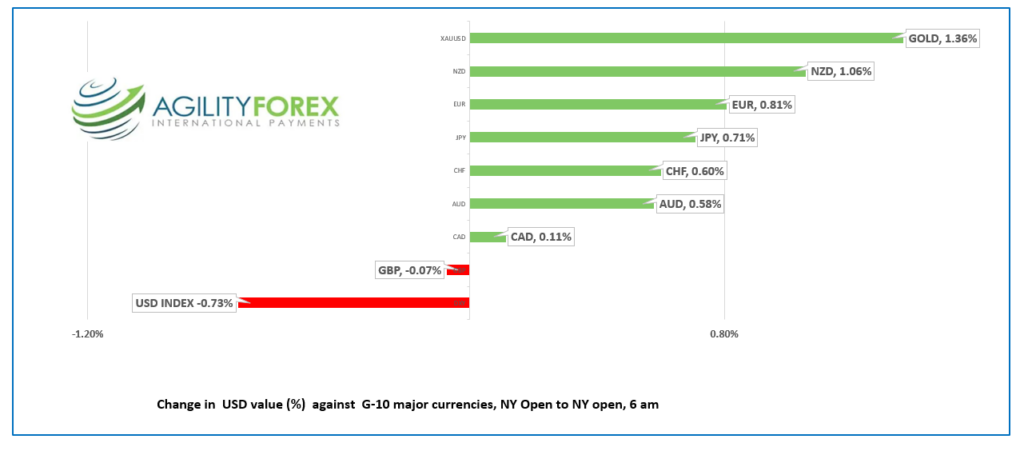

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3294-98, overnight range 1.3264-1.3296, close 1.3291

USDCAD plunged on widespread US dollar selling vs the G-10 majors after traders dismissed the Fed’s inflation and interest rate outlook following Jerome Powell’s press conference.

WTI oil prices fell from $79.69/b to $76.07/b yesterday after disappointing EIA and ISM Manufacturing PMI data. EIA report US crude inventories rose by 4.1 million barrels in the week ending January 27 while ISM PMI was worse than expected at 47.4 (forecast 48). The results suggest lower US demand from a slowing economy.

The drop in WTI prices helped to slow USDCAD losses above major resistance in the 1.3250 area. Failure to break below this levels risks a return to 1.3600.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3340 but need to break major support at 1.3250 or continue to bounce in a 1.3250-1.3450 range.

The daily chart warns that a substantial move is imminent. A move below 1.3250 opens the door to further losses to the 1.2980-1.3000 area while a break above 1.3460 suggests further gains to 1.3600.

For today, USDCAD support is at 1.3250 and 1.3210. Resistance is at 1.3350 and 1.3390

Today’s range 1.3250-1.3320

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The Fed hiked the overnight rate by 25 bps to 4.75% as widely expected. The monetary policy statement was fairly straightforward noting that “ongoing rate increases will be appropriate.”

So far, so good, but then Fed Chair Powell’s press conference began.

He looked as timid and uncertain as Bambi at the start of hunting season. He failed to convince markets that the Fed outlook for inflation and interest rates was the correct view. He didn’t help his case by acknowledging that the “disinflationary process has begun. He struggled to explain how slowing wage growth, and the speed of falling inflation would necessitate higher interest rates.

At the end of the day the market and Mr Powell agreed to disagree, with the market voting with their wallets.

The market’s favourite risk sentiment barometer, the S&P 500 index, closed with a 1.05% gain while the US 10-year Treasury yield fell from 3.52% to sit at 3.41% this morning. The US dollar was sold across the board.

The post-FOMC reaction in Asia was rather tepid. The Nikkei and Australia’s ASX 200 managed to close with tiny gains while Chinese markets closed with small losses.

European bourses are higher led by a 1.19% gain in the German Dax and a 0.65% rise in the UK FTSE 100. Those levels are little changed following the BoE and ECB rate hikes

S&P futures climbed 0.45% so far, gold gained 0.11% since yesterday’s close and WTI oil is down 0.83% as of 5:30 am PT.

EURUSD surged from a low of 1.0853 yesterday to 1.1032 in early Asian markets then spent the rest of the session in a 1.0982-1.1024 range. The single currency traded at 1.0977 after the ECB raised rates by 50 bps to 2.5% and indicated that at least one more hike was in the cards.

The statement said, “In view of the underlying inflation pressures, the Governing Council intends to raise interest rates by another 50 basis points at its next monetary policy meeting in March. The technicals are bullish above 1.0930, looking for a break above 1.1050 to extend gains to 1.1170.

GBPUSD rallied from 1.2275 post-FOMC to 1.2401 in Asia then dropped to 1.2310 in Europe ahead of the Bank of England meeting. The BoE delivered on expectations and hiked rates 50 bps to 4.0% in a 7-2 vote. The MPR lowered 2023 inflation forecast to 4.0% from 5.25% while cutting the GDP forecast to -0.5% from 1.5%. GBPUSD spiked to 1.2385 on the news but has since retreated to 1.2325.

USDJPY is grinding out gains after yesterday’s post-FOMC plunge took prices from 129.85 to 128.18 in Asia, before climbing to 129.12 where the rally ran out of steam. The drop in US Treasury yields due to the market’s conviction the Fed’s rate outlook is wrong and the risk of a hawkish BoJ in coming months is weighing on the currency pair.

AUDUSD traded in a 0.7043-0.7157 range since the FOMC, due to broad US dollar weakness, positive Australian building permits data, and higher commodity prices.

US weekly jobless claims were better than expected, falling 3,000 to 183,000 which was better than the forecast for an increase of 14,000.

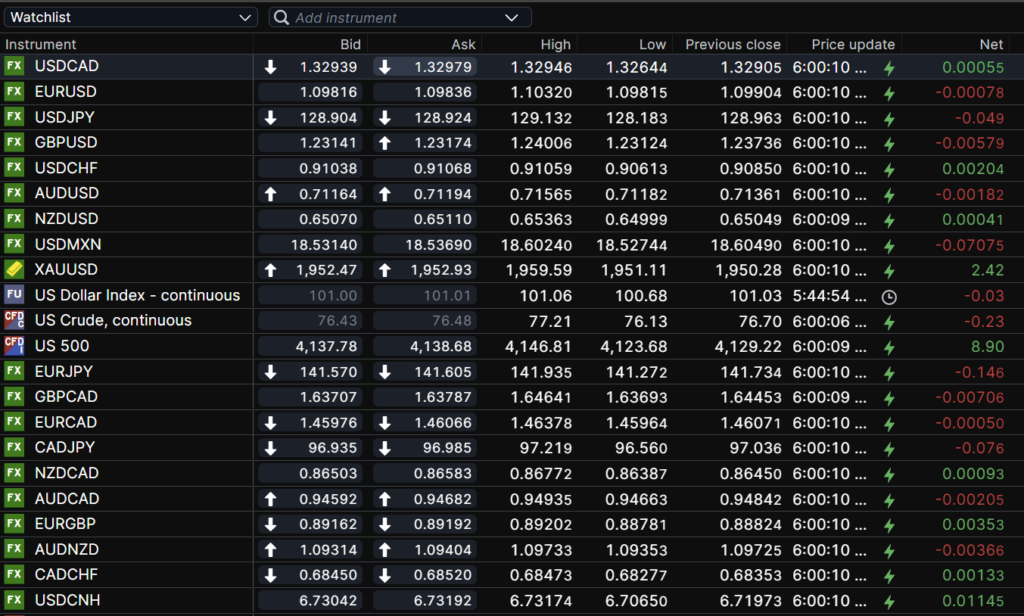

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

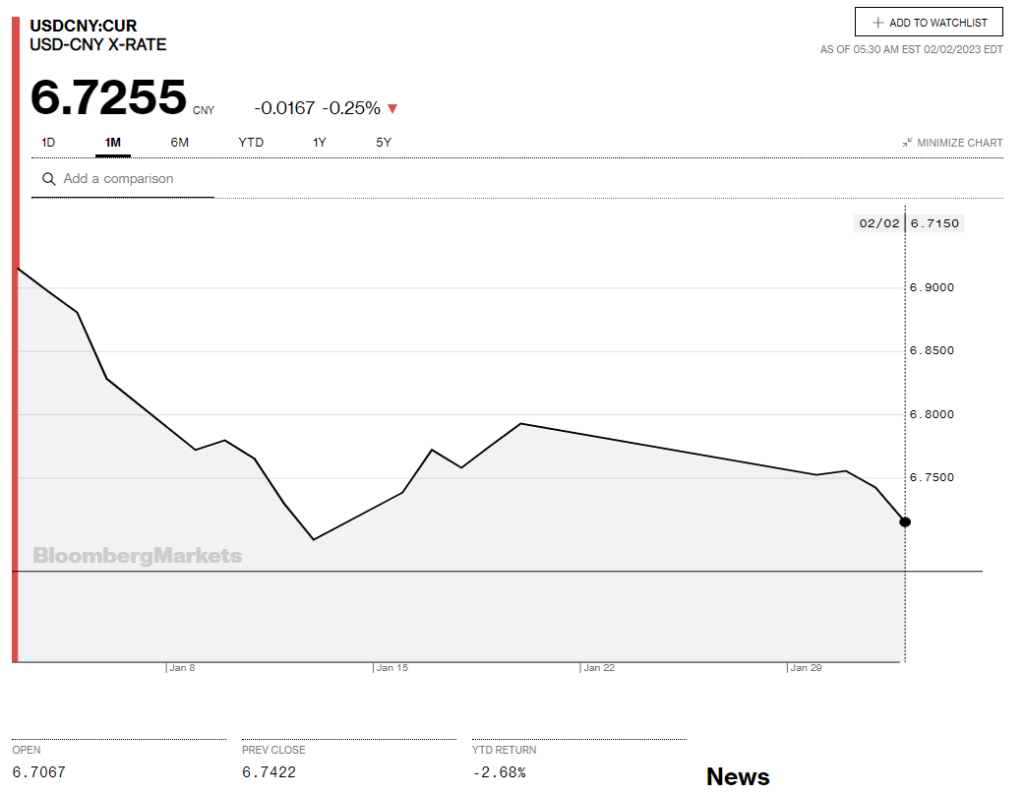

China Snapshot

Bank of China Fix: 6.7130, Previous: 6.7492,

Shanghai Shenzhen CSI 300 fell 0.35% % to 4181.15.

Chart: USDCNY 1 month

Source: Bloomberg