Source: HDClipartall.com

- Embarrassed UK government retracts top-tier tax cuts

- Quiet start as Chinese, Australian, South Korean, and German markets closed

- US remains above Friday opening levels, but mixed from the close-GBPUSD outperforms

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3771-75, overnight range 1.3713-1.3826, close 1.3831

USDCAD is a victim of US dollar strength and that won’t change until the greenback finds a peak. The Canadian economy showed signs of slowing, even though the 0.1% gain in July matched the increase in June.

USDCAD opened near its overnight session low then fell further in NY, coinciding with S&P 500 futures rising 0.62%.

Traders may get some fresh insight into the Bank of Canada’s outlook for the economy on October 6, when Governor Tiff Macklem addresses the Halifax Chamber of Commerce. Even so, the BoC monetary meeting isn’t until October 26, which suggests domestic events will be on the back burner, and the currency will remain vulnerable to global risk sentiment.

Oil traders are looking ahead to Wednesday’s Opec meeting. The cartel is expected to announce they are cutting production by at least 1 million barrels/day in an effort to shore up slumping prices. WTI rallied on the news, climbing from $79.72/barrel at Friday’s close to $83.28/b in Europe. The rally is somewhat dubious as the cartel is merely cutting production from a level they are unable to achieve, to a level they still can’t meet.

The Canadian data calendar is empty.

USDCAD Technical outlook

The intraday technicals are bullish above 1.3710, looking from a break above 1.3780 to retest Friday’s peak of 1.3835. A break of the latter level will extend gains to 1.3650. A move below 1.3710 targets 1.3560, then 1.3460.

Longer term, Fibonacci retracement analysis of the 2020-2021 range suggests the break above 1.3650 sets the stage for gains to 1.4040, the 76.6% retracement.

For today, USDCAD support is at 1.3710 and 1.3660. Resistance is at 1.3760 and 1.3810. Today’s range: 1.3670-1.3770

Chart: USDCAD daily

Source: Saxo Bank

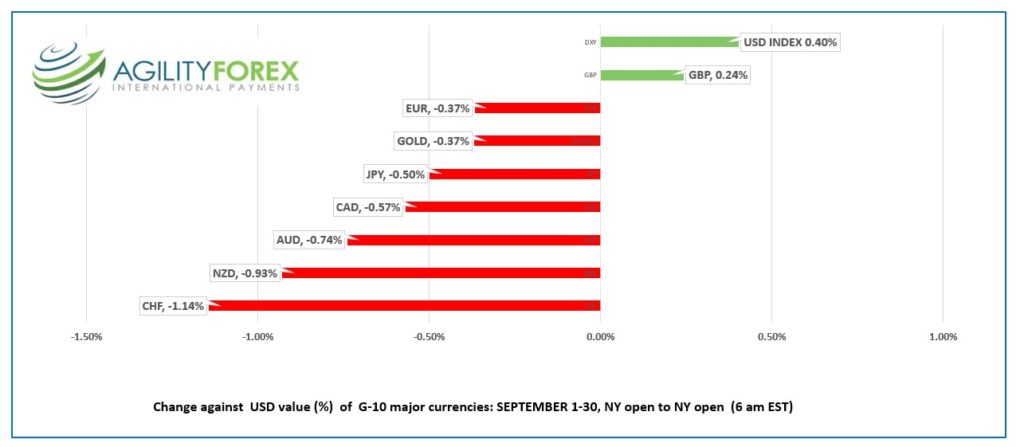

G-10 FX recap and outlook

October is a spooky month, and no one was more spooked than UK Prime Minister Liz Truss and Chancellor Kwasi Kwarteng. The volatile market reaction to their mini budget forced the two incompetents to reverse planned tax cuts for those earning over £150,000.

The UK leadership may be incompetent, but they look like superstars when compared to Turkey’s government. Recep Erdogan’s erdoganomics has lifted inflation from 14.6% in 2020 to 83.45% y/y in September 2022.

EURUSD chopped about in a 0.9754-0.9834 range. Prices tumbled from the peak after Eurozone September Manufacturing PMI fell deeper into contraction territory, dropping to 48.4 from 48.5 in August. The decline is the result of sliding output and new orders. Market chatter about the health of Credit Suisse, the 2nd largest bank in Switzerland, is not helping matters, although fears of its demise seem a tad overdone.

GBPUSD rallied from 1.1088 to 1.1281 on anticipation the UK government would reverse tax cut plans for high earners. Prices retreated to 1.1165 when the rumours were confirmed but have rebounded to 1.1215 in NY. Chancellor Kwarteng denied the move was in response to the gilt market turmoil, which implies the policy reversal was a desperate move to save his job. GBPUSD gains are limited due to ongoing economic woes which are exacerbated by failing confidence in the administration.

USDJPY traders are taunting the BoJ. They drove prices from 144.51 to 145.31, despite the 10-year Treasury yield dropping from 3.833% to 3.762%, daring policymakers to intervene. The rally was reversed in NY.

AUDUSD drifted higher overnight, rising from 0.6404 to 0.6459 ahead of the expected 0.50% RBA rate hike tomorrow. There is a risk the RBA will only raise rates by 25 basis points due to previous comments about normalizing policy moves.

NZDUSD firmed in a 0.5599-0.5663 band due to a broadly softer US dollar and expectations that the RBNZ hikes rates 50 bps on Wednesday.

US ISM Manufacturing PMI is expected at 52.2 compared to 52.8 in August.

Chart of the Day: USDJPY hourly

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: Closed: previous 7.0998

Shanghai Shenzhen CSI 300 closed

Caixin September Manufacturing PMI 49.1 (forecast 49.5, August 49.5)

NOTE: Chinese markets closed next week for Golden Week.

Chart: USDCNH (offshore) 1 month

Source: Saxo Bank