January 11, 2024

- US Core CPI gives a bit of something for everyone.

- WTI remains rangebound with gains capped by concerns of weak demand.

- US dollar opens mixed, and little changed form yesterday.

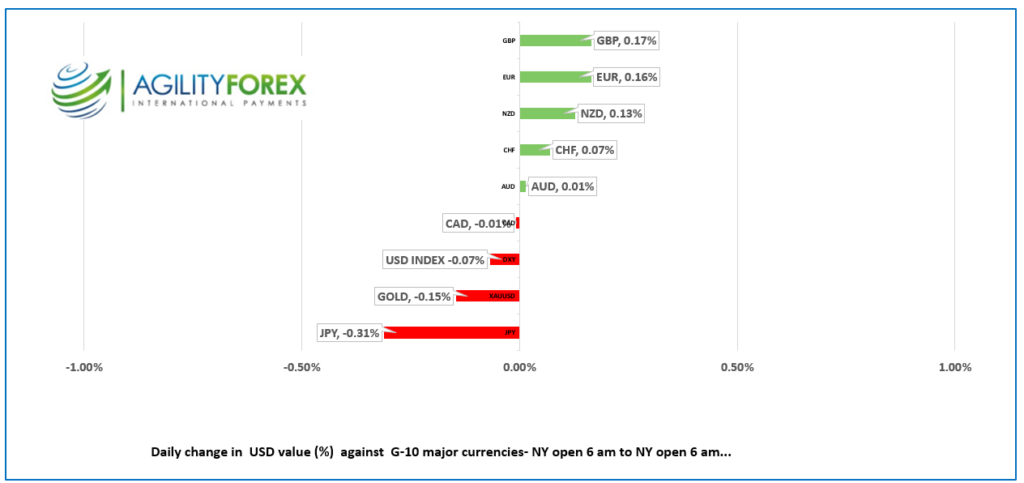

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3372-76, overnight range 1.3355-1.3411, close 1.3382.

USDCAD surged to 1.3411 from 1.3360 in the wake of the disappointing US inflation report. US headline CPI rose mores than expected while Core CPI rose 0.1% more than expected. The news squeezed short USDCAD positions and raised questions about the magnitude of Fed rate cuts in 2024.

The Bank of Canada is expected to match Fed rate cuts with some analysts believing the BoC’s first 25 bp cut will occur at the March 6 meeting.

Oil prices are struggling to maintain upward momentum and yesterday’s EIA report of a 1.1 million barrel increase in inventories didn’t help. WTI continues to chop about in a $70.00-$74.00/b range which has contained prices since the end of December. Barclay’s Bank cut its Brent forecast for this year by $8.00/b to $85.00/b due to higher supply. However, analysts did not that at current levels, oil looks undervalued.

USDCAD Technicals:

The intraday USDCAD technicals are bullish while prices are above 1.3340. A break above resistance in the 1.3440 area suggests further gains to 1.3490. However, only a decisive breech of 1.3550 resistance will negate the downtrend that has guided prices lower since the beginning of November.

The longer term technicals are bullish. The uptrend from June 2021 is at 1.3200 (daily chart) while the 200 day moving average is at 1.3360. The uptrend from August 2011 is intact while prices are above 1.2500 (monthly chart) and the June 2021 uptrend is in play above 1.3200 (monthly chart)

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3440 and 1.3480. Todays range 1.3340-1.3430.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The highly anticipated US inflation number was more “meh” than lukewarm coffee on a Monday morning. US headline inflation rose 0.3% to 3.4%, which is above the consensus forecast of 3.2% and November’s 3.1% increase. The 0.1% decline in Core inflation to 3.9% from 4.0% was not enough to offset the disappointment from the headline. Adding insult to injury was that weekly jobless claims were 202,000, unchanged from last week and below the 210,000 estimate.

Perhaps New York Fed President John Williams had a point yesterday. He said it was still far too soon to expect interest rate cuts. He said, “I expect that we will need to maintain a restrictive stance of policy for some time to fully achieve our goals, and it will only be appropriate to dial back the degree of policy restraint when we are confident that inflation is moving toward 2% on a sustained basis.”

Traders were not impressed. The US dollar jumped, S&P 500 futures fell, and the US 10-year Treasury yield rose to 4.04% from 3.99%. More than likely, the immediate reaction is just a knee-jerk reaction by short-term traders. No one expects a rate cut on January 31, and that leaves two more CPI reports before the March 20 decision.

EURUSD dropped from 1.0990 to 1.0950 following the US data, after trading with a bit of a bid in a 1.0958-1.1000 range overnight and into CPI. The single currency received some support in Europe after ECB policymaker Isabel Schnabel said it was too early to discuss rate cuts.

GBPUSD dropped to 1.2732 from a pre-CPI of 1.2761 but is still inside its 1.2730-1.2774 overnight range. The pound is modestly underpinned by speculation that UK recession odds have diminished.

USDJPY spiked to 146.16 from 145.36 following the inflation data. The risk that US and Japanese rates remain unchanged for longer than anticipated is driving USDJPY higher.

AUDUSD fell through the bottom of its overnight 0.6695-0.6726 range after the inflation data and is currently trading at 0.6663. Earlier support after a larger than expected trade surplus in December (actual 11.437 billion vs. 7.66 B in November) has been forgotten.

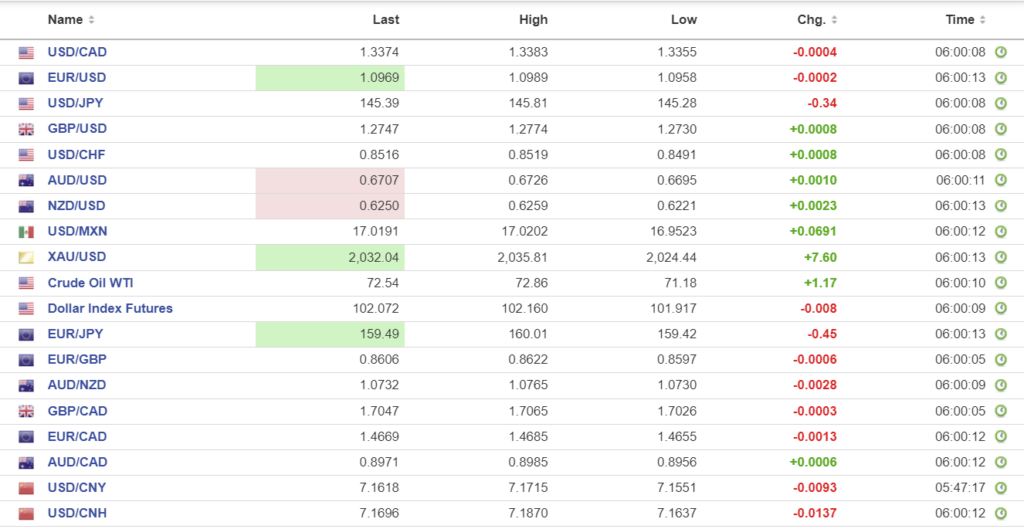

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1087, expected 7.1667, previous 7.1055.

Shanghai Shenzhen CSI 300 rose 0.57% to 3295.67.

Chart: USDCNY and USDCNH 1 year.

Source: Investing.com