May 13, 2024

- Trader’s biding their time ahead of inflation data Tuesday and Wednesday.

- Oil prices inch higher while equities flat-line.

- US dollar opens mixed but little changed from Friday.

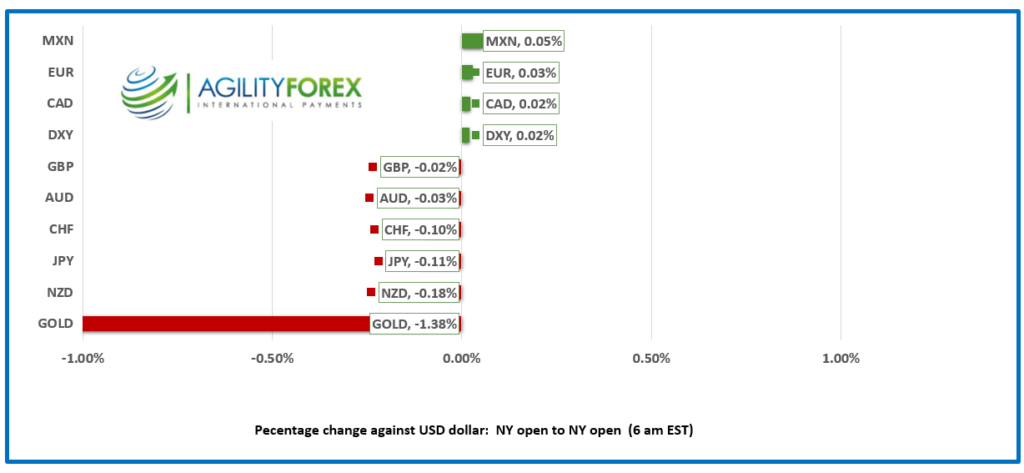

FX at a Glance

Source: IFXA/RP

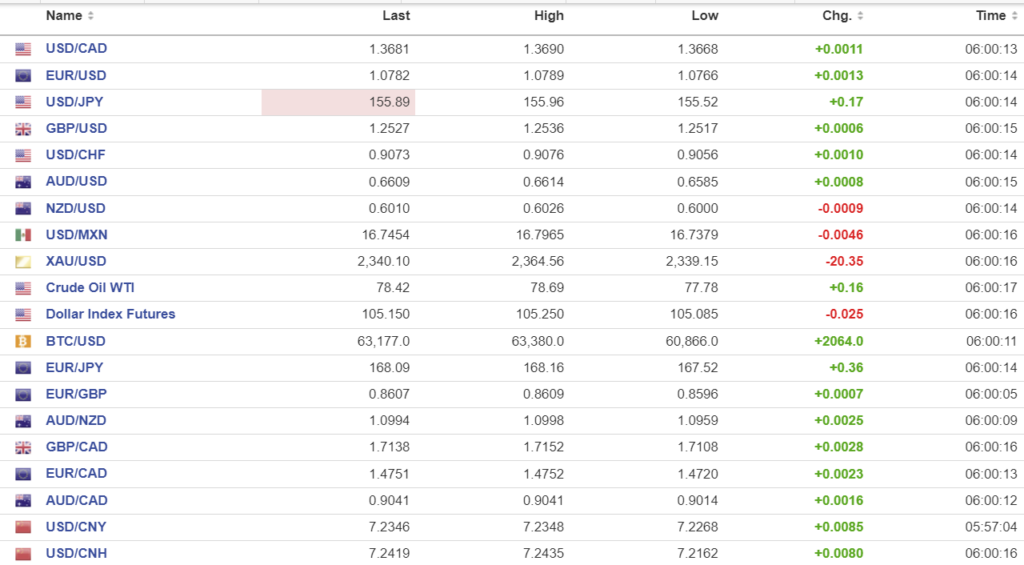

USDCAD Snapshot: open 1.3681, overnight range 1.3668-1.3690, close 1.3673

USDCAD dropped to 1.3634 from 1.3680 ish on Friday, after Statistics Canada reported 90,400 new jobs were created in April. The move was fully reversed when the details revealed that it was really quite weak because the number of new jobs was below the number of immigrants entering the work force. Compared to last April, Canada’s working population aged 15 and over grew by 3.3% from 32.2 million to 33.3 million last month. Employment though only grew by 1.9% over that same time frame from 21.1 million to 21.8 million.

Traders have shifted their focus to the US inflation data due this week. Evidence of lower prices will encourage speculation that the Fed will cut rates more aggressively which in turn will limit USDCAD gains due to expectations of widening CAD/US interest rate differentials if the BoC cuts rates in June.

WTI traded is at the top of is 77.78-78.72 overnight range with prices weighed down by concerns US rates will remain at current levels for longer than previously expected.

USDCAD Technicals

The intraday USDCAD technicals flipped to bullish from bearish on Friday when prices rallied above 1.3680 after failing to break below support at 1.3630. A break above 1.3710 would extend gains to 1.3760.

Longer term, the January uptrend line is intact above 1.3590 which is guarded by support in the 1.3610-1.3630 level. A break above 1.3740 targets 1.3900.

For today USDCAD support is at 1.3640 and 1.3610. Resistance is at 1.3710 and 1.3740. Today’s range is 1.3650-1.3730.

Chart: USDCAD daily

Source: DailyFX

Inflation, Inflation, Toil, and Trouble

It’s open-the-kimono time in the US this week with inflation data flashing today, tomorrow, and Wednesday. The New York Fed’s Survey of Inflation Expectations is today, the Producer Price Index on Tuesday, and the Consumer Price Index on Wednesday. Global markets have their fingers crossed and are hoping to see lower readings, which would encourage the Fed to step up the pace of easing. At the moment, traders expect the first rate cut in November.

Equities are marking time.

Asian equity indexes closed little changed in an uneventful session. Things were not any different in Europe. The major bourses are underwater, led by a 0.24% dip in the German DAX. The UK FTSE 100 is the exception, and it is slightly positive. S&P 500 futures are up 0.14%, and the US 10-year Treasury yield is little changed at 4.449%. Gold (XAUUSD) is down $17.47 since Friday’s close.

EURUSD

EURUSD was steady in a 1.0766-1.0789 range with traders patiently awaiting this week’s US inflation data. The EURUSD downtrend channel since November 2023 is intact between 1.0850 and 1.0500. However, the intraday technicals are bullish above 1.0740.

GBPUSD

GBPUSD shuffled around in a 1.2517-1.2536 range with gains from the better-than-expected Q1 data on Friday fading due to the dovish outlook for UK rates. Traders are looking ahead to Tuesday’s employment report and comments from BoE Chief Economist Huw Pill.

USDJPY

USDJPY drifted higher in a narrow 155.52-155.96 range. The BoJ has taken a toll on JPY short positions according to IMM positioning data. Prices were also weighed down by the steady US 10-year Treasury yield of 4.485%.

AUDUSD AND NZDUSD

AUDUSD is trading at the top of its 0.6585-0.6614 range. NAB Business Conditions Index eased to 7 from 9 in March, while Business Confidence was unchanged at 1. NAB Chief Economist Alan Oster wrote, “All three components of business conditions were back at their long-run averages in April. In some ways, this marks a bit of a milestone after a long period in which conditions have been gradually easing from the very high levels seen in 2022, reflecting slowing economic growth.”

NZDUSD traded defensively in a 0.6600-0.6626 range. The Business NZ services index contracted further, dropping to 47.1 in April from 47.2 in March.

USDMXN

USDMXN consolidated Friday’s losses in a 16.7379-16.7965 range. Prices are undermined by expectations that Banxico will leave rates at elevated levels for longer than expected due to their outlook that inflation will remain sticky.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1030 vs exp. 7.2284 (prev. 7.1011).

Shanghai Shenzhen CSI 300 fell 0.04% to 3664.69.

April CPI 0.1% m/m and 0.3% y/y (previous 0.1%), PPI -2.5%y/y (forecast -2.2, previous -2.8

Country Garden Holdings made a coupon payment despite an earlier warning that would be unable to due to a lack of funds. Analyst are speculating that the guarantor, China Bond Insurance may have leaned on Country Gardens officials to make it happen.

China will start selling $138 billion ( 1 trillion yuan) of long bonds on Friday, in 20, 30 and 50 year tranches.

Chart: USDCNY and USDCNH

Source: Investing.com