Image by DALL-E,

December 12, 2023

- US November Core-CPI unchanged at 4.0%

- ZEW Survey shows economic sentiment improved in Germany.

- US dollar opens with small losses , dips further post CPI.

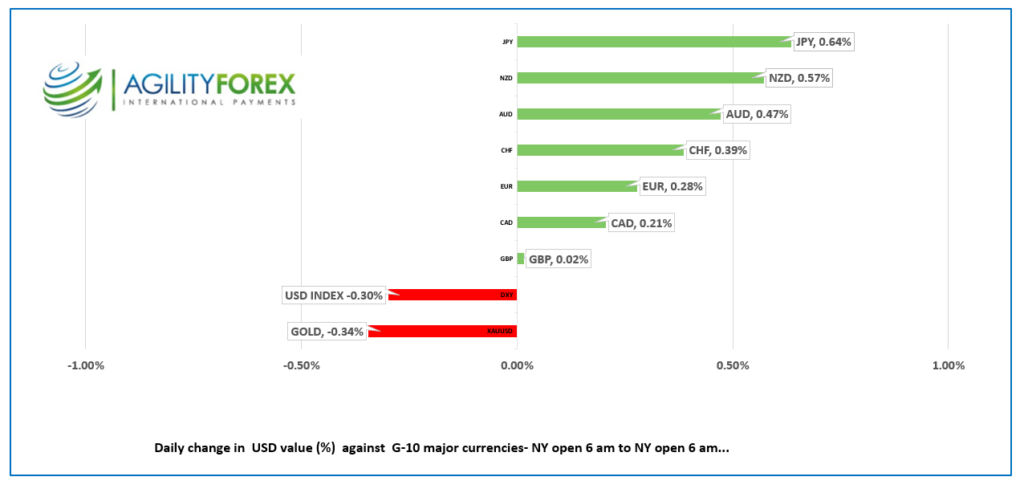

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3566-70, overnight range 1.3549-1.3580, close 1.3574

USDCAD inched lower overnight due to broad-based bearish US dollar sentiment then ticked below the overnight low to 1.3545, after the US inflation data. That sentiment will continue to drive USDCAD direction today.

The US Core inflation reading was unchanged at 4.0%, exactly as predicted and the results will not do anything to change anyone’s outlook for US interest rates in 2024. may drive prices lower as it would lift the odds of the Fed cutting rates in March.

USDCAD downside may be limited because of soft oil prices.

WTI is trading lower in a $70.47-$71.95/barrel range with the low occurring in the wake of the US CPI results. Prices continue to be depressed because of robust crude supplies which more than offset the latest Opec production cuts. The cartel said it would trim production by a total of 2.3 million bpd, starting in January.

USDCAD Technicals:

The intraday USDCAD technicals are bearish below the 1.3590-1.3510 area and looking for a break below 1.3540 to extend losses to 1.3480. A break above 1.3620 targets 1.3660, then 1.3720.

The uptrend from July 2023 comes into play at 1.3500 on a daily chart.

For today, USDCAD support at 1.3540 and 1.3510. Resistance is at 1.3610 and 1.3660. Today’s range 1.3510-1.3610.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Inflation may have been clubbed to the canvas, but it is far from being knocked out. Headline US CPI rose 3.1% year-over-year in November, as forecast, but 0.1% below the 3.2% year-over-year result in October. The more important Core-CPI remained unchanged at 4.0%.

The market reaction was mixed. The US 10-year Treasury yield, which had dropped from 4.24% at yesterday’s close to 4.176% just before today’s data, popped to 4.216% immediately afterwards. That is just noise and not evidence of a shift in sentiment. S&P 500 futures dipped from 0.17% to -0.21%, a negligible move.

Meanwhile, the US dollar experienced a very short-lived dip, then quickly erased the move as traders settled in to wait for the Wednesday afternoon FOMC meeting statement.

Today’s CPI data sets the stage for tomorrow’s FOMC meeting. No one expects the Fed to raise or lower rates, but today’s CPI print sets the tone for the monetary policy statement and press conference. Fed Chair Powell can be optimistic about the direction of inflation but will likely warn that the Fed has more work to do. Traders have already downgraded the odds for a rate cut in March and are still pricing in four rate cuts by the end of 2024.

EURUSD traded sideways in Asia, then climbed from 1.0759 to 1.0829 in NY, post-CPI, before dropping to 1.0781. In Europe, prices got a lift from the better-than-expected German Eurozone Zew survey. The survey said, “the situation and economic expectations have improved because the number of respondents expecting ECB rate cuts has doubled.” EURUSD was also supported by broad US dollar selling pressure ahead of today’s inflation report.

GBPUSD chopped in a 1.2543-1.2516 range. Prices peaked after the CPI then rapidly retreated to 1.2551 in NY. GBPUSD suffered from a soft UK employment report. Wages fell with total average earnings falling from 8.0% to 7.2% in the three months to October, which increased risks that the Bank of England will cut rates in June 2024.

USDJPY traded erratically in a 144.74-146.19 range due to the ebb and flow of US 10-year Treasury yields and uncertainty around the December BoJ meeting.

AUDUSD chopped about in a 0.6561-0.6600 range, with price action determined by the prevailing US dollar sentiment.

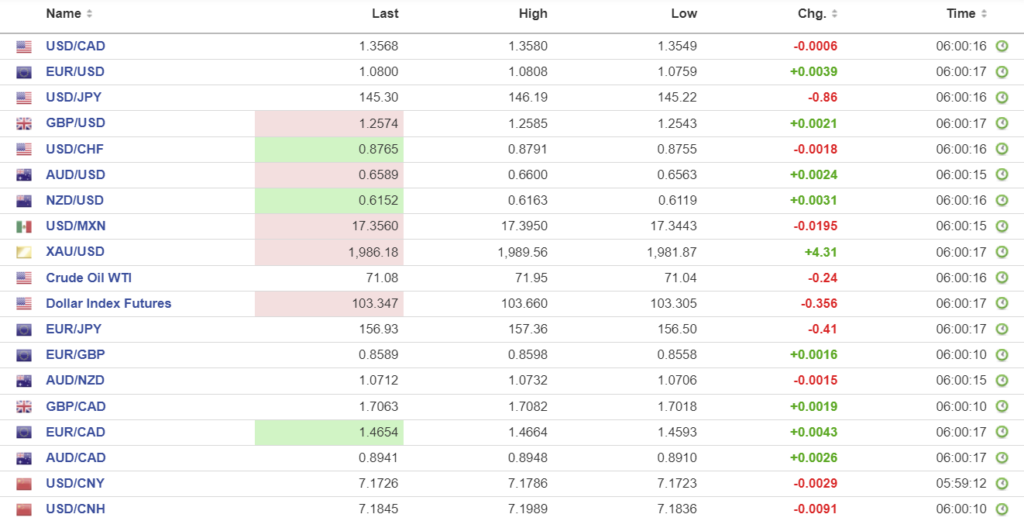

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1174, expected 7.1772, previous 7.1163.

Shanghai Shenzhen CSI 300 rose 0.21% to 3426.80.

Chart: USDCNY and USDCNH

Source: Investing.com