May 15, 2024

- CPI cools modestly-Markets ecstatic

- Retail sales are flat (forecast 0.4% m/m)

- USD opens lower then plunges post-CPI

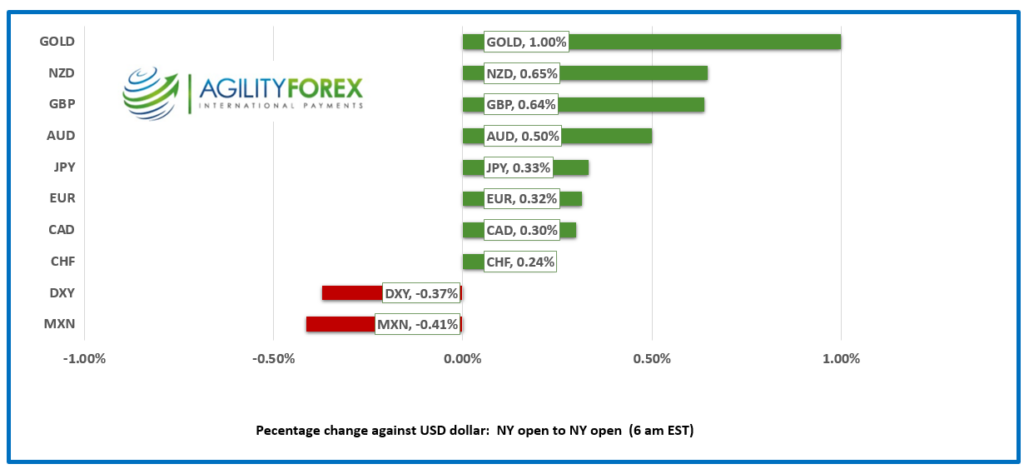

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3630, overnight range 1.3591.3656, close 1.3653

USDCAD dropped to 1.3591 from 1.3633 in the wake of the modestly better US inflation report. However, the move was mostly reversed within minutes reaching 1.3622, mainly because the Fed will not react to just one data point, especially one whose improvement was underwhelming.

Overnight, USDCAD retreated due to broad-based US dollar selling with additional pressure stemming from a further narrowing of CAD/US interest rate differentials. The prospect of Bank of Canada easing well ahead of a similar Fed move should limit the downside.

WTI oil prices fell from 78.75 to 77.97 despite API weekly inventory data showing US crude stocks fell by 3.10 million barrels last week. It was the latest International Energy Agency (IEA) forecast for 2024 oil demand that spooked traders. The IEA is forecasting that 2024 global demand will fall by 140,000 barrels /day due to weak demand which contradicts the Opec forecast of a 2.25 mb/d increase. Nevertheless the increase or decrease is merely a rounding error in the context of global crude production of 102.9 mb/d.

Manufacturing Sales fell 2.1% m/m in March.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3680 and looking for a break of support in the 1.3620 area to extend losses to 1.3560. A move above 1.3680 negates the downtrend and targets 1.3860.

The longer term technicals are bullish above 1.35660 which gets additional support as it is also the 200 day moving average.

For today USDCAD support is at 1.3620 and 1.3580. Resistance is at 1.3670 and 1.3710. Today’s range is 1.3580-1.3680.

Chart: USDCAD 4 hour

Source: DailyFX

Wet Blanket Powell and CPI

Trade rooms are hopping like a 70’s era disco thanks to modestly better April CPI data. Headline CPI rose 0.3% m/m a tick less than expected and below the 0.4% result in March. Core CPI rose 3.4% as expected but below the 3.5% y/y previously.

Oh joy! The results are hardly earth shattering and are not likely to cause Fed Chair Jerome Powell to improve his confidence in the Feds interest rate outlook. Yesterday he said that policymakers will stick to a “wait and see” approach to monetary policy.

US Retail Sales were flat in April compared to the forecast for a 0.4% rise.

Equities find their footing.

Asian equity indexes closed mixed. Australia’s ASX 200 gained 0.35%, Japan’s Nikkei 225 index was unchanged, and Chinese stock markets fell. European bourses extended gains, post-CPI, led by a 0.85% rise in the German Dax. S&P 500 futures jumped 0.42% after the CPI data. The US 10-year Treasury yield dropped to 4.34% from 4.424%.

EURUSD

EURUSD climbed from 1.0813 to 1.0835, supported by better-than-expected March Industrial Production data (actual 0.6% vs forecast 0.5% and February 1.0%) alongside steady employment and Q1 GDP at 0.4%. Prices rallied to 1.0869 after the US data. The short-term technicals are bullish above 1.0750, looking for a move above 1.0890 to target 1.0970.

GBPUSD

GBPUSD traded quietly in Asia before catching a bid in Europe and rallying from 1.2582 to 1.2625 into the NY open then surging to 1.2670 after US CPI and Retail Sales. The currency pair shrugged off dovish comments from BoE Chief Economist Huw Pill, who yesterday suggested rate cuts were possible in the summer. Instead, traders are looking ahead to a lower US CPI reading today, which would lead to broad US dollar selling pressures. The medium-term GBPUSD technicals are bullish above 1.2510, looking for a break above 1.2710 to extend gains to 1.2820.

USDJPY

USDJPY traded sideways in Asia then plunged from 156.56 to 155.74 in Europe before falling to 154.76 post-CPI. The losses were exacerbated by the plunge in the US 10-year Treasury yield to 4.34% from 4.445% at yesterday’s close.

AUDUSD AND NZDUSD

AUDUSD traded firmer in a 0.6622-0.6652 range then rallied to 0.6680, supported by US data and news about potential new China fiscal stimulus. Traders ignored the slowing Australian wage growth data.

NZDUSD rallied from 0.6029 to 0.6101 due to broad US dollar weakness.

USDMXN

USDMXN consolidated yesterday’s gains in a 16.8186-16.8795 range. Gains are limited due to ongoing hopes for robust economic growth and the recovering tourism sector. However, the downside is supported by speculation that Banxico cuts rates in June and by concerns the Fed will leave rates unchanged until at least November.

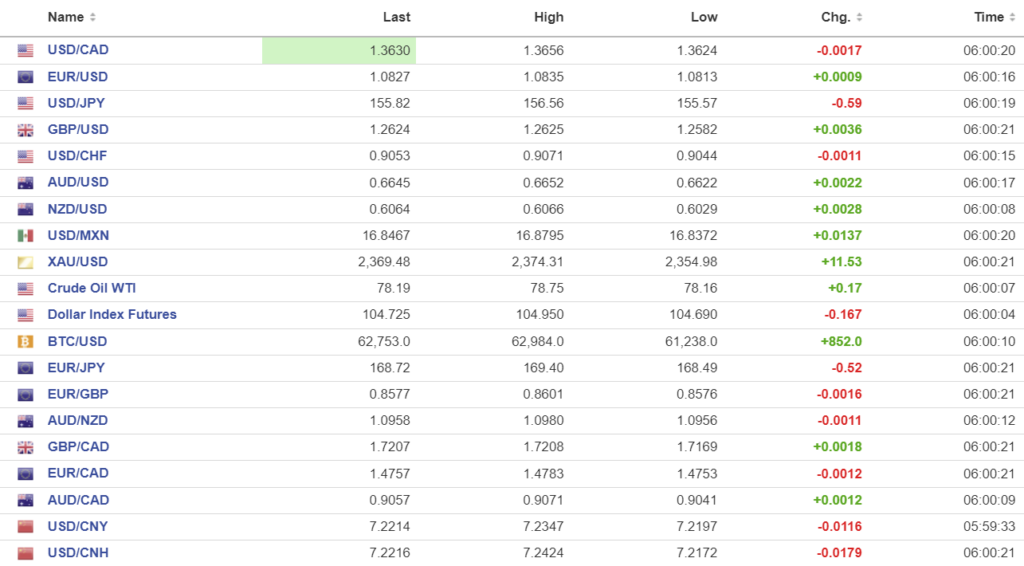

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1049 (forecast 7.2279) prev. 7.1053.

Shanghai Shenzhen CSI 300 fell 0.85% to 3626.06.

PBoC leaves 1-year MLF rate unchanged at 2.5%. Analysts suggest the decision is evidence that authorities want to boost the economy through fiscal measures rather than risk destabilizing the currency by cutting rates.

Chinese authorities are considering a proposal to buy unsold houses at discounted prices from distressed developers.

Chart: USDCNY and USDCNH

Source: Investing.com