Source: Adobe Stock

- Aggressive Fed rate hike fears fuel further dollar rally

- British pound hits 37 year low

- US dollar rallied on fears of sharply higher US rates

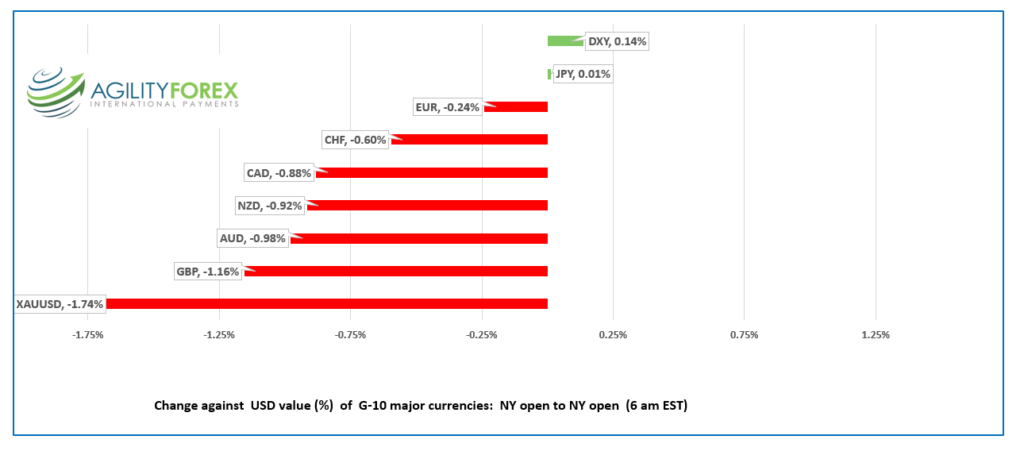

FX at a glance:

Source: IFXA Ltd/RP

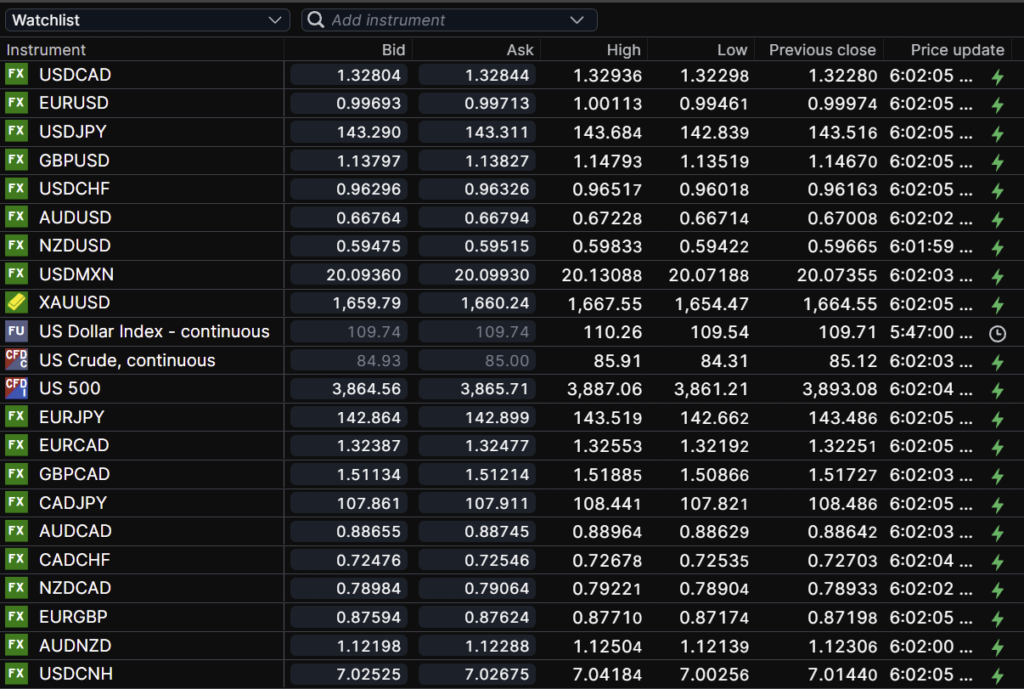

USDCAD Snapshot: open 1.3280-84, overnight range 1.3230-1.3306, close 1.3228

USDCAD caught a bid yesterday and continued climbing overnight. It is a broad US dollar move, domestic influences including the Bank of Canada’s rate hike plans did not enter into the equation.

The rally occurred even though yesterday’s US data was mixed. Retail rose 0.3% which was not enough to recover the 0.4% slide in July which some believed would temper forecasts for aggressive Fed action next week.

It didn’t. Traders still believe the Fed will hike rates 0.75 bps next week but the odds for a 100 bp bump dropped from 31% to 26.5%. Nevertheless, analysts have amended their Fed funds peak rate forecasts to 4.5% from 4.0%. Ray Dalio, founder of hedge fund Bridgewater predicted that a 4.5% rate would knock equities down by 20%/

The US 2’s-10’s yield curve is inverted and expected to drop to levels last seen since 1985, which ING economists claim is the reason for the US dollar strength.

USDCAD may be getting further support from the slide in WTI oil prices, although the latest drop is just a correction while prices are above $76.00/barrel.

Prime Minister Trudeau declared Monday September 19 a federal holiday and day of mourning for Queen Elizabeth. Except it is only a holiday for federal politicians and direct federal employees. In BC, Premier John Horgan is giving provincial public sector workers the day off. Not so in Ontario. Premier Doug Ford skipped the whole holiday thing and said people should observe a moment of silence, prompting one Twitter user to call it “Go to work and cry at your desk” day.

August Housing Starts rose 267,400 y/y compared to 275,200 in July. Wholesale Sales data fell 0.6% m/m, as expected.

USDCAD Technical outlook

The intraday USDCAD are bullish, short, medium, and long term. Yesterday’s decisive break above resistance in the 1.3205-20 area touched 1.3294 overnight. A topside break of that level suggests a straight shot to 1.3370, then a test of major resistance at 1.3460, which is the 61.8% Fibonacci retracement of the 2002-2007 range.

A decisive break above 1.3460 puts the 2020 Covid peak of 1.4660.

For today, USDCAD support is at 1.3220 and 1.3170. Resistance is at 1.3310 and 1.3370. Today’s range: 1.3240-1.3330

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar is on a tear after Wall Street tumbled yesterday and S&P 500 and DJIA futures extended losses overnight.

The rally is due to speculation US interest rates will rise sharply higher as inflation has not peaked. US yield curve inversion, geopolitical tensions, and a sharp divergence between economic growth in the US and many G-10 countries underpin prices.

The major Asian equity indexes closed with losses. Japan’s Nikkei 225 index fell 1.1%, a much better performance than China’s Shenzhen CSI 300 index, which fell 2.31%. The German Dax index is down 1.26%, while the UK FTSE 100 is 0.19% higher. WTI oil prices are a tad higher compared to the NY close, while gold lost more ground overnight.

The 10-year Treasury yield is sitting at 3.471%.

EURUSD rallied was volatile and whipped around in a 0.9946-1.0011 range. Eurostat reported, “The euro area annual inflation rate was 9.1% in August 2022, up from 8.9% in July. A year earlier, the rate was

3.0%. European Union annual inflation was 10.1% in August 2022, up from 9.8% in July. A year earlier, the rate. Higher energy prices were primarily to blame. Prices got a bit of support after ECB President Christine Lagarde implied Eurozone rates would rise despite the implications for growth as fighting inflation was more important.

GBPUSD is dropped to a 37-year low, falling from 1.1479 to 1.1352, and sentiment remains bearish. UK data didn’t help. Retail Sales fell 5.4% y/y in August compared to a 3.2% drop in July.

The technical picture is bearish, with a decisive breach of 1.1350 extending losses to 1.1120.

USDJPY climbed from 142.84 to 143.68, where the rally stalled. Firm US Treasury yields underpin prices while intervention fears cap gains.

AUDUSD dropped from 0.6723 to 0.6671 due to weaker commodity prices and widespread US dollar demand. The negative pressure was exacerbated after RBA Governor Philip Lowe’s hinted that the pace of rate hikes might be eased in October.

Michigan Consumer Sentiment index is ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

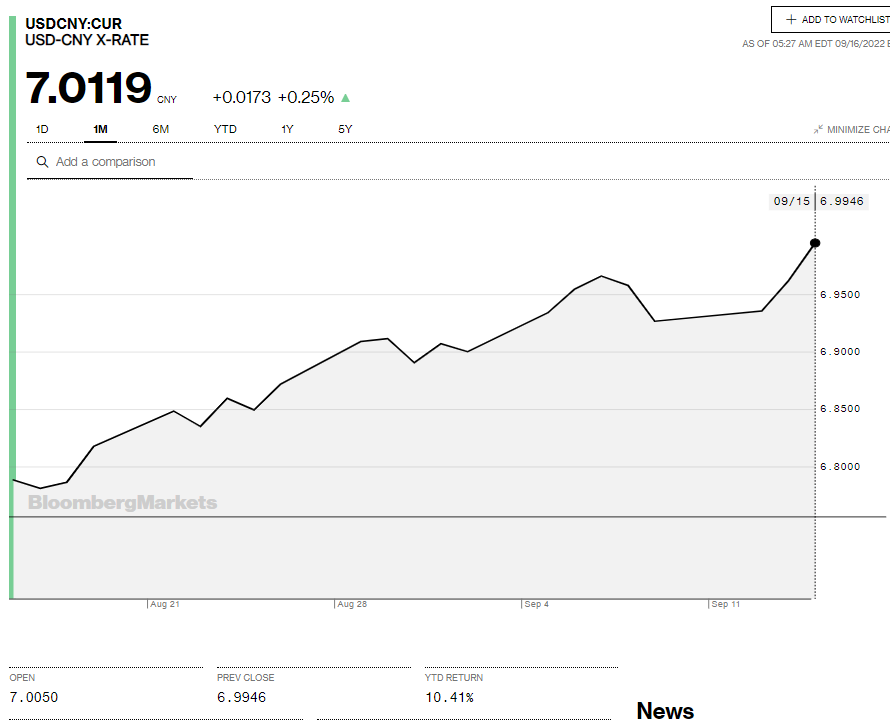

China Snapshot

Today’s Bank of China Fix: 6.9305, previous 6.9101

Shanghai Shenzhen CSI 300 fell 2.35% to 3,932.68

August Retail Sales 5.4% y/y vs July 2.7% y/y

August Industrial Production 4.2% vs July 3.8%

Report from China Securities Daily suggests lending rates may decline further

Chart: USDCNY 1 month

Source: Bloomberg