Photo: Wikipedia.org

May 2, 2023

- Eurozone inflation rises and EURUSD sinks.

- RBA surprises with a 25 bp rate hike

- US dollar opens higher compared to Monday; AUDUSD outperforms.

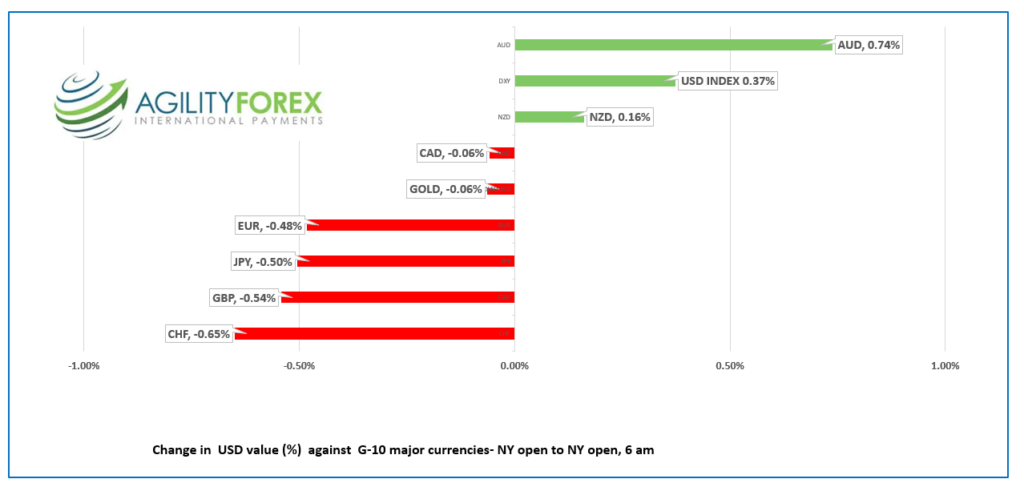

FX at a glance

Source: IFXA Ltd/RP

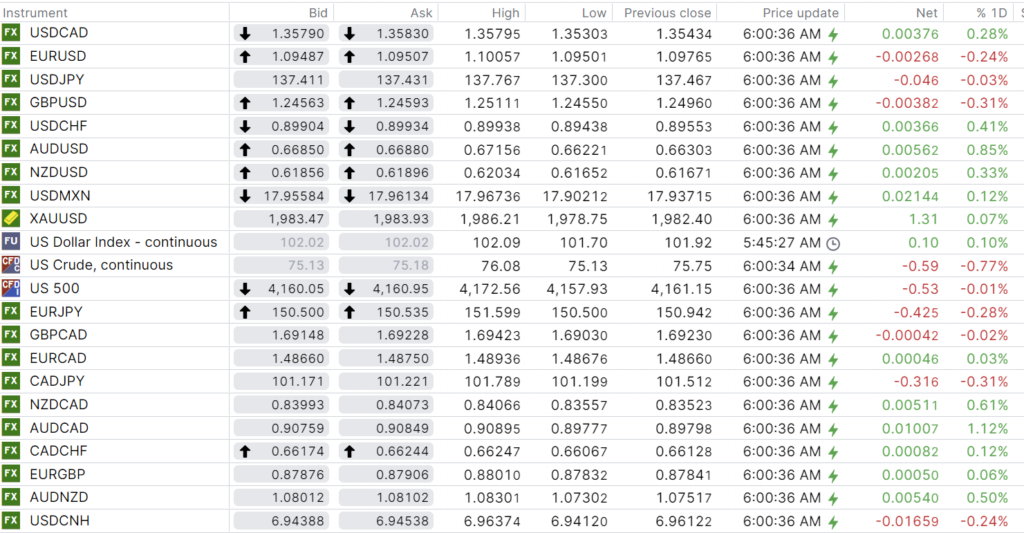

USDCAD Snapshot: open 1.3579-83, overnight range 1.3530-1.3585, close 1.3543

USDCAD closed with a bearish bias on Monday but that changed in Europe after Euro area inflation data sparked broad US dollar demand against the G-10 major currencies. USDCAD rallied to 1.3583 in early NY, with direction determined solely by broad US dollar sentiment.

The public workers strike ended with employees reluctantly accepting a 12.5% wage hike over three years. The strikers also received a one-off $2,500 lump sum pension payment which is really the government’s way of paying their wages while they were on strike.

Oil prices are not doing much for USDCAD. WTI traded choppily in a $75.09-$76.08 range due to broad US dollar strength and concerns of reduced demand because of slowing global growth.

There are no Canadian economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals turned bearish with the break below 1.3580 on Friday which snapped the two-week uptrend from 1.3305. USDCAD is looking for a move above 1.3660 to target 1.3860.

Longer term, USDCAD failed to sustain losses below the 200 day moving average which sits at 1.3433 and has not been much below the 100-day moving average (1.3524) since its topside break on April 21.

USDCAD is trading just below the middle of its 1.3300-1.3560 range that has contained price action since March 10. That won’t change today.

For today, USDCAD support is at 1.3530 and 1.3510. Resistance is at 1.3590 and 1.3610

Today’s range 1.3530-1.3610

Chart: USDCAD 1 day

Source: Saxo Bank

G-10 FX recap and outlook

Many traders are biding their time until tomorrows FOMC meeting leaving the rest to react to headlines.

JP Morgan Chase CEO Jamie Dimon declared the US banking crisis over which gave US stocks a bit of a lift, although many investors are not so sure.

Treasury Secretary Janet Yellen warned the US would default on its debt by June 1. Markets are not really concerned as a US debt-ceiling crisis is as much a part of government theatrics as the stand, clap, sit calisthenics are to a State of the Union address.

The major Asian equity indexes closed on a mixed note. Japan’s Nikkei 225 index finished with a 0.12% gain while Australia’s ASX 200 dropped 0.92%. S&P 500 futures are modestly lower, down 0.12% (as of 7:10 am ET).

European bourses opened after the long weekend and are trading in negative territory led by a 0.52% fall in the French CAC-40 index.

EURUSD rose steadily from yesterday’s NY close of 1.0977 to 1.1006 then plunged to 1.0949 after Eurostat released inflation data for April. The headline Harmonized Index of Consumer Prices (HICP) was hotter than expected (7.0% y/y vs forecast 6.9%), but that was ignored. Traders focused on Core HICP which was lower than forecast (actual 5.6% y/y vs forecast 5.7%).

The EURUSD retreat was because traders feared that the inflation results would lead to a somewhat dovish ECB monetary policy decision on Thursday.

GBPUSD traded sideways in Asia then fell from 1.2511 to 1.2455 in early NY trading, mainly because EURUSD came under pressure. GBPUSD saw a little support early in the session after the Nationwide Housing Price index rose 0.5% m/m in April (forecast -0.4%).

However, that support evaporated after the S&P Global Manufacturing PMI (actual 47.8 vs forecast 46.6, March 46.6) showed the UK was still shrinking.

USDJPY rose from 137.30 to 137.77 just before Europe opened, then drifted back to 137.42 in early NY, when the US 10-year Treasury yield fell from 3.60^ to 3.532%.

The prospect of further US rate hikes while the BoJ leaves monetary policy unchanged is exacerbating the rally.

AUDUSD rallied sharply, rising from 0.6622 to 0.6716 in the wake of a hawkish RBA monetary policy meeting, and is consolidating the gains in a 0.6674-.6716 range.

The RBA surprised a majority of traders and analysts when they hiked rates 25 bps to 3.85%. Governor Philip Lowe said the decision was due to sticky inflation and a tight labour market. It was also not the last hike. The Governor said, “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe.”

Factory orders and JOLTS job openings are on tap.

FX open, high, low, previous close as of 6:00 am ET

China Snapshot

Bank of China Fix: 6.9240, closed.

Shanghai Shenzhen CSI 300 closed: 4029.09.

China on National holiday from May 1-3.

Chart: USDCNH 4 hour

Source: Saxo Bank