May 6, 2024

- Risk sentiment is mildly positive in holiday thinned trading.

- US 10-year Treasury yield consolidating Friday’s drop.

- USD dollar opens lower except against CAD and JPY.

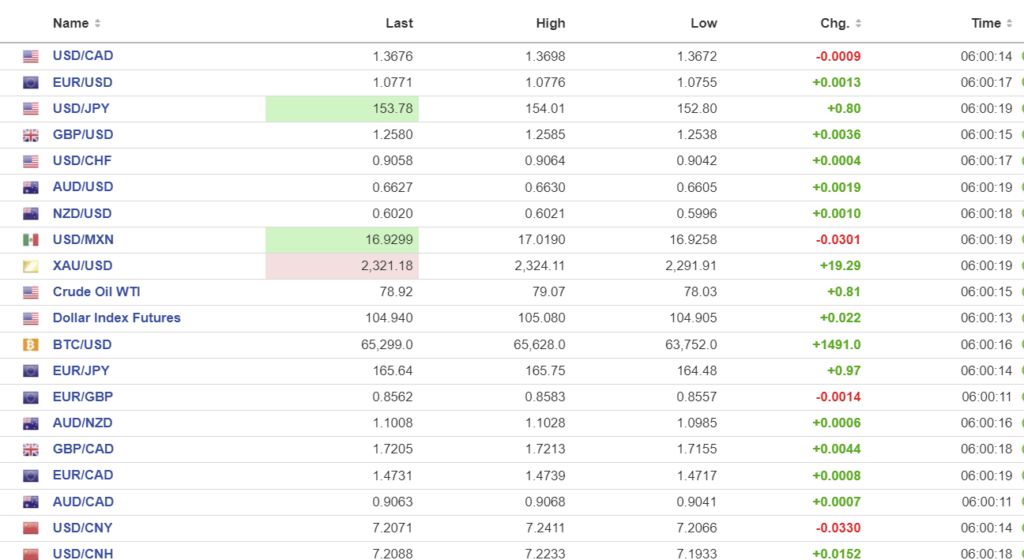

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3676, overnight range 1.3672-1.3698, close 1.3687

On Friday, USDCAD plummeted on the heels of the weaker than expected US nonfarm payrolls report, falling from 1.3689 to 1.3610 but quickly retraced the entire move.

The NFP data encouraged bets that the Fed would be cutting rates in 2024, maybe even earlier than in November. Numerous Fed officials may have something to say on that topic throughout this week. Even so, traders do not expect more than two rate cuts and if they occur it will be long after the Bank of Canada cuts rates, as early as June 5.

WTI oil prices traded in a 78.03-79.07 range supported by ongoing tensions in the Middle East. Israel plans to cleanse Rafah of Hamas and has told non-combatants to flee. The downside may be limited due to speculation of new production cuts by Opec and because Saudi Arabia hiked crude prices.

USDCAD Technicals

The intraday USDCAD technicals are bearish while prices are below 1.3690 and looking to revisit support at 1.3610. A break above 1.3690 targets 1.3750.

The USDCAD uptrend line from the beginning of the year comes into play at 1.3560 and it is guarded by a slew of previous tops in the 1.3600-10 zone.

For today USDCAD support is at 1.3640 and 1.3610. Resistance is at 1.3690 and 1.3750. Today’s range is 1.3620-1.3720-1.3660.

Chart: USDCAD 1 day

Source: DailyFX

Shh! Traders Sleeping.

It was a very quiet start to the week. Top-tier US economic reports have gone missing in action this week, much like the Toronto Maple Leaf Stanley Cup hopes, which disappeared for the 57th consecutive time. Australian, Japanese, and South Korean markets were closed as were those in the United Kingdom. But all is not lost. The Reserve Bank of Australia (RBA) and Bank of England monetary policy meetings will entertain traders tomorrow and Thursday.

The US dollar remains on the defensive after Friday’s weaker than expected showed that the labour market is weakening. There will be more on that subject this week from a host of FOMC policymakers.

EURUSD

EURUSD traded in a 1.0755-1.0776 range supported by broad US dollar weakness and weaker than expected Eurozone PPI data. Industrial producer prices decreased by 0.4% in the euro area and by 0.5% in the EU, according to first estimates. The prospect of narrowing ECB and Fed interest rate differentials has the short term EURUSD technicals in an uptrend above 1.0680.

GBPUSD

GBPUSD climbed in a 1.2538-1.2585 range in thin trading as UK markets were closed. The Bank of England is expected to leave rates unchanged at this week’s meeting and indicate that rates will stay at current levels for a while longer. The intraday technicals are bullish but the March downtrend line, currently at 1.2640, may cap rallies.

USDJPY

USDJPY traded in a 152.80-154.01 range but gains were capped by ongoing intervention fears, a lower US 10-year Treasury yield (actual 4.73%) and by downtrend resistance at 155.60.

AUDUSD and NZDUSD

AUDUSD drifted in a 0.6605-0.6630 range with local markets closed for Labour Day. TD Securities Inflation was unchanged at 0.1%. Tomorrow, the RBA is expected to remind markets that they are content to monitor incoming data and leave rates unchanged.

NZDUSD rose to 0.6024 from 0.5996 thanks to the generally soft US dollar.

USDMXN

USDMXN traded defensively in a 16.9203-17.0190 range due to broad-based US dollar selling pressures. Mexican Consumer Confidence data is due tomorrow.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

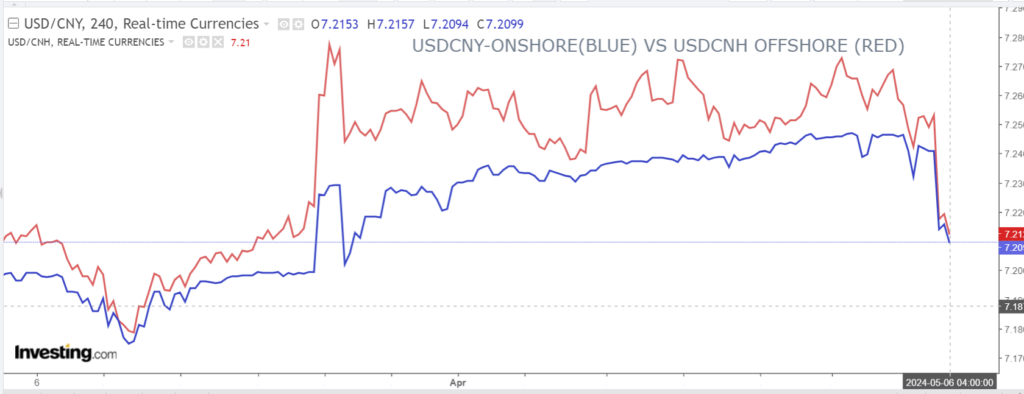

China Snapshot`

PBoC fix: 7.0994 vs exp. 7.2127 (prev. 7.1063)

Shanghai Shenzhen CSI 300 rose 1.48% to 3657.88

Caixin Services PMI was 52.5 in April, as expected. S&P Global wrote: “The Caixin China General Manufacturing PMI came in at 51.4 in April, up 0.3 points from the previous month, the highest reading since February 2023. It also marked the sector’s sixth consecutive month of growth as the overall market continued to improve. Both supply and demand expanded at a faster pace amid the market upturn.”

Chart: USDCNY and USDCNH

Source: Investing.com