Source: BBC

- Markets befuddled by hawkish/dovish Fed debate

- Eurozone inflation higher than expected

- US dollar opens mixed, Kiwi outperforms

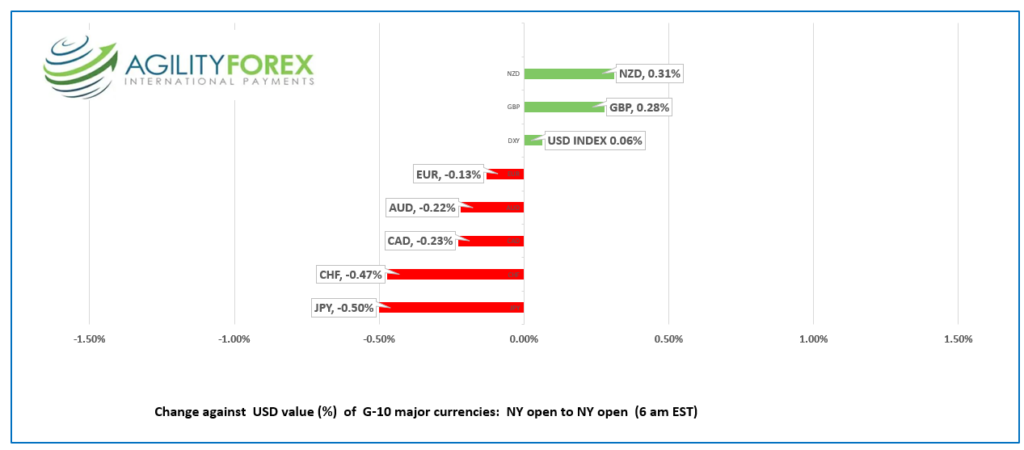

FX at a glance:

Source: IFXA Ltd/RP

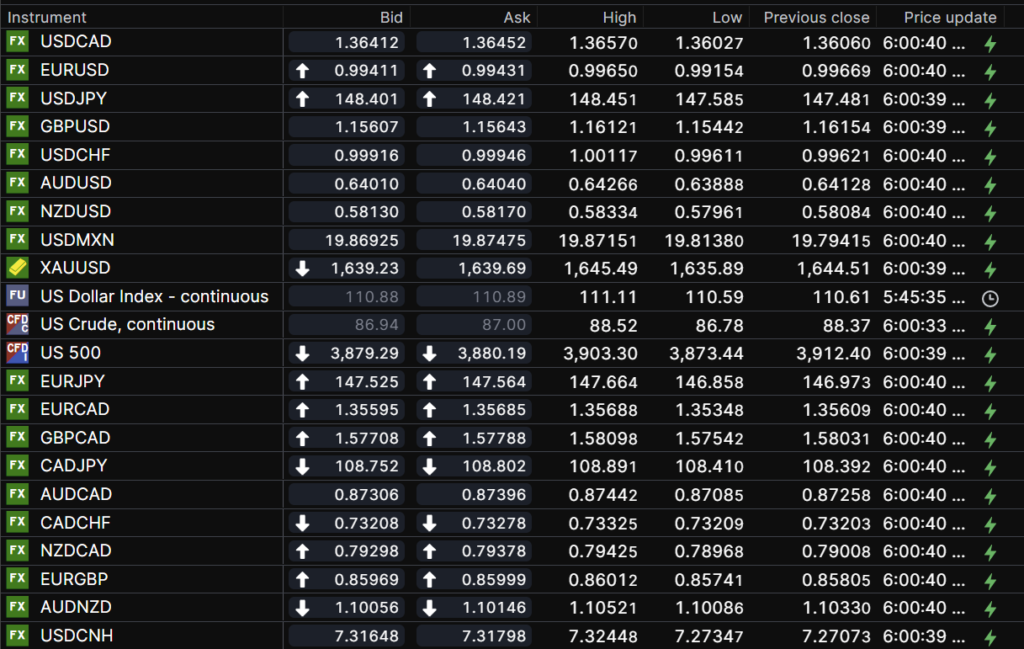

USDCAD Snapshot: open 1.3641-45, overnight range 1.3603-1.3671, close 1.3606

Canadian dollar traders are the Charlie Brown of G-10 currencies. The currency is often pessimistic, occasionally optimistic but generally hopes for the best.

The evidence was on display last week when traders went trick or treating to the Bank of Canada door. They expected a 75 bp rate increase into their goodie bags. Instead, they got a rock or in this case a 50 bp bump. That’s a Charlie Brown trick or treating moment.

A more aggressive Fed and a more timid BoC suggest further gains for USDCAD.

WTI oil prices rose to $88.52 then dipped to $86,33/b. Supply fears due to the 2.0 million b/day tomorrow’s Opec production cuts were more than offset by weaker Chinese PMI data reinforcing global slowdown concerns.

USDCAD Technical outlook

The intraday USDCAD are bullish above 1.3605 looking for a break above 1.3690 to extend gains to 1.3750.

The USDCAD downtrend channel from the October 13 peak is intact while prices are below 1.3690. Failure to break above this level suggests a retreat to the bottom of the channel at 1.3420.

For today, USDCAD support is at 1.3620 and 1.3590. Resistance is at 1.3690 and 1.3750. Today’s range 1.3610-1.3710.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

FX markets didn’t get much traction from weekend events when Asia opened.

Russia is playing “silly buggers” with grain shipments and Ukraine is calling for more G-10 aid. Brazilians are on the march, Left, right, left. Former President Luiz Lula De Silva returns to the Presidents chair four years and a 580-day prison term, winning a not-so-commanding 50.9% of the vote.

Weaker than expected Chinese PMI data kept the focus on slowing global growth, while FX traders jockeyed for position ahead of today’s month-end portfolio rebalancing flows, and caution ahead of Wednesday’s FOMC meeting.

Wall Street Journal reporter Nick Timiraos described by many as the “Fed Whisperer,” appears to whisper out of both sides of his mouth. Last week he opined that the Fed would be discussing how to signal a slower pace of rate hikes. On the weekend, he wrote that Fed officials were thinking Cash rich consumers could mean higher rates for longer.

Goldman Sachs economists’ kind of agree. They raised their forecast for peak Fed rates to 5.0% by March 2023.

Asian equity markets closed mixed. The Nikkei 225 and Australian ASX 200 were higher while Chinese markets were in the red. European bourses flitting between positive and negative in quiet trading and S&P 500 futures are down 0.54%.

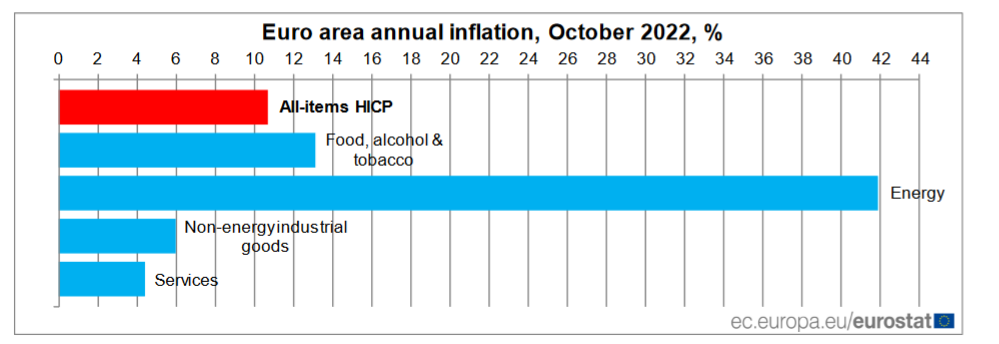

EURUSD traded sideways in Asia then dropped from 0.9965 to 0.9915 in Europe before climbing to 0.9947 when NY opened. Eurozone inflation was hotter than expected, rising 10.7% y/y in October (forecast 9.8%) and 1.5% m/m (forecast 0.6%). GDP rose2.1% as expected

Source: eurostat

The higher-than-expected results support ECB Governing council member and Dutch Central Bank head Klaas Knot comment that a third 75 bp increase would be possible but “We still have six more weeks to go and there are still a lot of economic numbers coming out.” The short term EURUSD technicals are bullish above 0.9830 looking for a break above 1.0100 to target 1.0350.

GBPUSD is at the bottom of its 1.1517-1.1612 overnight range with prices tracking broad US dollar moves. Traders are focused on Wednesday’s Fed meeting and Thursday’s Bank of England meeting. Analysts are debating whether the BoE will hike 50 or 75 bps.

USDJPY rallied from its Asia low of 147.59 to 148.78 in NY, supported by the gain in the US 10-year yield from 4.017% to 4.054%. in NY

AUDUSD Is at the bottom of its 0.6382-0.6427 range despite expectations for the RBA hike rates by 25 bps tomorrow as inflation is well above its 2022 target. Australian Retail Sales data was ignored even though sales rose 0.6% in September.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

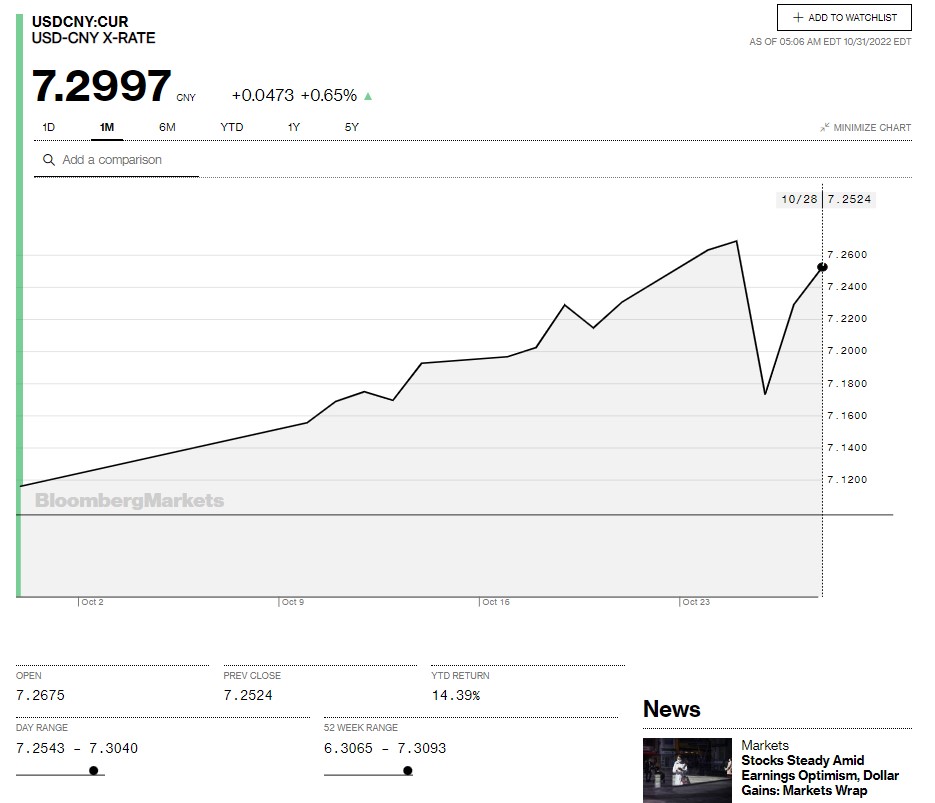

China Snapshot

Today’s Bank of China Fix: 7.1768, previous 7.1698

Shanghai Shenzhen CSI 300 fell 0.92% to 3508.70

October NBS Manufacturing PMI 49.2 (forecast 50, September 50.1)

Non-manufacturing PMI (48.7 (forecast 51.9, September 50.6)

Stocks continue to be sold due to on-going COVID lockdowns. China is forcing millions of people to stay home because 0.00018% of the population test positive for COVID.

Chart: USDCNY 1 month

Source: Saxo Bank