Source: memegenerator.net

- Powell’s new hawkish persona spooks markets

- Wall Street’s Santa rally hits Omicron wall

- US dollar steady ahead of Friday’s NFP report

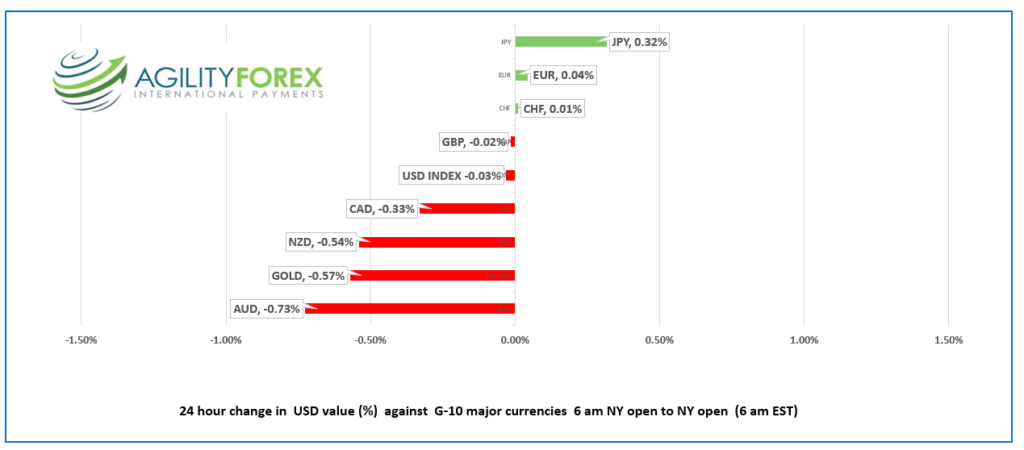

FX at a Glance:

Source: IFXA Ltd/RP

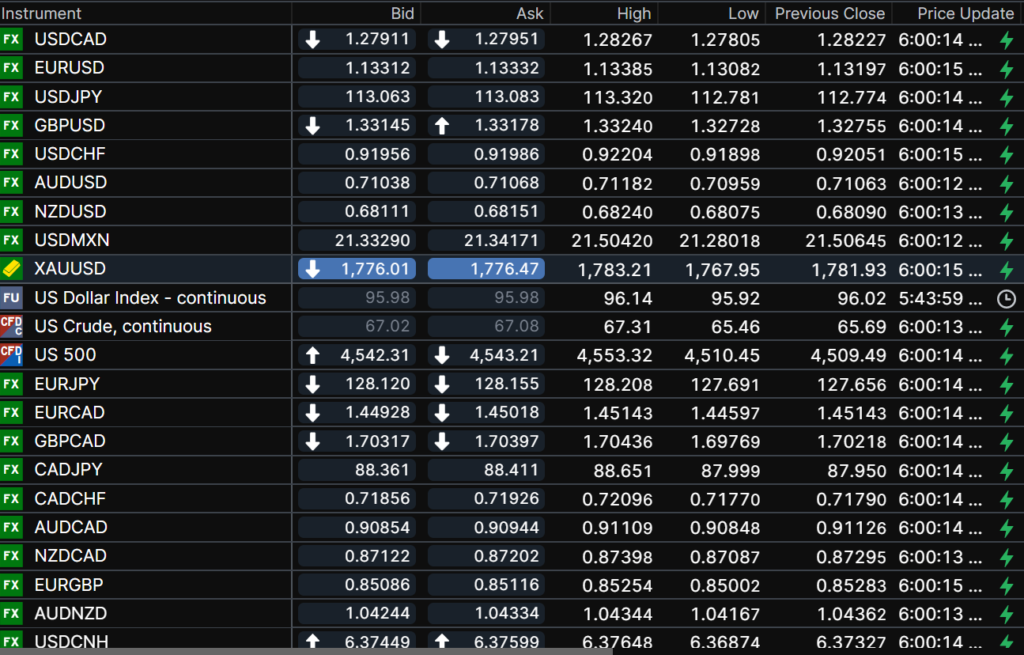

USDCAD Snapshot Open 1.2798-02, Overnight Range 1.2781-1.2827, Previous close 1.2823

USDCAD gains are exacerbated by falling oil prices. WTI oil dropped to $64.90/barrel yesterday as traders worry that Opec will announce plans to further increase production in January, as scheduled. The cartel is expected to announce their decision today. WTI Fibonacci retracement analysis of the October 2020-October 2021 range warns that a decisive breach of $66.00/b targets $54.21/b

On the other hand, many economists expect the Bank of Canada to raise rates in Q2 2022, which should be a drag on USDCAD gains. That view will garner additional support if Friday’s Canadian employment report exceeds expectations.

Technical view: The intraday USDCAD technicals are bullish above 1.2750, looking for a break above 1.2850 to extend gains to 1.3000. A break below 1.2950 will alleviate the upward pressure and suggest 1.2650-1.2850 consolidation.

For today, USDCAD support is at 1.2750 and 1.2710. Resistance is at 1.2850 and 1.2890. Today’s Range 1.2750-1.2870.

Chart USDCAD and WTI 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

There is no shortage of hyperbole in the financial media lately. The news of the COVID-19 omicron variant and Fed Chair Powell changing his view on US inflation tipped the financial press into panic mode. Headlines shouted, “The Dow Plunges,” while TV talking heads regurgitated numbers while wearing their most serious faces.

The reality is “it ain’t that bad.” The S&P 500 dropped 3.8% from November 24 to December 1 but has risen 20.15% since closing December 31, 2020. That’s a pretty good performance for an index with 10-11% historical returns between 1928 and 2018.

Nevertheless, news of the first US Omicron case awoke memories of the 2020 COVID-19 plunge that knocked the S&P 500 down around 35% within a month.

More than likely, it was Fed Chair Powell’s response to a question on day two of his congressional testimony. Asked if he still believed price increases are not particularly large or persistent, he answered, “No. that is no longer my view.” Those words and his Tuesday comment suggesting it was appropriate to end tapering earlier are behind the market turmoil, more so than omicron.

US weekly jobless claims rose 222,000, lower than the forecast but higher than last week’s downward revised result of 194,000.

Asia equity indexes closed with small losses except those in China and Hong Kong. European indexes are down, led by a 1.09% drop in the German Dax. Wall Street futures are clawing back some of yesterday’s losses. Gold and oil prices are trading higher as well. The US 10-year yield bounced from the overnight low of 1.404% to 1.438%.

EURUSD is rangebound in a 1.1308-1.1343 band with a modest bullish bias targeting 1.1380. Better than expected Eurozone October PPI data (actual 5.4% m/m vs forecast 3.5% m/m) provided a little support. However, traders are content to await Friday’s Eurozone Retail Sales and Services PMI data as well as the US NFP report.

GBPUSD is at the top of its overnight 1.3273-1.3332 range, helped by a slide in EURGBP and improved global risk sentiment. Traders are still debating whether the Bank of England will hike rates on December 16 or wait until January.

USDJPY traded in a 112.78-113.32 range, undermined by both falling US Treasury yields and safe-haven demand for yen due to the Omicron variant.

AUDUSD and NZDUSD were rangebound with prices supported by the mildly improved risk tone. Both currency pairs have retreated to session lows in early NY trading.

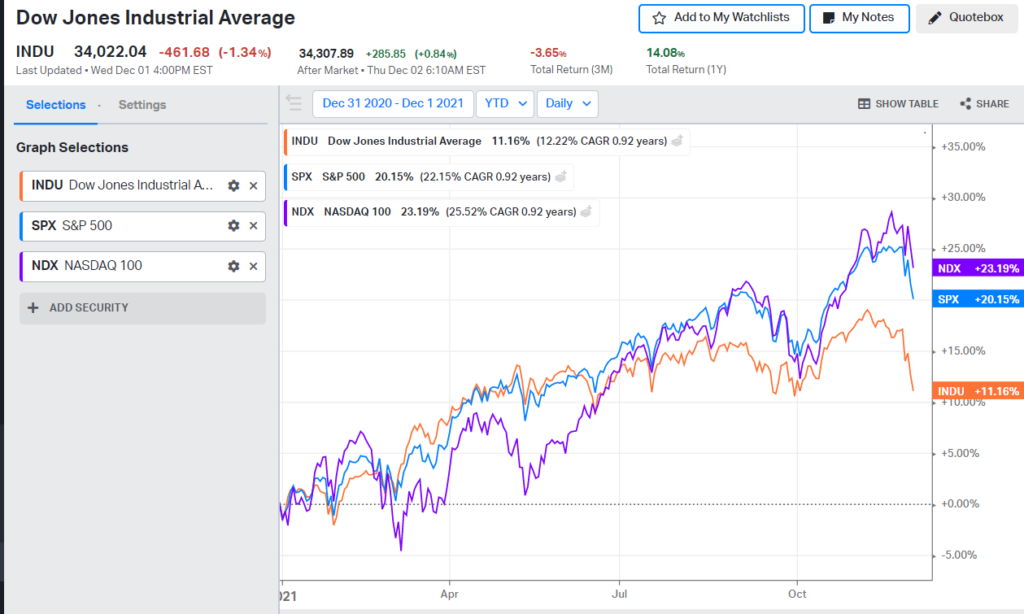

Chart of the Day: US Equities YTD

Source: Koyfin.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

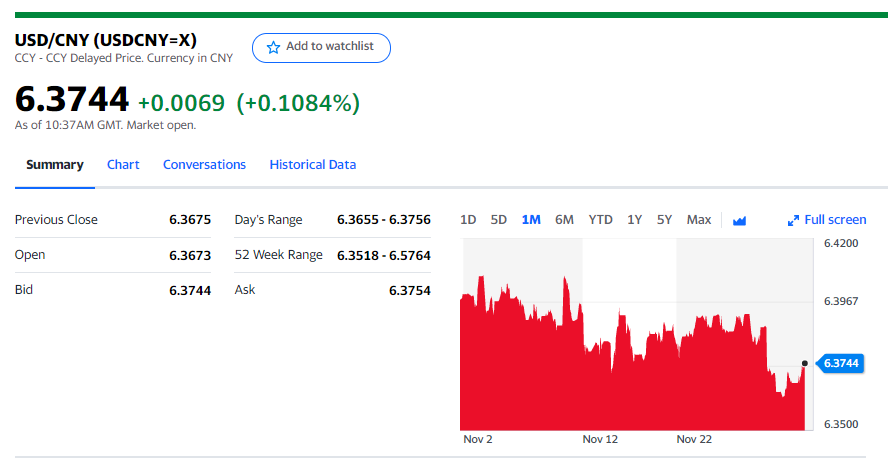

China Snapshot

Today’s Bank of China Fix 6.3719 Previous 6.3693

Shanghai Shenzhen CSI 300 rose 0.25% to 4,856.16

Chart: USDCNY 1 month

Source: Yahoo Finance