Source: Pixabay

- FOMC and geopolitics keeping traders on edge

- European stocks higher even as Wall Street futures retreat.

- US dollar opens firm, AUD outperforms

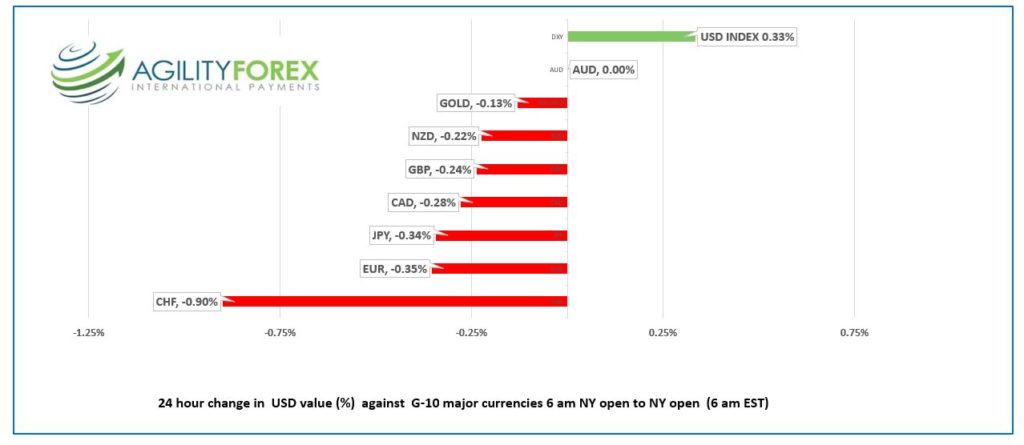

FX at a Glance

Source: IFXA Ltd/RP

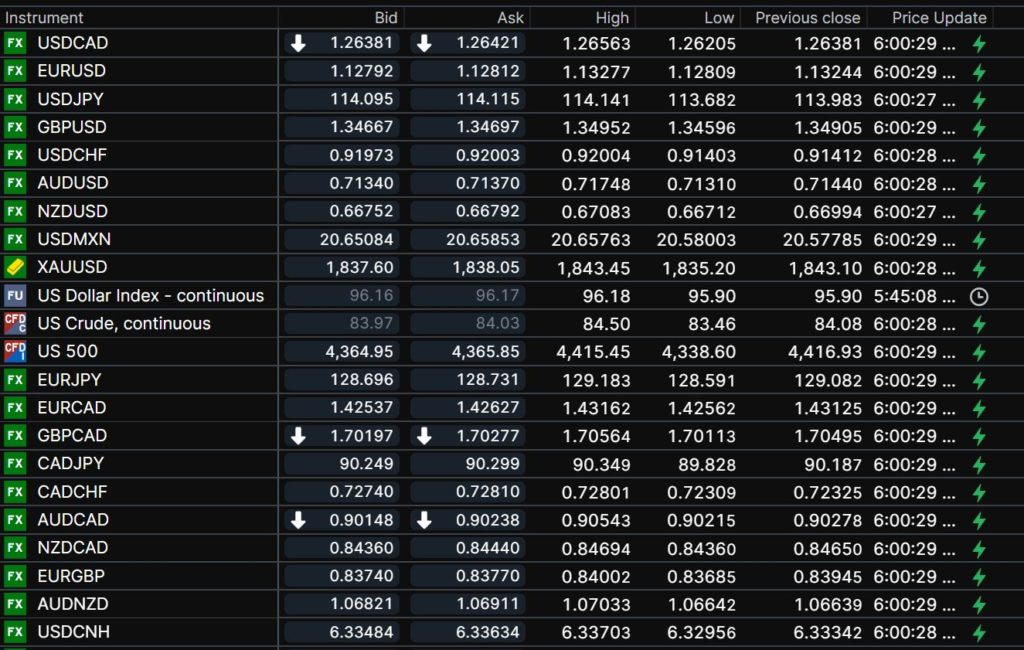

USDCAD Snapshot: Open 1.2638-42, Overnight Range-1.2621-1.2656, previous close 1.2638

USDCAD touched 1.2700 yesterday due to broad risk aversion sentiment overshadowing firm oil prices and Brank of Canada rate hike risks. The domestic currency is an after thought in the global arena and that won’t change today.

Prime Minister Trudeau promises troops and money for the Ukraine and then Canada’s Foreign Affairs Ministry is hit by a cyber-attack. Nothing to fear, it was probably done by disgruntled truckers.

Oil prices will continue to act as a drag on USDCAD gains. Even though they are down from last week’s $87.82 peak, the current level of $83.35is still 10% higher than where it was at the start of the year. Ongoing Middle East tensions, and expectations for a resurgence of demand will continue to support prices.

Technical view: The intraday USDCAD technicals are bullish above 1.2605, looking for a break above 1.2700 to extend gains to 1.2800. A move below 1.2590 suggests further losses to 1.2500.

For today, USDCAD support is at 1.2620 and 1.2590. Resistance is at 1.2660 and 1.2700. Today’s Range 1.2610-1.2690.

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

There’s a kind of a hush all over Wall Street this morning. That’s mainly because those enroute to offices haven’t arrived, but also because European stocks and US equity futures trading is somewhat somnolent, compared to Monday’s mad panic and chaotic rebound.

Monday, the S&&P 500 plunged from 4417.35 to 4222.62, then rallied and closed at 4410.13, modestly above Friday’s close of 4397.94. All in all, a good day, except for the panic part where the index lost 4.0%, before recouping all the losses.

Risk-off raged. The US dollar soared as did the Japanese yen and Swiss franc, while gold climbed, and US Treasury yields sank as traders fled to safe-havens. Alas, it was all for naught and those same traders are embracing risk-on, once again.

Except nothing has changed.

The FOMC meeting and risks for a hawkish outcome remain. Russian troops are camping at the Ukraine border, NATO ships and jets are flocking to Eastern Europe, missiles are flying around the Middle East, and North Korea’s resident nutcase is playing “silly buggers” with cruise missile testing.

Those fears were evident in Asia. Japan’s Nikkei 225, Hong Kong’s Hang Seng, and Australia’s ASX 200 suffered steep losses. European traders could not care less and bought stocks across the board.

The French CAC gained 1.0% and led the parade higher. S&P 500 futures rallied in Asia and early Europe but have given back most of the gains in NY trading and are down 1.5% as of 5:45 am PT.

EURUSD is trading with a negative bias and is at the bottom of its 1.1272-1.1328 range. FX traders may be acknowledging that a conflict over Ukraine will be another Cold War, literally and figuratively, as Russia has significant control over European energy supplies. The German IFO Survey was stronger than expected, with sentiment improving for the first time since June. ECB Chief Economist Philip Lane said there is less concern about Omicron now then in December. EURUSD technicals are bearish below 1.1330 with a break below 1.1260 targeting 1.1190.

GBPUSD is under pressure due to bearish technicals, negative risk sentiment, and ongoing UK political issues. A break below 1.3390 risks further losses to 1.3310.

USDJPY saw plenty of two-way action in a 113.68-114.15 range. Prices bounced off the Asia low and are trading the session high in NY due to a rebound in US 10-year Treasury yield to 1.78% from 1.716% yesterday.

AUDUSD rallied in early Asia, trading climbing from 0.7144 to 0.7175 consolidated in Europe then dropped to 0.7124 in NY S&P 500 futures fell. Australia CPI rose 3.5%, compared to a 3.2% y/y gain forecast. The reaction was muted as it was a National Holiday. Even so, the results fanned concerns about earlier than expected rate hikes.

Today’s data includes US Housing Price Index and Case-Shiller Home Price Index.

Chart of the Day: USDJPY hourly

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

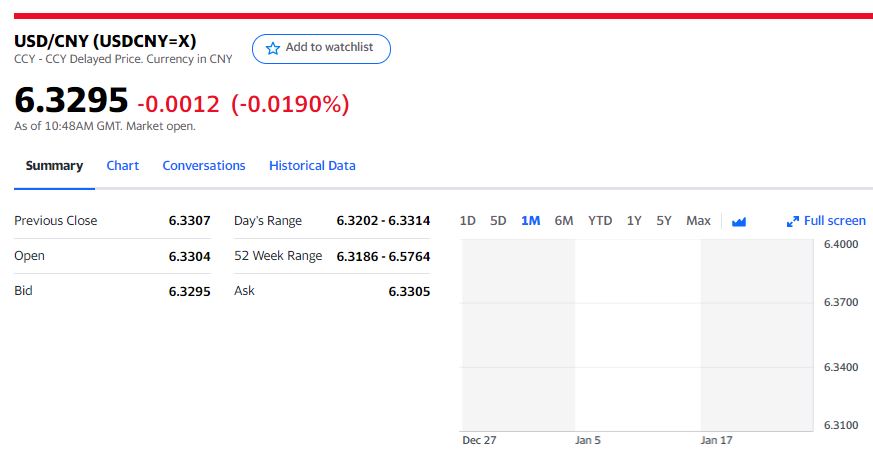

China Snapshot

Today’s Bank of China Fix 6.3418, previous 6.3411

Shanghai Shenzhen CSI 300 fell 2.26% to 4,678.45

China/US playing football with air passengers. US cancels 44 Chinese carriers in retaliation for China cancelling some US flights.

Chart: USDCNY 1 month

Source: Yahoo Finance