July 3, 2024

- Dovish sounding Powell improves risk sentiment

- Weekly jobless claims and ADP employment weaker than expected.

- US dollar trading defensively.

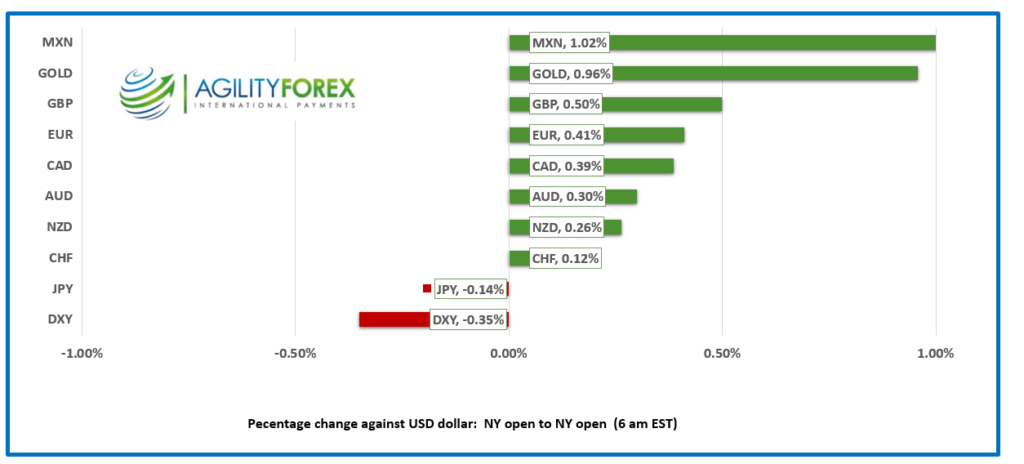

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3678, overnight range 1.3654-1.3756, previous close 1.3680

USDCAD dropped yesterday after Fed Chair Powell sounded cautiously optimistic about the direction of inflation, leading to speculation of an earlier-than-expected rate cut. USDCAD bears may find it difficult to gain traction due to the increased risk of trade sanctions with the US. The Canadian government imposed a 3% digital services tax aimed at many US tech giants. The US Computer and Communications Industry Association is asking the Biden administration to take action under the US-Mexico-Canada free trade agreement.

USDCAD dipped from 1.3670 pre-ADP and weekly jobless claims data to 1.3654 after both weaker than expected reports improve hopes for early Fed rate cut.

USDCAD downside will struggle around the 1.3660 area as a $879 million 1.3660 option strike expires at 10:00 am.

WTI oil is at the bottom of its 82.70-83.36 overnight range. The downside may be limited after the American Petroleum Institute reported a 9.16 million barrel drop in US crude inventories.

Canada’s May trade deficit widened to $1.93 billion from $1.32 billion. Analysts expected it to have narrowed to $1.2 billion.

USDCAD Technicals

The intraday technicals flipped again and turned negative after failing to move above resistance in the 1.3750 zone and the falling below support in the 1.3680-90 area. The drop sets up a test of the 1.3640-60 support area and then 1.3590.

The longer term technicals suggest that USDCAD sellers will find a number of hurdles beginning with support from the 100-day moving average at 1.3630, again in the 1.3590-1.3600 area and the from the 200-day moving average at 1.3590.

For today USDCAD support is at 1.3640 and 1.3610. Resistance is at 1.3710 and 1.3740. Today’s range is 1.3620-1.3700

Chart: USDCAD 4 hour

Source: DailyFX

Pre-Independence Day Data Dump and Early Close

ADP Employment rose 150,000 compared to the forecast for a 160,000 increase. The data was tainted by the upward revision to the previous months result of 157,000. Meanwhile weekly jobless claims increased by 5,000 to 238,000. The FOMC minutes are released this afternoon, but the impact from the deliberations has likely been diminished by Powell’s comments yesterday.

Powell is Cautiously Optimistic

Fed Chair Jerome Powell donned his optimist’s hat and said that recent inflation readings “suggest that we are getting back on the disinflationary path. We want to be more confident that inflation is moving sustainably down toward 2% before we start loosening policy.” Equity traders embraced the comments enthusiastically. Bond traders were less impressed and left the 10-year Treasury yield in the 4.255% area.

So Is Trump

The soon-to-be former felon and possibly the 47th President of the United States saw his odds of winning the November election soar to 67% after the Supreme Court ruling granted him immunity from prosecution. Some pundits worry that he could order Seal Team 6 to take out a rival. If so, it stands to reason that Biden could do the same thing.

What Goes Up, Keeps Going Up

The S&P 500 closed at 5509.01, the first close above 5500 ever and the 32nd record for the index in 2024. Bloomberg reported that more than $16 trillion has been added to the S&P 500’s value since October 2022. Asian equity traders were pleased. Australia’s ASX 200 rose 0.28% despite RBA rate hike concerns while Japan’s Topix rose 0.54%. European traders are no longer spooked by politics with the French CAC-40 index rising 1.36% and the UK FTSE 100 gaining 0.44%. S&P 500 futures traders are cautious ahead of today’s US data dump, and the index is down 0.13%.

EURUSD

EURUSD traded firmer in a 1.0736-1.0779 range. Eurozone Composite and Services PMI data were mixed. German results were a tick worse than expected (but still in expansion territory above 50) while Eurozone results were slightly better. Price action is limited ahead of round 2 of the French elections on July 7.

GBPUSD

GBPUSD climbed from 1.2674 to 1.2723 supported by steady Services PMI data and a dovish interpretation of Fed Chair Powell’s comments yesterday. S&P Global economist Joe Hayes wrote, “we’re on track for another quarter of GDP growth, according to Composite PMI data for the three months to June, albeit one that will be less punchy than the first quarter’s 0.7%.”

USDJPY

USDJPY rose from 161.39 to 161.99, a fresh 30-year peak, in another Buzz Lightyear (to infinity and beyond) moment. Steady US 10-year Treasury yields at 4.42% as wide Japan and G-10 interest rate differentials encourage yen sales.

AUDUSD and NZDUSD

AUDUSD is at the top of its 0.6665-0.6684 range, supported by solid May retail sales data which rose by 0.6% m/m compared to the forecast for a 0.2% gain. The data, combined with yesterday’s release of the RBA minutes, raised the odds for the RBA to hike rates this year to about 50/50.

NZDUSD traded in a 0.6069-0.6088 range supported by renewed US dollar weakness following Fed Chair Powell’s comments.

USDMXN

USDMXN retreated from 18.3060 to 18.2232 after Fed Chair Jerome Powell expressed “cautious optimism” about inflation performance in a speech yesterday. Prices saw some support after Trump’s election prospects improved following the Supreme Court ruling.

Bitcoin (BTCUSD)

BTCUSD is on the defensive again, falling from 63,177 to 59,686 with gains limited due to fears of around $9 billion in sales stemming from Mt. Gox bankruptcy distributions.

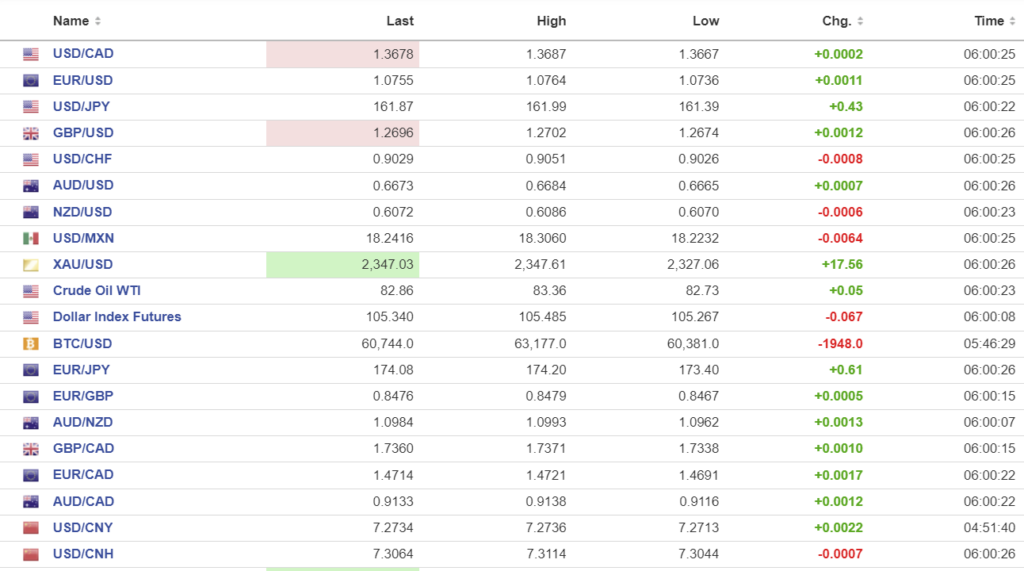

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1312 vs exp. 7.2633 (prev. 7.1291)

Sanghai Shenzhen CSI 300 fell 0.24% to 3463.41

Caixin June Services PMI 51.2 vs. Exp. 53.4 (Prev. 54.0), Composite PMI 52.8 (Prev. 54.1)

Chart: USDCNY and USDCNH

Source: Investing.com