March 4, 2024

- Opec and friends extend production cuts, as expected.

- Powell, BoC and ECB on tap this week.

- US dollar opens with minor losses except against JPY.

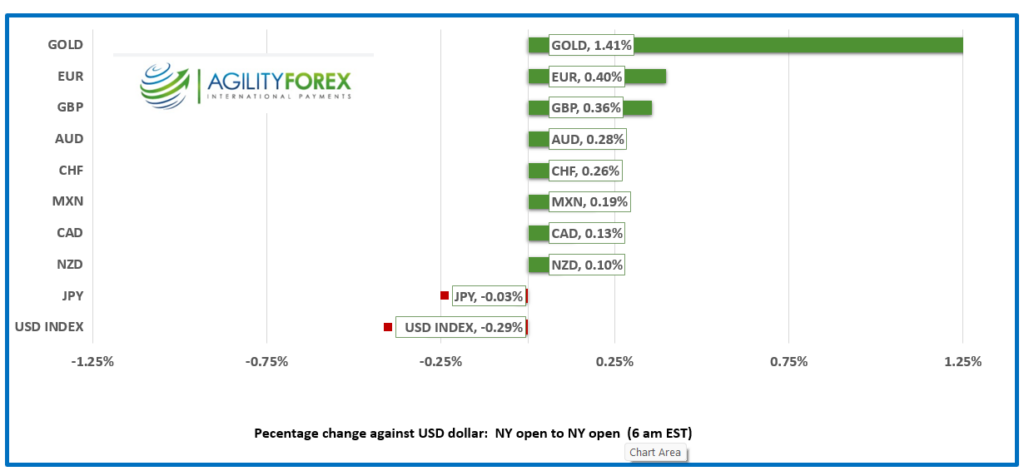

FX at a Glance

Source: IFXA/RP

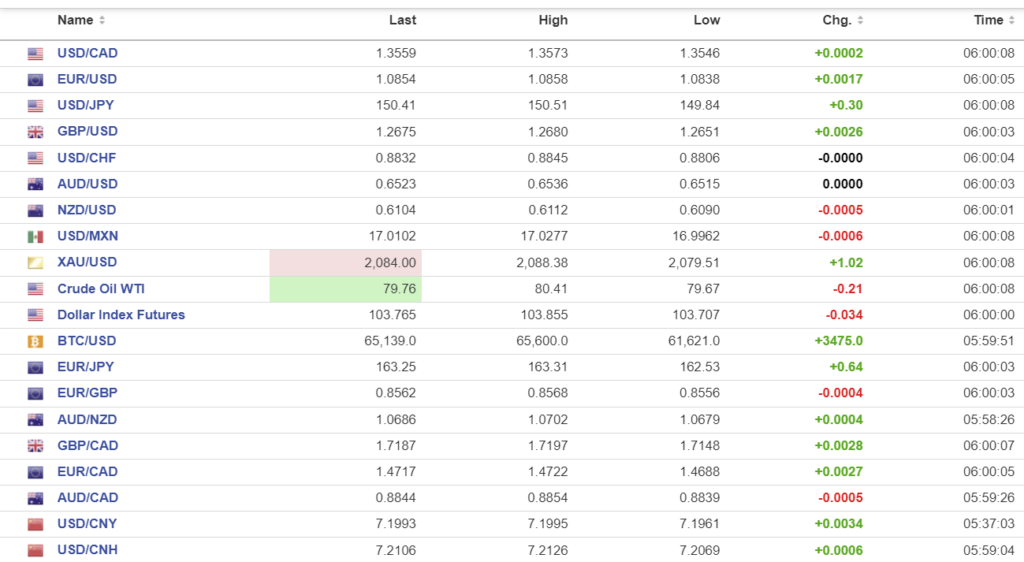

USDCAD Snapshot: open 1.3557-1.3561, overnight range 1.3546-1.3573, close 1.3564

USDCAD drifted lower in tandem with the other G-10 major currencies in a quiet overnight session. The currency pair may get some Canada-specific direction on March 6 when the Bank of Canada announces its monetary policy decision.

Don’t expect much. The BoC will push back against any near-term rate cut speculation by warning sticky inflation could lead to rate hikes. In any event, the BoC will be content to await guidance from the Fed meeting on March 20.

USDCAD saw some downward pressure after Opec announced it would extend oil production cuts of 2.2 million barrels/day into the second quarter even though the news was expected. WTI rose to $80.41/b before retreating to $79.44.

USDCAD Technicals

USDCAD failed to make any headway above 1.3600 last week but continues to trade with a bullish bias while prices are above 1.3490. The intraday technicals are bullish above 1.3540, looking for a move above 1.3610 to extend gains to 1.3630. A break below 1.3540 targets 1.3510.

The longer term technicals are unchanged with USDCAD a 1.3280-1.3660 range.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3620 and 1.3650. Today’s range is 1.3530-1.3610

Chart: USDCAD daily

Source: Daily FX

G-10 FX

It is a data- and event-filled week, but only Friday’s US nonfarm payrolls report will spark much volatility. Fed Chair Jerome Powell’s quarterly Congressional testimony starts Wednesday, and he will likely reiterate that it is not the right time to ease monetary policy. The ECB will also be downplaying chances of early rate cuts at Thursday’s meeting.

Asian equity indexes closed with small gains. Japan’s Nikkei 225 index cracked 40,000 for the first time and finished the day at 40,109.23. European bourses are modestly negative except for the UK FTSE 100 index, which is down 0.45%. S&P 500 futures are down 0.15%. The US 10-year Treasury yield is a touch higher at 4.211%.

EURUSD is rather uninspired as it drifts in a1.0838-1.0858 range ahead of Powell’s testimony on Wednesday and Thursday’s ECB meeting. This ECB meeting is expected to be a non-event with interest rates left unchanged.

GBPUSD is at the top of its 1.2651-1.2680 range. UK traders are awaiting Chancellor Jeremy Hunt’s budget (Wednesday) with a bit of trepidation, as the debacle of the Kwasi Kwarteng offering in 2022 is still fresh in their minds.

USDJPY chopped around in a 149.84-150.51 range and is near the top of that band in early NY. Downgraded risks for a BoJ rate hike and a near-term “unchanged” outlook for US rates are underpinning the currency.

AUDUSD continues to consolidate recent losses in a 0.6513-0.6536 range. Sentiment is bearish, with short AUD positions on the IMM near record levels and soft iron ore prices, which are at a 4-month low. Commonwealth Bank of Australia analysts are forecasting 150 bps of rate cuts by mid-2025. A mixed bag of Australian economic data barely moved the needle.

USDMXN is trading softer in a 16.9962-17.0277 range, with prices tracking broad-based US dollar sentiment. The currency pair faces domestic risks from the onset of the Presidential election campaign. The coalition led by former Mexico City mayor Claudia Sheinbaum and current President Obrador has a 20-point lead over challenger Galvez.

The US economic calendar is empty.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1020, expected 7.1906, previous 7.1059.

Shanghai Shenzhen CSI 300 rose 0.09% to 3540.87.

Chinese Premier Li Qiang will not hold a press briefing at the National Peoples Congress, the first time that has happened since 1993. Cynics suggest its because Xi Jinping’s ego cannot handle other politicians in the spotlight.

Chart: USDCNY and USDCNH daily

Source: Investing.com