Image by DALL-E

November 21, 2023

- No surprises from Canada October CPI

- Trading muted ahead of FOMC minutes this afternoon.

- US dollar opens mixed-to flat, consolidating earlier losses.

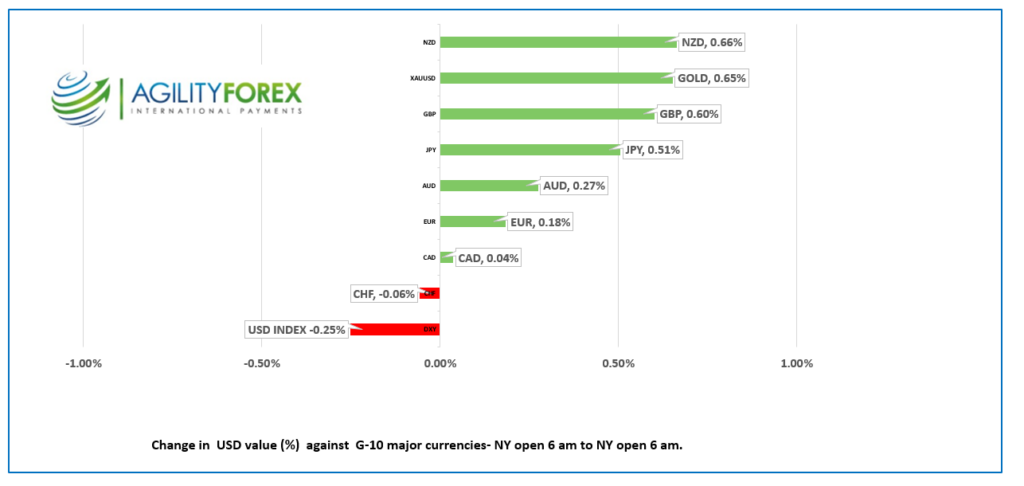

FX at a Glance

Source: IFXA/RP

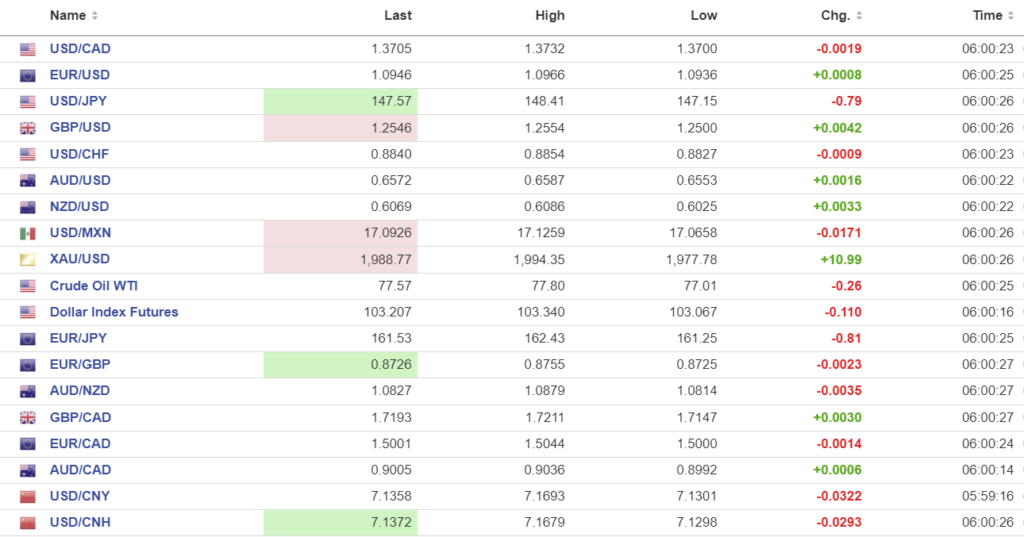

USDCAD Snapshot: open 1.3703-08, overnight range 1.3695-1.3732, close 1.3724

The October inflation report delivered too close to expectations to cause and furor. CPI rose 3.1% y/y (forecast 3.2%, September 3.8%). The decline was mostly due to falling gasoline prices which dropped 7.8% in the month. However, if you exclude gasoline, CPI was a sticky 3.5% y/y. Governor Macklem will not be thrilled to learn that prices for services rose at a faster pace in October which will may raise the risk of a rate hike on the December 6.

However, the reaction to the Canadian data is muted as traders look ahead to the FOMC minutes, hoping to find any clues to determine if policymakers were really as dovish as the market thinks.

Oil prices were directionless but held on to earlier gains. WTI traded in a $77.01/b – $77.80 range with traders sidelined until the FOMC minutes and a dose of caution ahead of this weekend’s OPEC meeting. The cartel is rumored to be planning a new wave of production cuts.”

USDCAD Technicals:

The USDCAD technicals are mixed. They are bearish below 1.3740 due to a weak one-week old downtrend line but bullish above 1.3660 from a two week old uptrend line. 1.3660 is also the 50 day moving average which may provide some additional support. A topside break will lead to a retest of the 1.3860 area while a downside break targets 1.3610 then 1.3570. Something has to give and today’s CPI number or FOMC minutes may be catalysts.

The uptrend line from the middle of July is intact while prices are below 1.3510.

For today, USDCAD support at 1.3670 and 1.3630. Resistance is at 1.3740 and 1.3780. Today’s range 1.3670-1.3770.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Traders are sitting on the sidelines awaiting thee release of the FOMC minutes at 11:00 am PT.

The narrative following the FOMC minutes will be interesting. The November 1 meeting introduced ‘financial conditions’ tightening into the mix, suggesting that high Treasury yields (the 10-year Treasury yield was in the 4.95-5.0% area) reduced the necessity for the Fed to hike rates. The question is – what does the Fed think now that rates are around 50 bps lower?

Traders were entertained and distracted by the OpenAI soap opera playing out in the headlines and newsfeeds. The OpenAI board’s decision to oust co-founder Sam Altman was met with outrage by over 700 employees of the company. They are demanding that the entire board resign, or else all 700 employees will quit. Vladimir Lenin may be popping out of his grave yelling, ‘Power to the Proletariat!'”

“Democracy is indispensable to socialism” Picture DALL-E

Asian equity indexes drifted aimlessly and closed not far from where they opened. European bourses are trading in a similar vein, except for the UK FTSE 100, which is down 0.62%. S&P 500 futures are down 0.12%, while the US 10-year Treasury yield slipped to 4.412%.

EURUSD is spinning its wheels in a narrow 1.0936-1.0966 band partly due to a lack of actionable EU data. The single currency is supported by hopes that US rates have seen the top which will lead to a broadly weaker US dollar.

GBPUSD is just above the middle of its overnight 1.2500-1.2554 trading range. Hawkish comments by BoE policymakers suggesting rates could rise further are underpinning prices. Governor Dave Ramsden said, “I would not rule out having to raise Bank Rate further.” His comments were supported by Governor Andrew Bailey who repeated an earlier comment, saying, it is “sensible to keep rates where they are.”

USDJPY is under pressure with prices falling to 147.15 from 148.41. Sentiment is bearish because of speculation that the Fed is done hiking rates while the Bank of Japan will soon be starting to raise rates.

AUDUSD drifted with a bullish bias in a 0.6553-0.6587 range supported by mildly improved risk sentiment. The minutes from the RBA November 6 meeting revealed that policymakers raised rates because businesses were passing on inflation costs to consumers.

NZDUSD is near the top of its 0.6025-0.6086 range. New Zealand’s trade deficit narrowed to -$1.70 million from -$3.42 million, but the results were higher than expected.

US October Existing Home Sales are expected to have declined to 3.9 million from 3.96 million in September.

FX high, low, open

Source: Investing.com

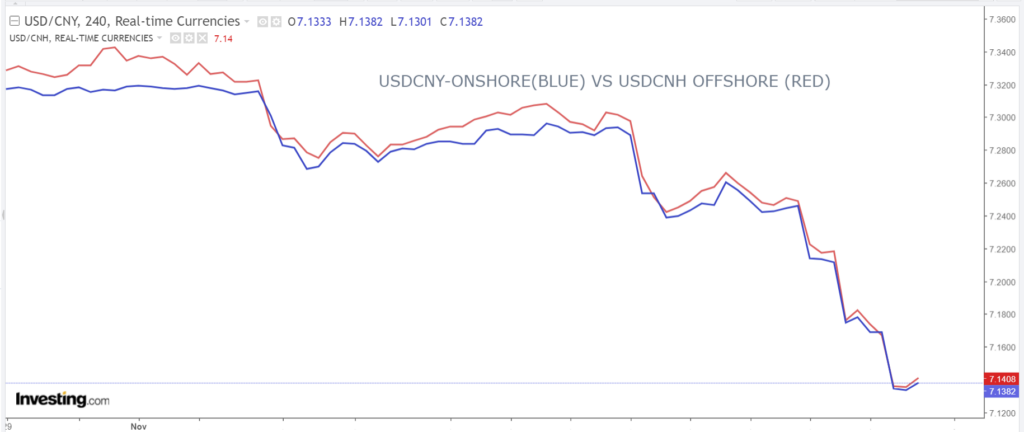

China Snapshot

PBoC fix: today 7.1406, expected 7.1677, previous 7.1612.

Shanghai Shenzhen CSI 300 rose 0.13% to 3581.07.

The yuan is rallying. The offshore USDCNH fell below the official fix rate for the first time since July, and forecaster are updating forecasts for USDCNY and USDCNY to reach 7.00 by year end. The USDCNY retreat is due to a modest improvement in US/China relations, talk that the greenback has peaked, and PBoC and a long USDCNH squeeze.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com