Photo: hdclipart.com

March 30, 2023

- US banking fears dissipate-inflation back on the agenda.

- US Q4 GDP and weekly jobless claims on tap

- US dollar opens mixed compared to Wednesday: drifted lower overnight.

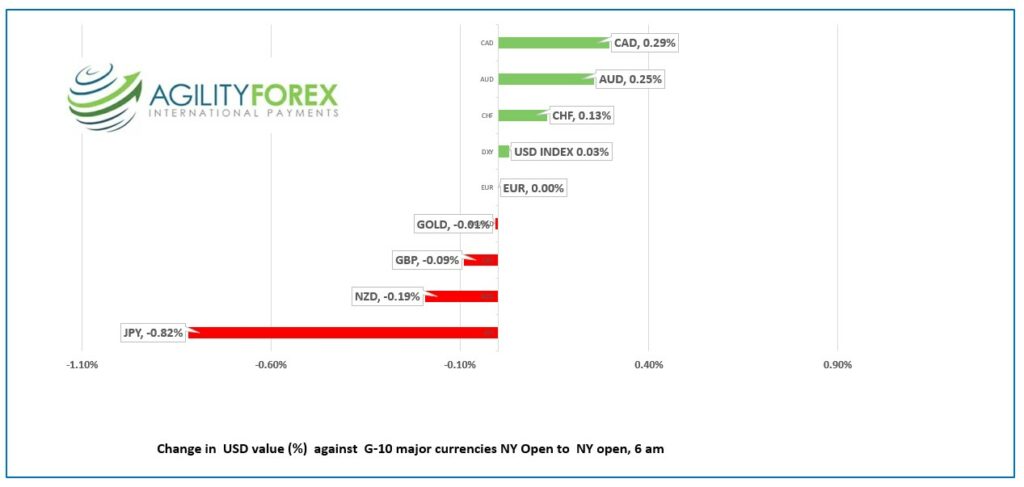

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3546-50, overnight range 1.3532-1.3580, close 1.3558

USDCAD is sinking under the weight of month and quarter-end rebalancing flows, firmer oil prices, improved global risk sentiment, and bearish short term technicals.

USDCAD is also being pressure by the unwinding of bullish bets following the failure to take out resistance at 1.3800 and the subsequent loss of support in the 1.3620-40 zone.

Bank of Canada deputy Governor Toni Gravelle’s speech yesterday didn’t offer any fresh insight into monetary policy.

The US dollar decline was aided by the recent oil price rally that has lifted WTI from $66.90 last Friday to $74.30 yesterday., after the EIA weekly oil report showed US inventories falling by 7.48 million barrels in the previous week. Prices have slipped from the peak and are at $73.60.

There are no Canadian economic reports today, leaving USDCAD direction determined by Wall Street.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while trading below 1.3590, looking for a break below 1.3510, which represents the 100-day moving averages as well as previous lows. A move below 1.3510 will extend losses to 1.3460.

Longer term, the uptrend line from mid-June comes into play at 1.3410.

For today, USDCAD support is at 1.3530 and 1.3510. Resistance is at 1.3590 and 1.3610.

Today’s range 1.3510-1. 3590

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders are trying to discern if the stock market rally and the drop in the US dollar are due to quarter and month-end position adjustments or because markets no longer fear banking risks or higher US rates.

The CME FedWatch tools suggests the risk that the Fed raises the Fed funds rate is a 44%, and the belief that the terminal rate has been reached or is very close, may be boosting Wall Street. On the other hand, the recent gains may just be the result of banking crisis safe-haven trades being unwound, exacerbated by quarter-end trading.

The Chinese government is rather upset that Taiwan President Tsai Ing-wen is in NY and ready to go apocalyptic if she meets with US House Speaker Kevin McCarthy. Taiwan is slowly losing official recognition from other countries in favour of money. G-20 nations are all for human rights, democracy, and respecting sovereignty, unless those views clash with economic benefits from dealing with a despotic regime.

Asia equity indexes closed higher except for those in Japan. Australia’s ASX 200 gained 1.02% while Japan’s Nikkei slipped 0.30%. European bourses opened positively and added to the gains with the French CAC 40 leading the pack higher. S&P 500 futures have gained 0.64% as of 5:50 am PDT.

The US 10-year Treasury yield is steady at 3.591%.

US weekly jobless claims rose by 7,000 to 198,000 (forecast 196,000) while Q4 GDP ticked down to 2.6% from 2.7% earlier.

EURUSD rose from 1.0825 to 1.0909, continuing the trend from the overnight session and getting a lift from hotter than expected German inflation. CPI rose 0.8% m/m (forecast 0.7%, and 7.8% y/y (forecast 7.5%). Economic Sentiment and Employment Expectations were marginally softer while consumer and services sentiment was largely unchanged. The EURUSD technicals are bullish above 1.0820 looking for a test of 1.1000.

GBPUSD rallied from its Asia low of 1.2295 to 1.2378 in NY, boosted by month and quarter end demand. Gains may be limited if analysts at Morgan Stanley are correct. They warn of GBPUSD downside risks if BoE rate hikes lag those of the ECB. Nevertheless, GBPUSD is in an uptrend above 1.2290, targeting 1.2420.

USDJPY climbed from 132.21 to 132.89 range due to the steady US 10-year Treasury yield and Japanese year end flows.

AUDUSD rose from 0.6663 to 0.6717 due to broad US dollar weakness. Across the Tasmanian Sea, NZDUSD traded in a 0.6205-0.6248 but slipped to 0.6230 in NY. NZ business confidence was unchanged in March at -43.

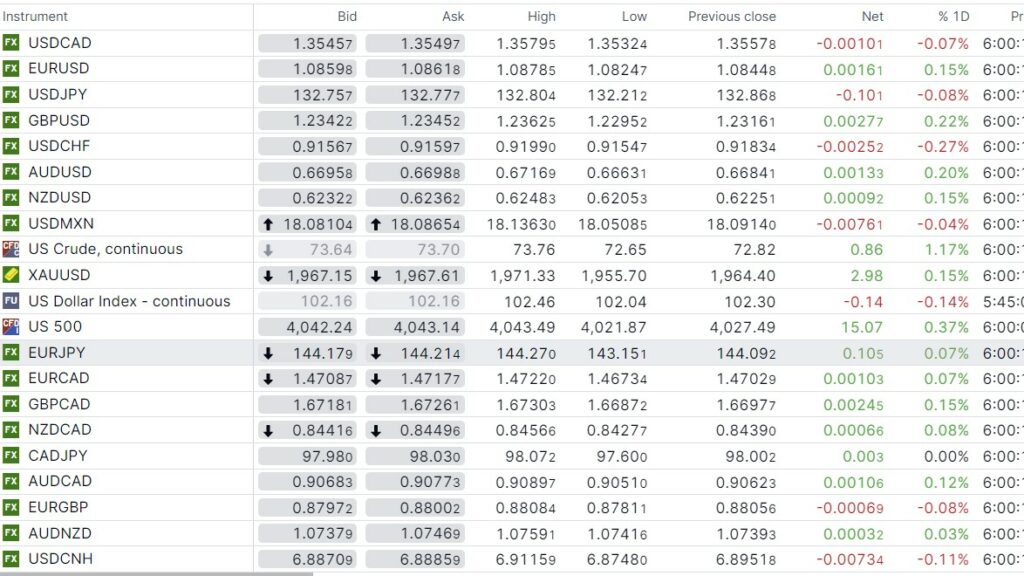

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

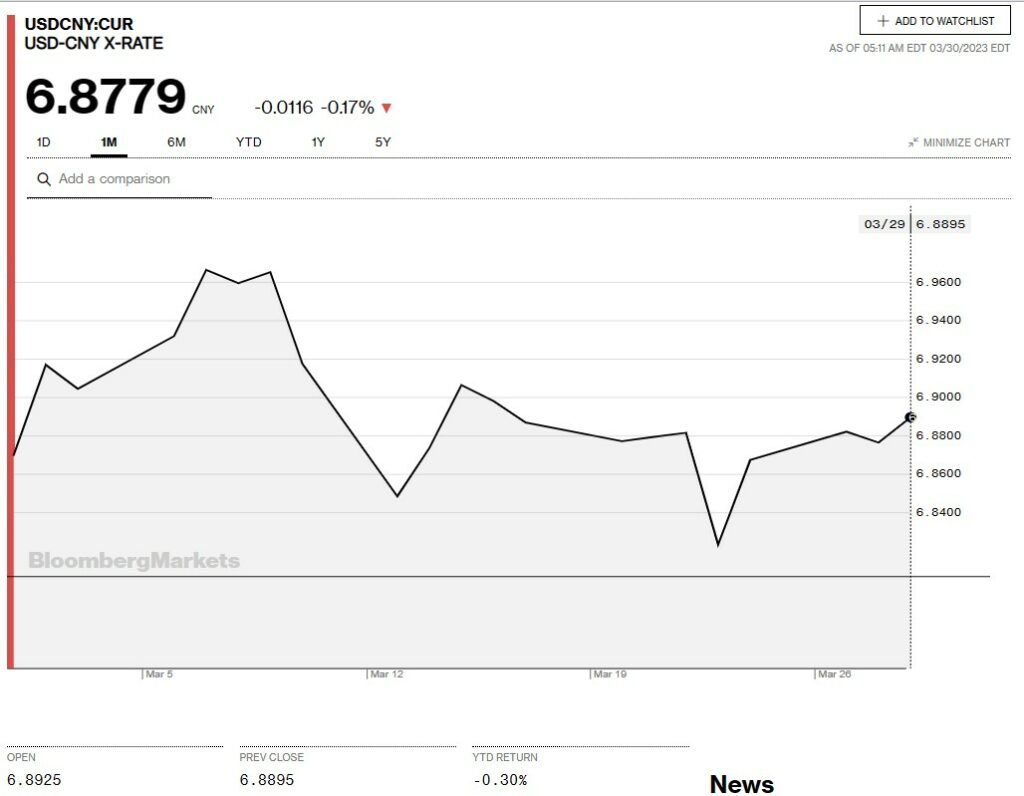

China Snapshot

Bank of China Fix: 6.8886, Previous: 6.8771

Shanghai Shenzhen CSI 300 rose 0.81% to 4038.53.

Chinese Premier Li Qiang told the audience at the Boao Forum that domestic economic situation is better than it was in January and February. He said the government will roll out new measures to improve market access and improve the business environment.

China and Brazil reached a deal to trade in their own currencies, scrapping the need for US dollars.

Chart: USDCNY 1 month

Source: Bloomberg