June 16, 2020

USDCAD Open (6:00 am) 1.3564-68, Overnight Range: 1.3514-1.3597

- US Retail Sales rise 17.7% in May (forecast 8.0%)

- IEA Oil Market Monthly outlook underpins crude prices.

- UK/EU say no more Brexit talks beyond December 2020

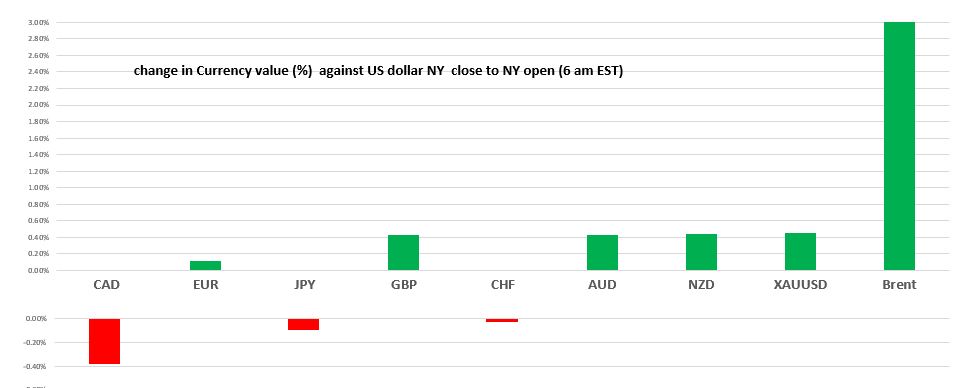

- US dollar opens lower vs G-10 majors, except vs CAD-JPY and CHF unchanged

Percent change in US dollar since Thursday’s NY open

Source: Saxo Bank/IFXA

FX Recap and outlook: The US dollar retreated against the majors except against EURUSD after the release of US May Retail Sales. The US Census Bureau said that despite the 17.7% increase from April, the results were still 6.1% below May 2019.

The Fed released details of its Corporate bond-buying program yesterday, and Wall Street turned a mini-meltdown in the opening hours into a rally. In addition, the US dollar safe-haven trades were abandoned, sinking the US dollar. Oil prices surged.

The positive risk sentiment washed over Asia and European equity markets overnight, and S&P futures are up over 1.3% (as of this writing).

The rally seems bogus.

The Fed announced it would buy Corporate bonds on March 23, so why get excited now? How does the Fed’s corporate bond buying program offset risks from a second wave COVID-19 outbreak? It was only a couple of days ago, that stock traders were stampeding for the exits on news that cases of coronavirus requiring hospitalization were rising in some US states.

Traders may be pinning their hopes on Fed Chair Jerome Powell’s quarterly testimony to Congress today. They may be hoping he delivers a less gloomy outlook than what the earlier FOMC statement suggested.

EURUSD’s rally stalled at resistance in the 1.1350 area, and prices drifted to the overnight low of 1.1315 in early NY trading. Profit-taking ahead of the US data and Powell’s testimony weighed on prices. ZEW Survey data improved for Germany and the Eurozone.

GBPUSD climbed from 1.2600 at yesterday’s NY close to 1.2687 in Asia before dropping down to 1.26507 in early European trading. The UK unemployment data was surprisingly unchanged at 3.9% for the three months to April 20. The total hours worked dropped 8.9% in the same three month period. GBPUSD rebounded from the lows, but when the UK and EU announced there would not be an extension of the Brexit transition period beyond December 2020, it thwarted the rally.

USDJPY is sitting at 107.30, just above the bottom of its overnight 107.24-107.63 range. The Bank of Japan left interest rates unchanged and made the usual noises about taking additional steps as needed. As always, the Japanese economy is expected to improve in the long run.

AUDUSD rode the rally wave with the minutes from the RBA meeting of June 2 giving the currency pair an added boost with its suggestion that the “worst was behind them”. NZDUSD tracked AUDUSD.

Oil prices got a lift after the International Energy Agency upgraded its forecast for 2020 oil demand due to stronger deliveries during the coronavirus period. They said the recovery was being driven by China’s exit from lockdowns, Opec compliance to cuts, and a decline in US, Canadian, and other non-Opec production.

USDCAD tracked broad US dollar sentiment and dropped to 1.3510 in Asia before rebounding to 1.3595 in Europe. The currency will continue to track broad US dollar sentiment and oil price moves.

USDCAD Technicals: The intraday USDCAD technicals are bearish below 1.3580, looking for a break below 1.3510 to extend losses to 1.3460. However, longer term, USDCAD is consolidating in a 1.3350-1.3890 range. The top represents the downtrend from mid-March, while the bottom is the uptrend from January. For today, USDCAD support is at 1.3520 and 1.3490. Resistance is at 1.3590 and 1.3640. Today’s Range 1.3470-1.3560

Chart: USDCAD daily

Source: Saxo Bank