Source: RCA/Columbia Pictures

- Risk sentiment improves even as Fed officials send mixed messages

- OECD warns of slower 2023 growth

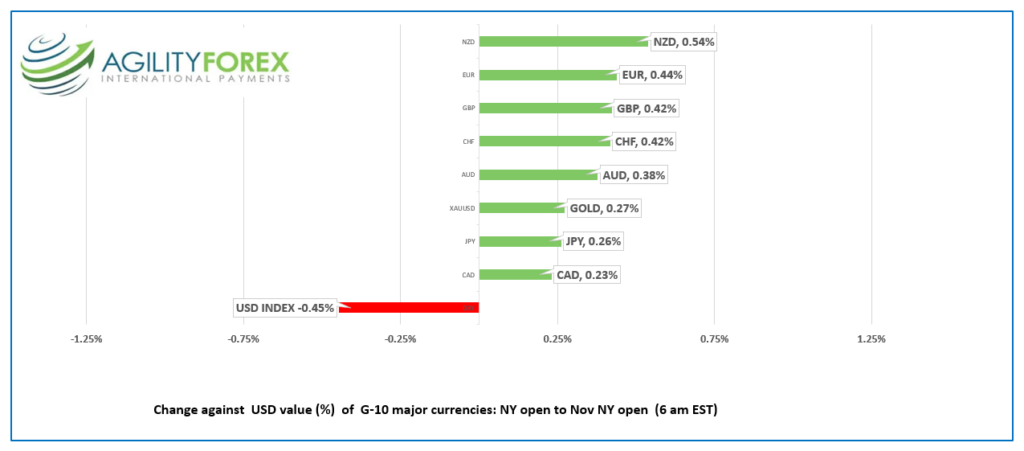

- US dollar retreats led by NZD gain

FX at a glance:

Source: IFXA Ltd/RP

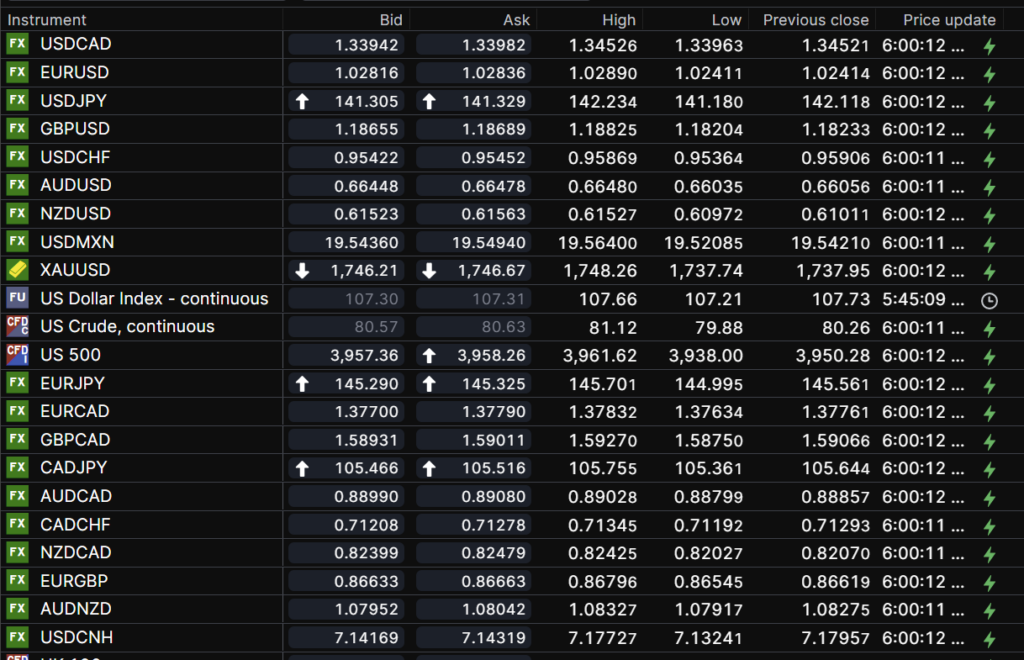

USDCAD Snapshot: open 1.3394-98, overnight range 1.3387-1.3453, close 1.3452

USDCAD is giving back all of yesterday’s gains in a Thanksgiving week, FIFA-thinned market. USDCAD direction is determined by broad US dollar sentiment and today that sentiment is bearish, albeit mildly. The reality it that this week’s moves are mostly noise ahead of tomorrows FOMC minutes. Even then, the US focus will be on how to cook a turkey and Black Friday Sales, not FX or equity markets.

WTI oil prices dropped to $75.35/barrel yesterday after the WSJ published a story claiming the Saudi’s and Opec were planning a production increase. Saudi officials denied the story and said Opec was sticking to its output cuts. WTI rallied to $81.23/b in NY today.

Canada Retail Sales fell 0.5% m/m in September, a touch better than the 0.7% dip that was expected but below the August increase of 0.5%. The drop was due to lower gas prices and USDCAD barely budged on the news. Ho-hum.

USDCAD Technical outlook

The USDCAD technicals are bearish inside the September-November 1.3250-1.3900 trading range. A move below support at 1.3360, suggests a retest of 1.3200, while a break above 1.3500 targets 1.3750.

For today, USDCAD support is at 1.3360 and 1.3310. Resistance is at 1.3430 and 1.3460

Today’s range 1.3360-1.3430

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The Karate Kid’s Mister Miyagi taught Daniel LaRusso a series of defensive blocks by making the kid wax his car. Fed officials are doing their own version of “wax on-wax-off.” Every day, policymakers contradict each other about the Fed’s interest rate outlook-risk on, risk off.

That leads to market churn as traders attempt to position for the longer term. The Fed “blackout period” (where policymakers cannot talk to the media) is usually about ten days prior to an FOMC meeting. Maybe it should be longer.

Monday was a risk off day mainly due to rising Covid cases in China that raised speculation of more supply chain disruptions and lower oil demand.

Today, risk sentiment flipped to mildly positive. Traders ignored another jump in new China covid cases and reacted to dovish Fed-speak from San Francisco Fed President Mary Daley, and Cleveland Fed President Loretta Mester.

Trading volumes are also diminished as the FIFA World Cup kicks into high gear with four games on the slate today.

The Organisation for Economic Cooperation and Development (OECD) warned that the global economy is expected to slow further, blaming the oil shock from Russia’s war of aggression for the slowdown.

OECD Secretary-General Mathias Cormann said, “The global economy is facing serious headwinds. We are dealing with a major energy crisis and risks continue to be titled to the downside with lower global growth, high inflation, weak confidence, and high levels of uncertainty making successful navigation of the economy out of this crisis and back toward a sustainable recovery very challenging. An end to the war and a just peace for Ukraine would be the most impactful way to improve the global economic outlook right now. Until this happens, it is important that governments deploy both short- and medium-term policy measures to confront the crisis, to cushion its impact in the short term while building the foundations for a stronger and sustainable recovery.

Asia equity markets closed higher led by a 0.61% rise in Japan’s Nikkei 225 index and a 0.59% gain in Australia’s ASX 200. European bourses are all in the green. The UK FTSE 100 is up 0.66% and the German Dax has gained 0.29% in a low volume session. S&P 500 futures are just above unchanged, posting a 0.07% increase.

WTI oil rose 1.3% and gold climbed 0.55%, helped by the weaker US dollar. The US 10-year Treasury yield eased from 3.844% at yesterdays close to 3.795% today.

EURUSD traded in a 1.0241-1.0290 range supported by broad US dollar weakness. ECB policymakers are following the Feds lead with some officials suggesting a need for smaller rate hikes, while others insist a 75 bp bump is required to lower inflation. Meanwhile, the intraday EURSD technicals are bullish above 1.0240. The OECD forecasts Euro area growth at 0.5% in 2023.

GBPUSD ticked higher in a 1.1820-1.1883 band due to the modestly better risk tone. Traders ignored the OECD forecast forecasting the UK to be the weakest G7 country in 2023, blaming high inflation and worker shortages for the slump. The OECD predicts the UK economy will shrink by 0.4% in 2023.

USDJPY has given back almost half of yesterday’s gains and traded with a negative bias in a 141.09-142.23 range. The drop was mainly due to broad US dollar weakness and exacerbated by the slide in the US 10-year Treasury yield.

AUDUSD rose from 0.6604 to 0.6648 underpinned by data showing Consumer Confidence rose 1% from the previous week. RBA Governor Philip Lowe said, “supply shocks, climate change, aging workforces and the retreat of globalization will increasingly fuel inflation volatility worldwide.”

NZDUSD rallied from 0.6097 to 0.6153 ahead of an expected 75 bp RBNZ rate hike, tomorrow.

There are no top tier US economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

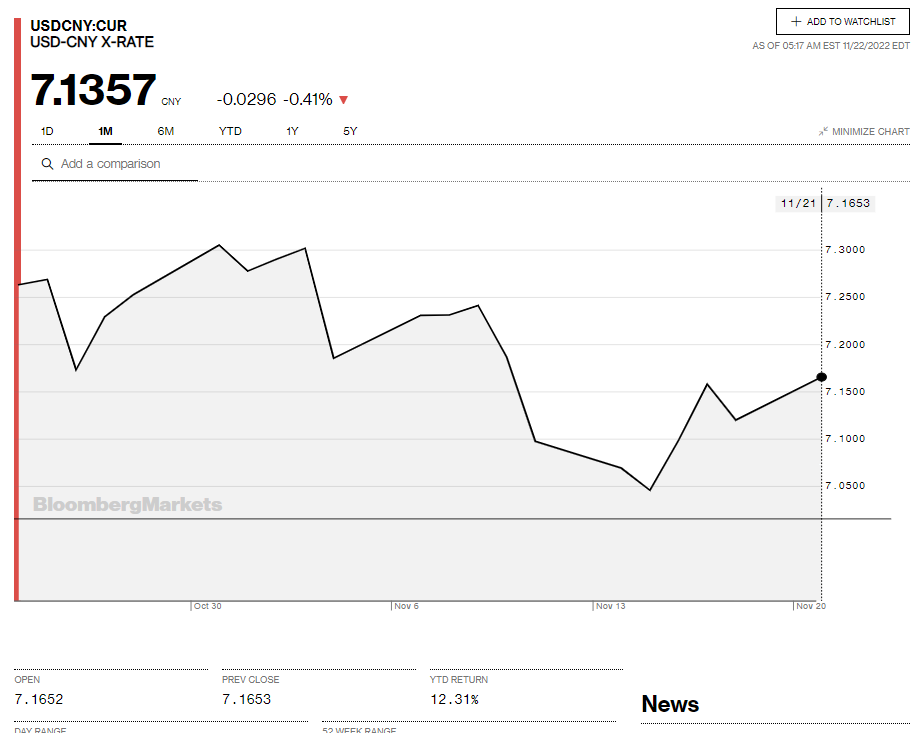

China Snapshot

Today’s Bank of China Fix: 7.1667, previous 7.1256

Shanghai Shenzhen CSI 300 rose 0.01% to 3769.57

China reports 28,127 new Covid cases on Monday. Beijing shutters museums, shopping centers, and parks

Chart: USDCNY 1 month

Source: Bloomberg