April 18, 2024

- Global risk sentiment improves modestly.

- Fed-speak. Quarterly earnings and Jobless claims data on tap.

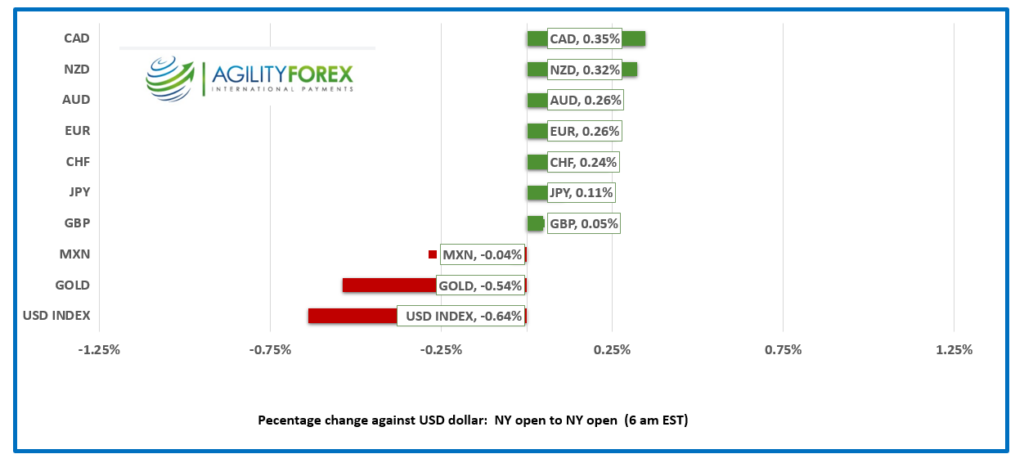

- US dollar opens with losses across the board.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3759, overnight range 1.3742-1.3780, close 1.3775.

The USDCAD rally ran out of gas, and it didn’t have anything to do with the huger 12-17 cents per litre jump in the price of fuel across Canada. No, USDCAD fell because of broad-based US dollar selling largely due to profit-taking and because Fed Chair Powell hadn’t really said anything different. The lack of escalation following Iran’s bungled attack on Israel led to the unwinding of safe-haven trades.

Peel Regional Police have solved the mystery of last year’s $22.5 million gold heist from Pearson Airport. They know who did it, the how they did it, but they don’t know where the gold is. Some people think that the Canadian Air Transport Security Authority (CATSA) should have led the investigation. You can’t get a 2 ounce bottle of shampoo past them, so the odds of sneaking around 300 kilograms of gold out the door would be slim.

WTI oil traded lower, falling from 82.94 to 81.58, mainly because geopolitical tensions eased somewhat and because the energy Information Administration reported a 2.7 million barrel increase in crude inventories.

There is a $1.0 billion USDCAD option expiring today with a strike of 1.3750 which suggests a price action could get choppy on the approach to 10:00 am.

There is no Canadian data

USDCAD Technicals

The intraday USDCAD technical are bearish below 1.3805 and looking for a test of the 1.3740 area. A break above 1.3805 targets 1.3850.

The USDCAD uptrend that began with the break above 1.3640 is intact while prices are above 1.3730 (4 hr chart). Failure to break below this levels suggests a rest of resistance in the 1.3850-60 area. A break below 1.3640 suggests further losses to 1.3500.

For today, USDCAD support is at 1.3740 and 1.3710. Resistance is at 1.3805 and 1.3850. Today’s range is 1.3730-1.3790.

Chart: USDCAD daily

Source: DailyFX

There’s a kind of a hush all over the world.

A sense of calm has descended across global markets following the recent drama around the Fed and Middle East. The risks remain, but the lack of any fresh catalysts is allowing traders to shift their focus to US quarterly earnings reports.

Mundane G-7 Statement

The G7 noted the global economy’s resilience against multiple shocks, noting that although growth remains subdued, inflation pressures have moderated due to easing commodity prices and ongoing tight monetary policies. The group reaffirmed their commitment to price and financial stability as foundations for sustainable growth while acknowledging significant geopolitical risks. So, nothing new.

EURUSD

EURUSD bounced in a narrow 1.0664-1.0690 range. Prices were supported by improved risk sentiment, but comments by ECB President Christine Lagarde suggesting that the first ECB rate cut would occur in June capped gains. ECB policymaker Bostjan Vasle reminded markets that the ECB cannot fully disregard inflation dynamics in the US.

GBPUSD

GBPUSD inched a tad higher, trading in a 1.2448-1.2485 range, but gains were limited due to dovish comments from Bank of England officials Governor Bailey. Yesterday Mr. Bailey said, “In the UK we’re disinflating at what I call full employment. I see, you know, strong evidence now that that process is working its way through.” BoE policymaker Megan Greene also offered positive comments about inflation. Analysts suggested that those comments meant that the BoE would be cutting rates soon.

USDJPY

USDJPY dropped to 153.96 in the early going on heightened fears of FX intervention. However, the BoJ was nowhere to be seen, and prices climbed to 154.48 in NY. A BoJ official reiterated the need to maintain an ultra-easy monetary policy as it would take a long time for trend inflation to rise to 2.0%. There is a lot of speculation of coordinated FX intervention by the BoJ, the Bank of Korea, and the PboC due to officials expressing serious concerns about the sharp deterioration of their currencies.

AUDUSD and NZDUSD

AUDUSD traded firmer, rising from 0.6430 to 0.6457, but gains were capped after a weak employment report. Australia lost 6,600 jobs in March compared to the 7,200 gain that was expected, and the unemployment rate rose to 3.8% from 3.7%.

NZDUSD rose to 0.5933 from 0.5906 on the back of improved risk sentiment fueling US dollar sales.

USDMXN

USDMXN hung on to recent gains and traded sideways in a 16.9207-16.9990 range. The gains were due to broad US dollar demand after Powell reiterated that he was in no hurry to cut interest rates and from safe-haven demand for US dollars because of Middle East tensions.

Weekly jobless claims were 212,000 basically unchanged from the previous week while the Philadelphia Fed Manufacturing Survey was 15.5 (3.2 previously)

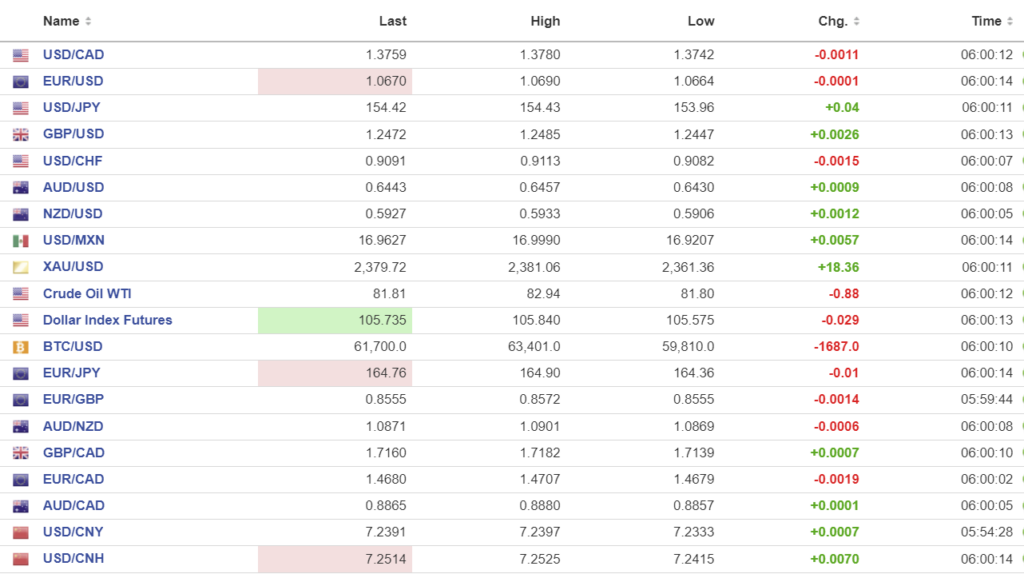

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1020 vs exp. 7.2281 (prev. 7.1025).

Shanghai Shenzhen CSI 300 rose 0.12% to 3569.80.

China is cooking its books. Bloomberg writes that the PboC urban depositor survey the economic growth of 5.3% doesn’t reflect the reality on the ground. The CSI 2000 index (small cap companies) are very vulnerable to business cycles and it is down 20% YTD,

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com