Picture: Wikipedia/IFXA Ltd

Equities rebound, SPX recoups yesterday’s losses

Second-tier data, and pending FOMC meeting suggest FX consolidation

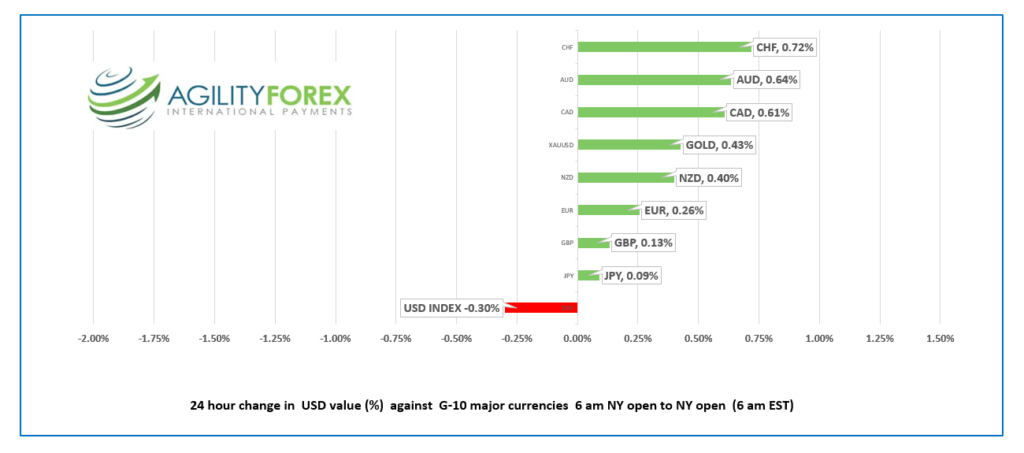

US dollar erases Monday’s gains, opens with losses across the board

FX at a Glance:

Source: IFXA/RP

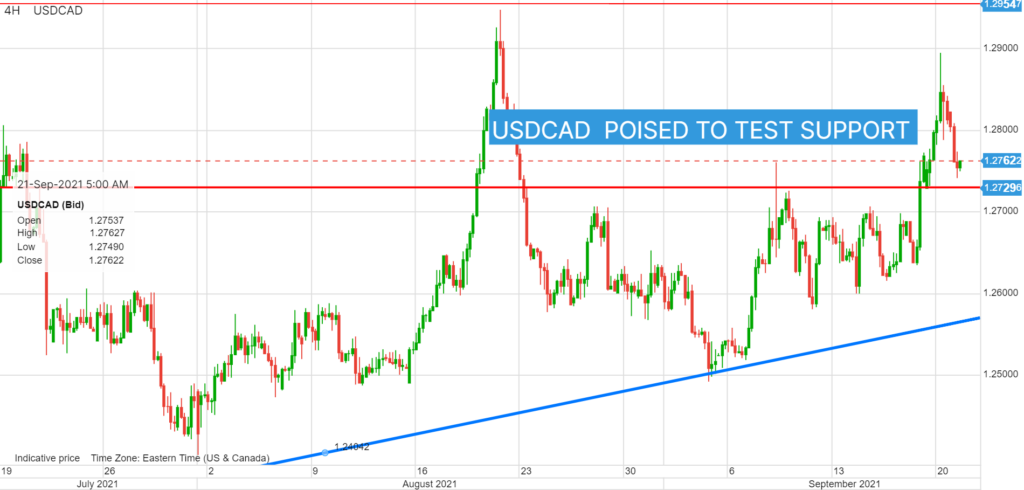

USDCAD Snapshot Open 1.2752-56, Overnight Range 1.2745-1.2823, Previous close 1.2820

Canada went to the polls and after a 36 day, $660 million election campaign and nothing changed. It’s a good thing that for Liberal’s “money is no object.” The 44th parliament is almost identical to the 43rd parliament. Mr Trudeau failed to secure a coveted “majority” and lost the popular vote for the second time in a row. 34.02% of Canadian preferred a Conservative government while only 32.9% wanted the Liberals.

USDCAD traders ignored the election and tracked external developments. Yesterday’s China Evergrande Group fueled equity meltdown drove USDCAD from 1.2762 to 1.2894 by 8:40 am ET yesterday. Prices slid steadily throughout the rest of the session and continued to retreat overnight.

The currency pair derived a little support from crude oil prices. USDCAD price action mirrored WTI oil moves. Monday, Goldman Sachs analyst raised their Q4 oil price forecast to $85.00/b from $80.00/b, due to expected higher demand.

USDCAD is expected to consolidate recent moves due to a lack of top-tier economic data from Canada and the US today, and due to caution ahead of tomorrows FOMC meeting.

Technical view: The intraday USDCAD technicals are bearish below 1.2780, looking for a break of support at 1.2730 to extend losses to 1.2660, the uptrend line from June 15. If broken, it negates the uptrend and shifts the focus to 1. 2500. A move above 1.2780, targets 1.2850

For today, support is at 1.2730 and 1.2680. Resistance is 1.2780 and 1.2830. Today’s range 1.2730-1.2780

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Yesterday’s market angst is today’s confidence. Fears that China’s Evergrande Group would collapse and lead to markets collapsing across Europe and the US have given way to hopes Chinese authorities will find a way to bail out the troubled company.

Hong Kong’s Hang Seng index climbed 0.51%, and the Australian ASX 200 gained 0.35%, while Japan’s Nikkei dropped 2.16%. European bourses are higher, led by a 1.27% gain in the German Dax. S&P and DJIA futures are pointing to a positive open on Wall Street. WTI oil rose 1.07%, while gold gained 0.21%. US 10-year Treasury yields have reclaimed the 1.335% level.

The Organisation for Economic Development and Cooperation (OECD) released an interim report. The report says, “Economic growth has picked up this year, helped by strong policy support, the deployment of effective vaccines, and the resumption of many economic activities.” However, it is too soon to withdraw stimulus. “A premature and abrupt withdrawal of policy support should be avoided whilst the near-term outlook is still uncertain”

EURUSD is rangebound in a 1.1719-1.1739 band due to caution ahead of Wednesday’s FOMC meeting. Analysts do not expect the Fed to announce tapering, which is one of the reasons why support in the 1.1700 area is holding. ECB policymaker Luis de Guindos suggested that inflation increases are temporary, and there is no need for the ECB to act. Sweden’s Riksbank left rates unchanged but increased its inflation forecast to 2.0% from 1.6% for 2021.

GBPUSD climbed from 1.3650 to 1.3692, but it is a countertrend bounce while prices are below 1.3730. Prices got a bit of support from better than expected CBI Industrial Trends data.

USDJPY remains depressed.

Prices dropped from 110.02 to 109.32 yesterday but only managed to bounce to 109.70 today. Steady US Treasury yields underpin USDJPY, but gains are capped by safe-haven demand for yen.

AUDUSD and NZDUSD rallied due to the improvement in global risk sentiment. The RBA minutes from the September 7 meeting did not provide any fresh insight. Australian interest rates are not expected to rise until 2024. The intraday AUDUSD technicals are bullish above 0.7250, looking for a break above 0.7290 to extend gains to 0.7350.

US Building Permits, Housing Starts, and Current Account reports are due, along with the Canada New Housing Price Index.

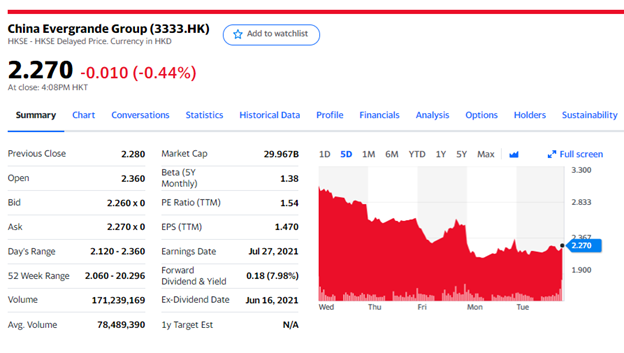

Chart of the Day- China Evergrande Group (3333.HK)

Chart: Yahoo Finance

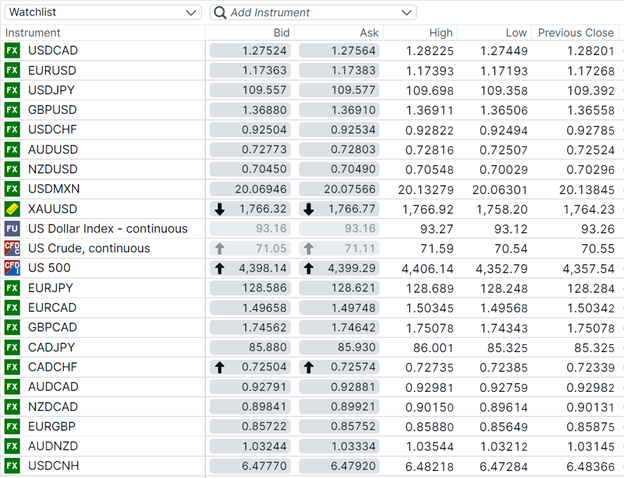

FX open, high, low, previous close

Source: Saxo Bank

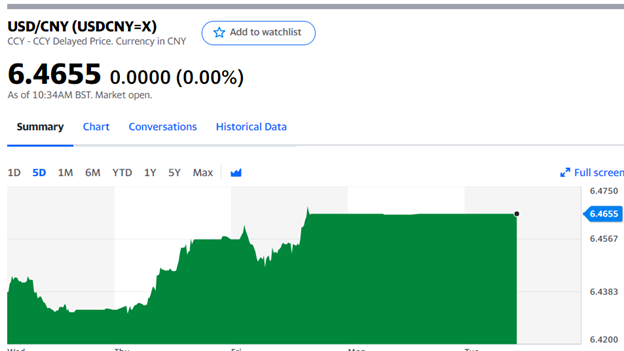

China Snapshot -Closed

Today’s Bank of China Fix, 6.4527, Previous 6.4527

Shanghai Shenzhen CSI 300 closed

Evergrande Chairman says he is confident the company will fulfil obligations to buyers. Jury is still out on Chinese government bailout.

B of A lowers 2021 growth to 8.0% from 8.3% and 2022 growth to 5.3% from 6.2%.

Chart: USDCNY 5 day

Source: Yahoo Finance