March 19, 2024

- Markets becalmed ahead of FOMC.

- BoC minutes from March 6 meeting on tap today.

- US dollar opens mixed-JPY sinks.

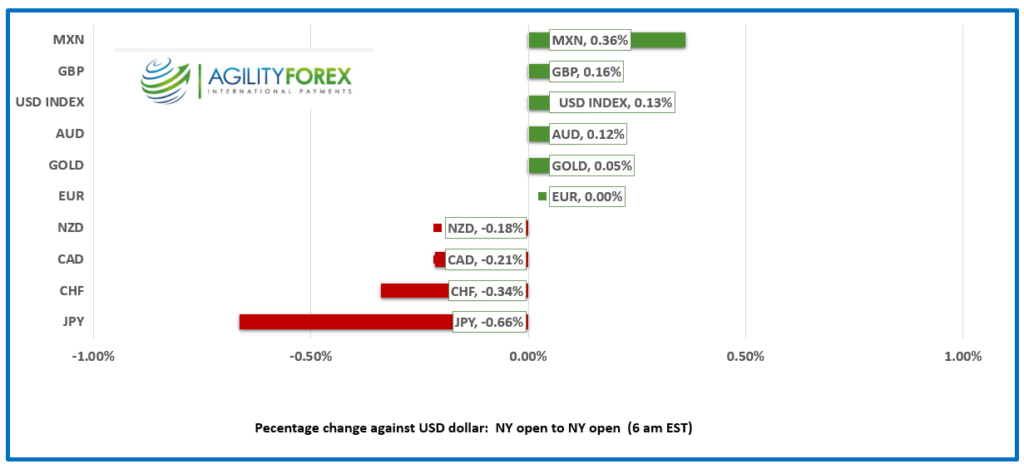

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3602-06, overnight range 1.3561-1.3606, close 1.3566

USDCAD bounced between 1.3560 and 1.3610 yesterday ang again overnight. Yesterday, lower than expected inflation data sparked a short term rally from 1.3567 to 1.3614 but that move was fully reversed before lunch. Position adjusting ahead of today’s FOMC meeting and speculation that the number of rate cuts projected in December would be lowered in todays Summary of Projections.

The BOC Summary of Deliberations from its March 6 meeting will be released today but they will not have much impact on FX markets as the FOMC meeting is the only game in town.

WTI oil prices are comfortably above $80.00/b. They traded in an $81.66-$82.66/b range and opened at the low. Traders are expecting a small increase in US crude inventories when the EIA reports its weekly statistics.

USDCAD Technicals

Thee intraday USDCAD technicals are bullish above 1.3570 supported by the failure to break below 1.3560 yesterday and again overnight.

USDCAD is trading with a bullish bias while prices are above 1.3470 (daily chart) and looking for a decisive breach of resistance in the 1.3620 area. That level has rejected probes on multiple occasions since November 28.

A topside break targets 1.3850 but prices will need a few days of above 1.3620 trading for confirmation. If that happens, the 1.3590-1.3620 area will become support. Failure to sustain the gains would be a false break and USDCAD would revert to its well-defined 1.3360-1.3620 trading range.

For today, USDCAD support is at 1.3570 and 1.3530. Resistance is at 1.3620 and 1.3660. Today’s range is 1.3560-1.3650.

Chart: USDCAD daily

Source: Investing.com

G-10 FX

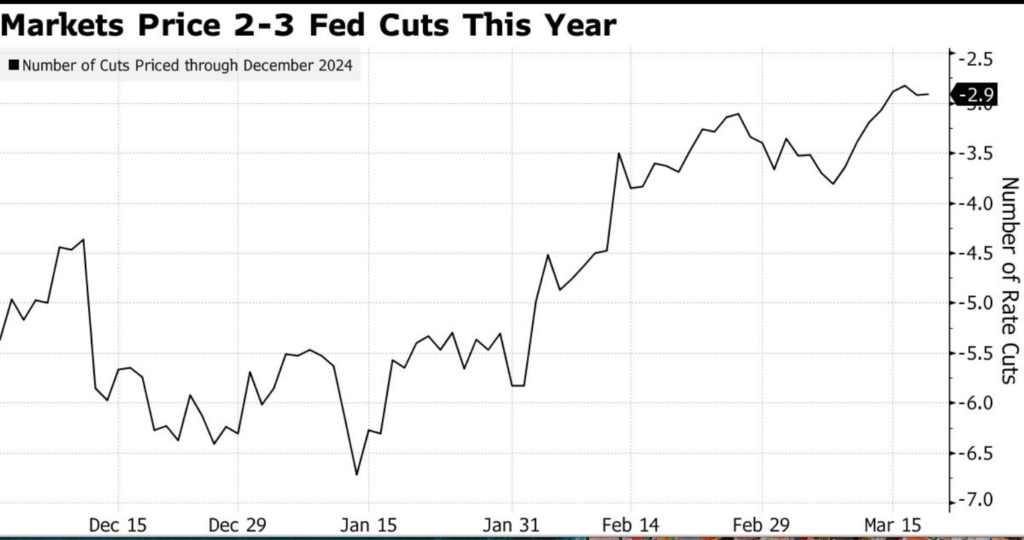

Traders are seeing spots…well more accurately dots. The FOMC quarterly Summary of Economic Projections (SEP) is expected to reflect fewer rate cuts than anticipated for 2024. That will merely confirm market pricing which has gone from expecting 7 rate reductions to just 2 or 3.

Source: Bloomberg

EURUSD traded in the same 1.0836-1.0873 range as yesterday, with prices weighed down by broad US dollar strength, ahead of an expected hawkish FOMC monetary policy statement. ECB President Christine Lagarde didn’t help when she gave a wishy-washy comment about June rate cut speculation. She said, “Our decisions will have to remain data-dependent and meeting-by-meeting, responding to new information as it comes in.” This implies that, even after the first rate cut, we cannot pre-commit to a particular rate path.”

GBPUSD chopped in a 1.2687-1.2730 range. Prices dropped from the peak after inflation data was lower than expected. CPI rose 3.4% year-over-year (forecast 3.6%, January 4.0%). The Bank of England policy meeting is tomorrow, and their focus is on Services inflation. That number is still a sticky 6.1% year-over-year. ING economists suggest that the volatility of the data will delay any rate cuts until June at the earliest.

USDJPY soared, rising from 150.77 to 151.79 just before NY opened as short USDJPY traders continue to get squeezed. Liquidity was poor as Japan was closed for the Vernal Equinox holiday. The BoJ decision to end negative rates after 17 years did not result in a steep drop in USDJPY as was widely expected because a) a short-term rate at 0.1% is negligible and b) because the Fed is not expected to cut interest rates until late in 2024. That still leaves a hefty interest rate differential in favor of US dollars.

AUDUSD traded in a 0.6511-0.6542 range and is just above the low in early NY trading. The currency is getting a bit of a benefit after the RBA left rates unchanged at 4.35% yesterday and is not expected to start easing until November. Australian employment data is due tomorrow.

NZDUSD traded narrowly in a 0.6025-0.6056 range. Traders are focused on this afternoon’s Fed meeting and ignored the latest IMF update. The IMF warned that the RBNZ needs to keep interest rates at elevated levels (currently 5.50%) even as the economy grows at 1.1%.

USDMXN traded firmer, rising from 16.7779 to 16.8495, due to US dollar strength stemming from expectations of a hawkish outcome from today’s FOMC meeting. Traders are also looking ahead to January Retail Sales (forecast 0.4% month-over-month, previous -0.9%) and the Banxico monetary policy meeting on Thursday.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0968 vs exp. 7.1967 (prev. 7.0985)

Shanghai Shenzhen CSI 300 rose 0.22% to 3585.38.

The US is considering more sanctions on companies linked to Huawei Technology’s after Huawei unveiled an advanced microchip. In addition, the Biden administration award Intel up to $8.5 billion in CHIPS Act grants. The news is certainly to inflame US/China trade tensions.

Chart: USDCNY and USDCNH daily

Source: Investing.com