Photo: HPclipart.com

June 7, 2023

- OECD forecasts global growth at 2.7% in 2023, (2.6% y/y in March)

- BoC decision ahead

- US dollar drifts lower awaiting fresh catalyst.

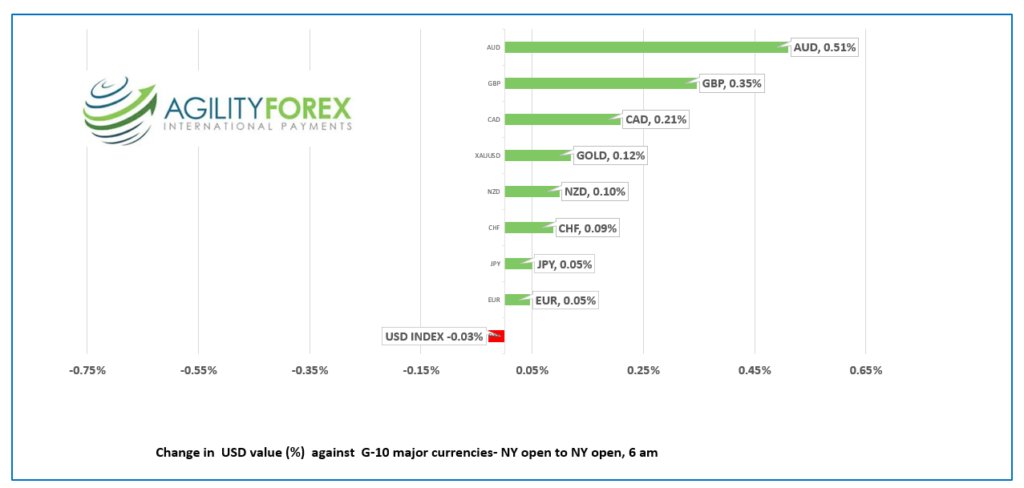

FX at a glance

Source: IFXA Ltd/RUSDCAD Snapshot: open 1.3389-93, overnight range 1.3377-1.3425, close 1.3402.

It’s BoC decision day and it is not just wildfire smoke clouding the outlook. The market is convinced that policymakers plan to raise rates by 25 bps. They just aren’t sure if it will happen today or on July 12.

Those expecting a hike point to the latest robust economic reports and yesterday’s RBA rate hike as justification for a move today. The others believe that because Governor Tiff Macklem announced a pause, the onus is on him to justify a rate increase and he isn’t having a press conference today. Tiff needs the Rush. “Living in the limelight, the universal dream.”

WTI oil prices are sloshing around in a $71.04-$72.49/b range. Prices are supported by Saudi Arabia’s decision to cut production by 1.0 mb/d but weighed down by the latest OECD forecast, predicting tepid global growth.

Canada’s trade surplus widened to 1.94 billion in April.

USDCAD Technical Outlook

The intraday USDCAD technicals in a short-term downtrend channel between 1.3350 and 1.3430. A break below 1.3350 targets 1.3290 then 1.3220, last seen in November 2022. A move above 1.3430 suggests a retest of 1.3560.

Longer term, USDCAD is supported at 1.3300 and has resistance at 1.3600.

For today, USDCAD support is at 1.3350 and 1.3300. Resistance is at 1.3430 and 1.3360.

Today’s range 1.3330-1.3430.

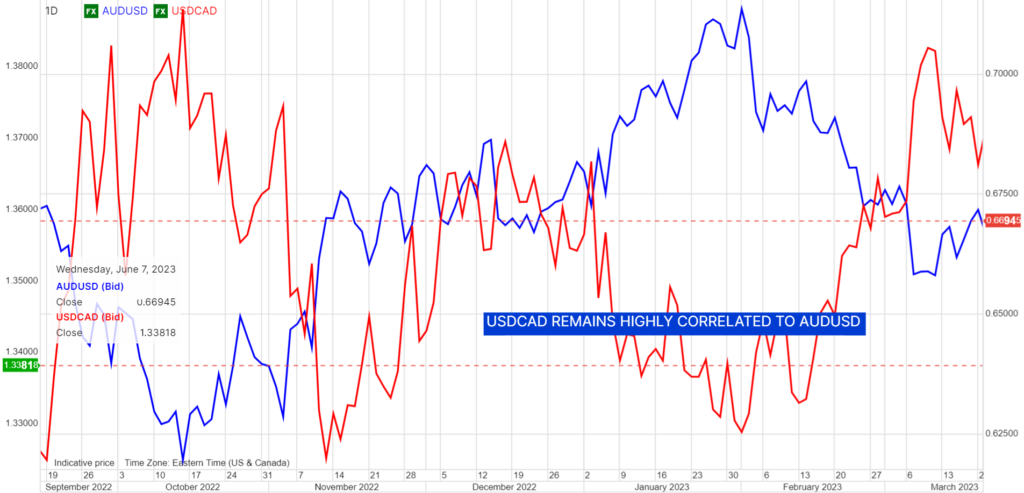

Chart: USDCAD and AUDUSD daily

Source: Saxo Bank

G-10 FX recap and outlook

Weaker than expected Chinese trade data dampened the post-pandemic global growth story in Asia, before the quarterly OECD report piled on.

The report said “The global economy has begun to improve, but the recovery will be weak. The upturn remains fragile, and risks are tilted to the downside. Uncertainty over the evolution of Russia’s war of aggression against Ukraine and its global impact remains a key concern.”

Traders only had eyes for stocks. The S&P 500 closed with a 0.24% gain with traders downplaying recession risks and S&P futures are unchanged today.

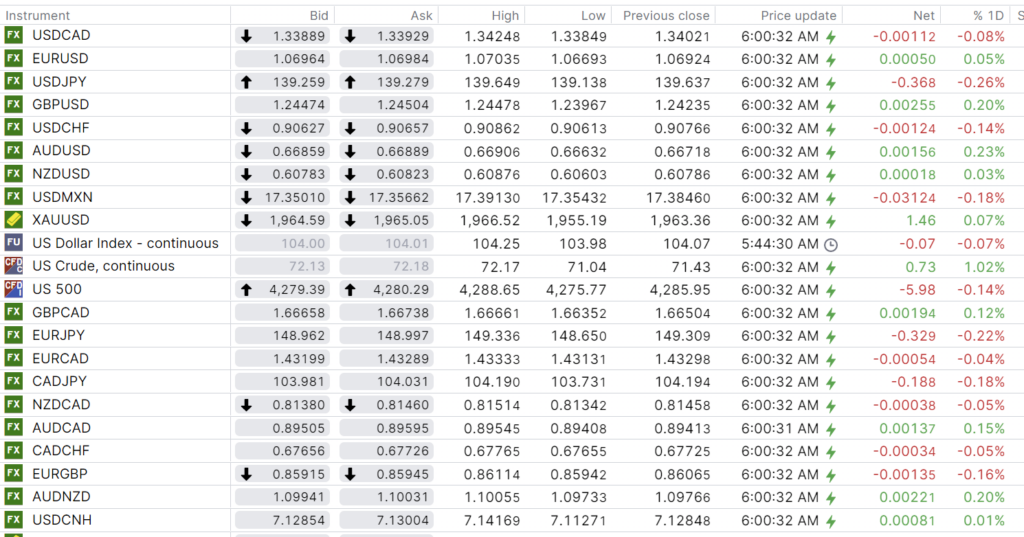

EURUSD is bouncing in a 1.0669-1.0722 band with prices below the peak in NY trading. The single currency is likely to remain in a 1.0650-1.0750 range until next week when German inflation the ZEW Survey and US CPI data are available.

GBPUSD rallied from 1.2397 to 1.2471 despite forecasts from some analysts suggesting the currency will be very weak in H2 because of a UK economic slowdown.

USDJPY dropped traded in a 139.14-1.3965 range with prices underpinned by slightly firmer US 10-year Treasury yields which are steady at 3.702%

AUDUSD traded in a 0.6663-0.6691 range. The bottom occurred after weak China trade data raised concerns about global growth from China’s stagnant post-pandemic economic recovery. Prices rallied after RBA Governor Philip Lowe warning that more rate hikes may be needed to counter rising inflation. The RBA raised rates to 4.10% yesterday and Goldman Sachs analysts predict rates will peak at 4.85%.

The US traded deficit widened to $74.6 billion in April (previous $60.6 b).

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

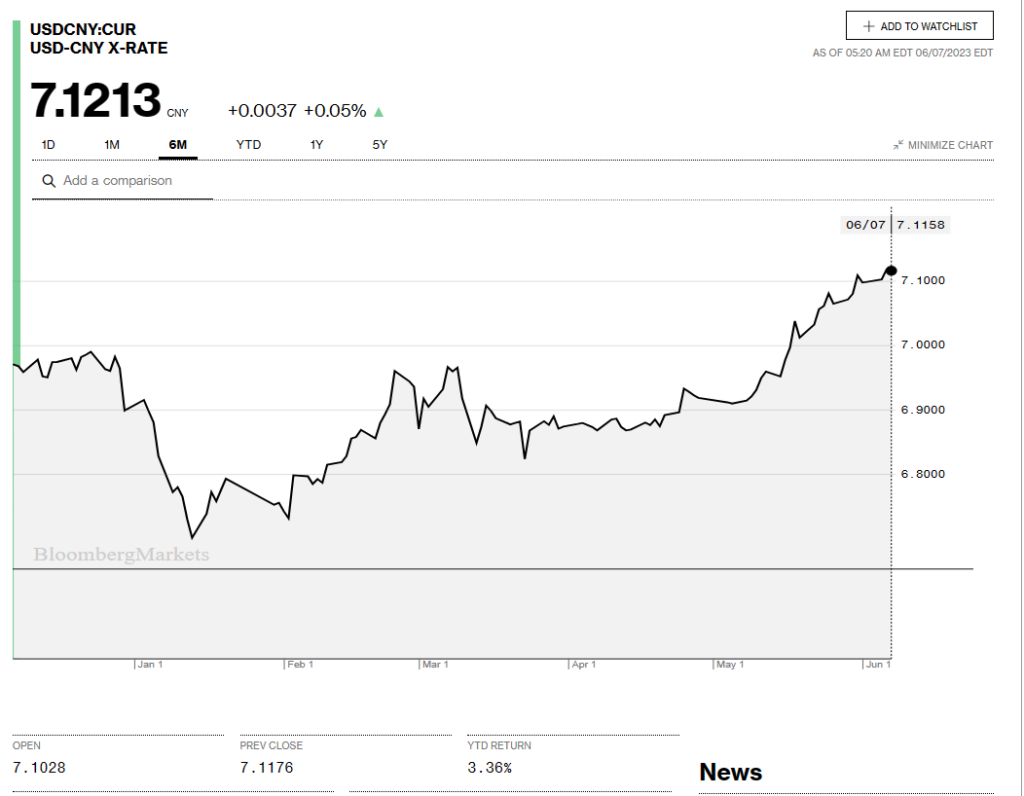

China Snapshot

Bank of China Fix: 7.1196, previous 7.1075.

Shanghai Shenzhen CSI 300 fell 0.49% to 3789.34.

China May Trade surplus shrinks to $65.81 billion from $90.21 billion with exports falling 7.5% y/y instead of -.04% as forecast.

Bloomberg reports that these four large Chinese banks, Industrial & Commercial Bank of China Ltd., Bank of China Ltd., Agricultural Bank of China Ltd. and China Construction Bank Corp., cut US dollar deposit rates.

Chart: USDCNY 6 month

Source: Bloomberg