May 2, 2024

- Markets are still mulling over the FOMC decision.

- Traders are unimpressed with BoJ intervention.

- US dollar is fairly subdued overnight but opens lower from yesterday.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3718, overnight range 1.3705-1.3743, close 1.3740.

USDCAD is dusting itself off after a wild and woolly session on Wednesday when it ping-ponged in a 1.3703-1.3784 range. The Fed failed to validate fears it would hike rates and instead suggests it would still ease in 2024. That was enough to squeeze US dollar bulls as evidenced by the US dollar index plunging from 106.38 yesterday to 105.45 overnight.

Bank of Canada Governor Tiff Macklem addressed the Senate Standing Committee on Banking, Commerce, and the Economy on May 1. He was pretty pleased with the inflation outlook saying, “we are getting closer. We are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained.” That leaves the door open to a June or July rate cut.

WTI oil prices fell to 79.03 from 81.42 yesterday partly because the Fed’s concern about stubborn inflation raised fears of a global economic slowdown. It didn’t help that the EIA reported US crude inventories rose by 7.265 million barrels last week.

Canada’s trade surplus is expected to increase to $1.5b from $1.39b.

USDCAD Technicals

The intraday USDCAD technicals are slightly bullish while trading above 1.3700, looking for a break above 1.3750 to extend gains to 1.3790. A move below 1.3700 suggests a test of the April uptrend line at 1.3650.

The month-long USDCAD uptrend above 1.3650, is guiding prices toward the two-week downtrend line at 1.3780. A topside break targets 1.3900 while a downside move suggests a retest of support at 1.3550.

For today, USDCAD support is at 1.3705 and 1.3670. Resistance is at 1.3760 and 1.3790. Today range is 1.3705-1.3780.

Chart: USDCAD 4 hour

Source: Investing.com

The Dance of the FOMC Fairy

The Fed pivoted in December, but the anticipated pirouette at the May 1 meeting failed to materialize. The Fed left rates unchanged at 5.25-5.50% as everyone expected. Prior to the meeting, Fed Chair Jerome Powell and his colleagues repeatedly told audiences that rate decisions were “data dependent.” The recent slate of US economic data, especially inflation readings, were higher than expected, and traders were positioned for a mildly hawkish FOMC outcome. It didn’t happen. Powell hit all the right notes and delivered a balanced but slightly dovish outlook.

The icing on the cake, at least for bond traders, was the announcement that because the Fed said it would slow down the pace that it reduces its securities holdings by cutting the monthly redemption cap on Treasury securities from $60 billion to $25 billion starting in June. Not quite quantitative easing, but close.

Canada’s trade surplus flipped to a trade deficit of $2.28b compared to expectations for an increase in the surplus top $1.5b from $1.49b

The First Move is the Wrong Move

The initial reaction was to buy stocks and bonds and sell US dollars. But that was probably just traders unwinding positions because the Fed was not as hawkish as the previous data suggested they would be. The proof is that by the end of the press conference, the US dollar started recouping some losses and 10-year Treasury yields were off its low. The S&P 500 finished the session down 0.34%.

FX markets were rather tame overnight with the US dollar consolidating its post-FOMC losses but above its worst levels. The exception was USDJPY which experienced another round of FX intervention.

OECD dons Rose-Coloured Glasses

The May OECD Economic Outlook says: There are signs that the global outlook has started to brighten, though growth remains modest. The impact of tighter monetary conditions continues, especially in housing and credit markets, but global activity is proving relatively resilient, inflation is falling faster than initially projected, and private sector confidence is improving. Global growth in 2023 continued at an annual rate above 3%, despite the drag exerted by tighter financial conditions and other adverse factors, including Russia’s war of aggression against Ukraine and the evolving conflict in the Middle East. Global GDP growth is projected at 3.1% in 2024 and 3.2% in 2025.

Data Doldrums

US weekly jobless claims rose just 208,000 last week, unchanged from the week before. The Challenger job cuts report showed that employers announced 64,789 cuts in April, a 28% decrease from the 90,309 cuts announced one month prior. The US trade deficit was little changed at $92.5b.

EURUSD

EURUSD jumped from 1.0672 to 1.0732 during the FOMC statement and Powell press conference then dropped to 1.0687 before closing at 1.0715. It chopped about in a 1.0696-1.0728 range overnight and is at the low in early NY. The single currency is getting a bit of support after Powell suggested rates should still be cut in 2024. German Manufacturing PMI was a tad better than expected at 45.3 compared to 44.9 in March.

GBPUSD

GBPUSD traded in a 1.2508-1.2545 range overnight and is sitting at 1.2512 in NY. The FOMC meeting saw GBPUSD swing between 1.2490 and 1.2550. Prices are being pressured by the OECD forecasting UK growth to be just 0.4% in 2024 making it the slowest growing G-7 economy.

USDJPY

USDJPY had a choppy session in the aftermath of the FOMC meeting. Right near the NY close, USDJPY plunged from 157.99 to 153.03 after the Bank of Japan reportedly spent $23.59 billion to buy yen and sell US dollars. Once again, BoJ officials admit nothing which is understandable since USDJPY has rallied back to 155.32 in NY. USDJPY is underpinned by the 10-year US Treasury yield which is steady at 4.61%.

AUDUSD and NZDUSD

AUDUSD traded in a 0.6515-0.6550 range and managed to hang on to most of its post-FOMC gains. Australian Building Permits and Trade data had little impact on FX.

NZDUSD traded firmer in a 0.5914-0.5948 range with direction determined by broad US dollar sentiment.

USDMXN

USDMXN is trading near the bottom of its overnight 16.9162-17.0185 range. Prices are on the defensive after Mr. Powell indicated that US interest rates would still be going lower this year.

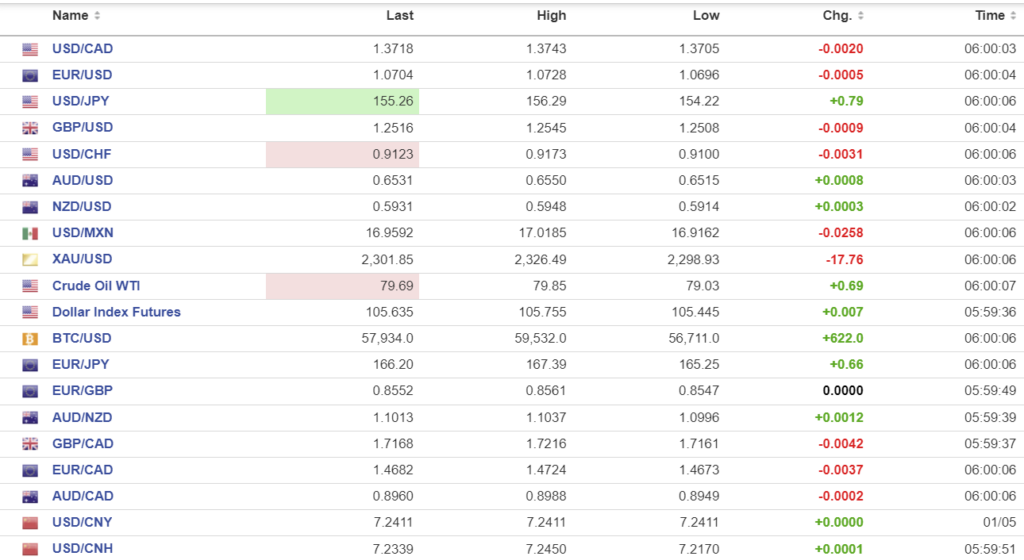

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot`

PBoC fix: 7.1063 (prev. 7.1066)

Chinese markets closed.

Shanghai Shenzhen CSI 300 fell 0.54% to 3604.39.

Chart: USDCNY and USDCNH 4 hour-as of April 30

Source: Investing.com