February 6, 2024

- BoC Governor Macklem speaks in Montreal at 10:00 am PT

- US data void may sideline traders.

- US dollar continues to consolidate recent gains.

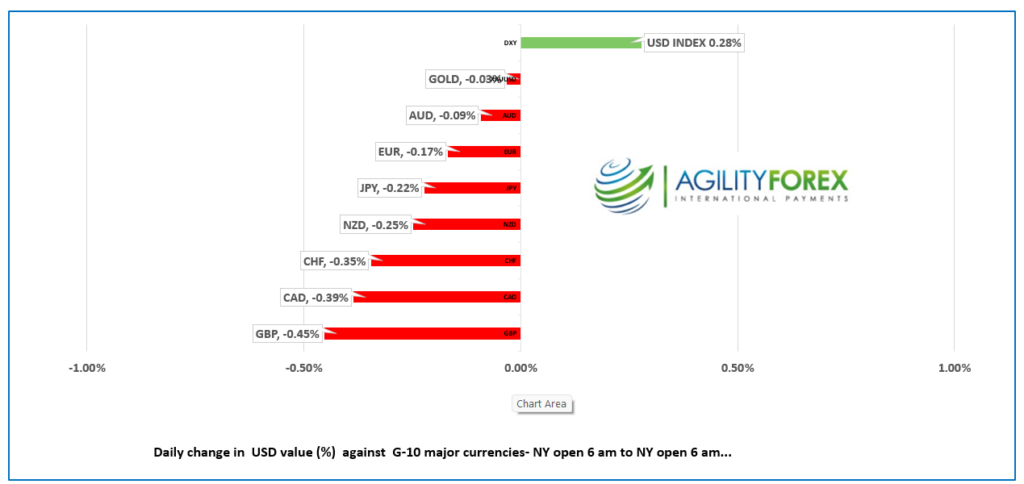

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3538-42, overnight range 1.3506-1.3544, close 1.3540.

USDCAD seesawed in a relatively narrow range, with the upside contained by strong resistance from previous highs and the 100-day moving average. Traders seem to have forgotten about last week’s BoC meeting and its implication that rates could go higher. They will hear more on that subject today when Governor Tiff Macklem speaks to the Montreal Council on Foreign Relations about “The effectiveness and the limitations of monetary policy.”

USDCAD direction is determined by US interest rate sentiment and the latest US data that suggested the US economy was booming, which precluded the need for rate cuts fueled the rally. However, despite the data, the Fed will not be raising rates in 2024 and still plans on at least 3 rate cuts. That suggests that the spike in Treasury yields, and the US dollar gains were due to profit preservation as weak positions were unwound or stopped out. Fading the moves looks like a winning strategy.

WTI oil prices are toing and froing in a $72.39-$73.38 range with US production gains and Chinese growth concerns offsetting Opec production cuts and risks of supply disruptions from Middle East tensions.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3510, looking for a break above the key 1.3540-60 pivot zone to extend gains to the 1.3900 area. A break below 1.3510 negates the upside pressure and shifts the focus to 1.3430 and 1.3360.

Bollinger Band studies suggest USDCAD is becoming overbought, and the 50% Fibonacci retracement of the November-December range is 1.3550. Both data points suggest limited upside without a fresh catalyst.

For today, USDCAD support is at 1.3510 and 1.3460. Resistance is at 1.3550 and 1.3590. Today’s range is 1.3490-1.3560

Chart: USDCAD monthly

Source: Daily FX

G-10 FX recap

Traders are continuing to feel the embarrassment from premature rate cut elation which has underpinned the US dollar since Friday’s nonfarm payrolls report and exacerbated by Fed Chair Powell’s 60 minutes interview. The view was reinforced again yesterday after the forecast-beating ISM Service data which suggested the US economy was still firing on all cylinders.

There are no US economic reports of note today, leaving traders to look elsewhere for inspiration. That came in the form of a sharp rally in Chinese stocks, mainly due to government intervention. The news lifted Hong Kong’s Hang Seng index by 4.04% and put European investors in a better mood. The UK FTSE 100 is leading the pack with a 0.50% gain. SP 500 futures are flat.

Traders will also get a dose of wisdom from Fed policymakers, Neal Kashkari, Loretta Mester, and Susan Collins.

EURUSD is going nowhere in a 1.0724-1.0762 band. The topside appears capped by negative technicals while prices are below the 1.0780 downtrend line and 100 day moving average zone. Eurozone December retail sales were worse than expected (actual -1.1% m/m, vs previous 0.3%)

GBPUSD is inching toward the to of its overnight 1.2525-1.2572 range and modestly supported by better than expected January Construction PMI data (actual 48.8, forecast 47.3, December 46.8). However gains may be limited after yesterday’s remarks by BoE Chief Economist Hu Pill who opined that the question for policymakers now is when to cut rates.

USDJPY is adrift in a 148.37-148.82 range partly because the US 10-year Treasury yield rally appears to have peaked at 4.17%. Japanese data did not have any lasting impact. Household spending fell 2.5% (forecast -2.1%) and total cash earnings rose 1.0% m/m.

AUDUSD traded calmly in a 0.6478-0.6522 range even with the RBA monetary policy decision. The central bank surprised no one when it left its overnight rate unchanged at 4.35%. The statement could be viewed as hawkish because it warned that “a further increase in interest rates cannot be ruled out.”

NZDUSD traded in a 0.6047-0.6078 range with New Zealand markets closed for the Waitangi Day holiday.

USDMXN traded cautiously in a 17.752-17.1324 range with price action mirroring US Fed rate sentiment. Mexico inflation is due Thursday and expected to rise to 4.88% y/y from 4.66% in December. Banxico also meets that day and is expected to leave rates unchanged.

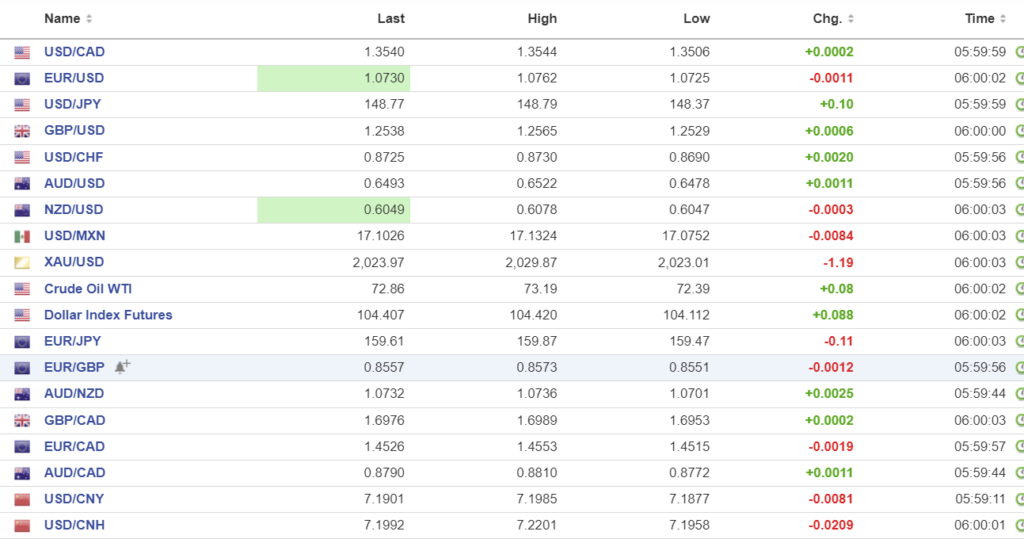

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1082, expected 7.2057, previous 7.1070

Shanghai Shenzhen CSI 300 rose 3.49% to 3311.69.

Beijing to the rescue. The surge in the CSI index is mainly due to state intervention and hope for more. Big funds that hold state owned funds reportedly bought ETFs against a backdrop of reports that Chinese regulators are to brief Xi Jinping on financial markets.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com