Photo: Bing AI

September 20, 2023

- Markets expect hawkish bias from FOMC.

- Economists predicting another BoC rate hike.

- US dollar rangebound but has a bid.

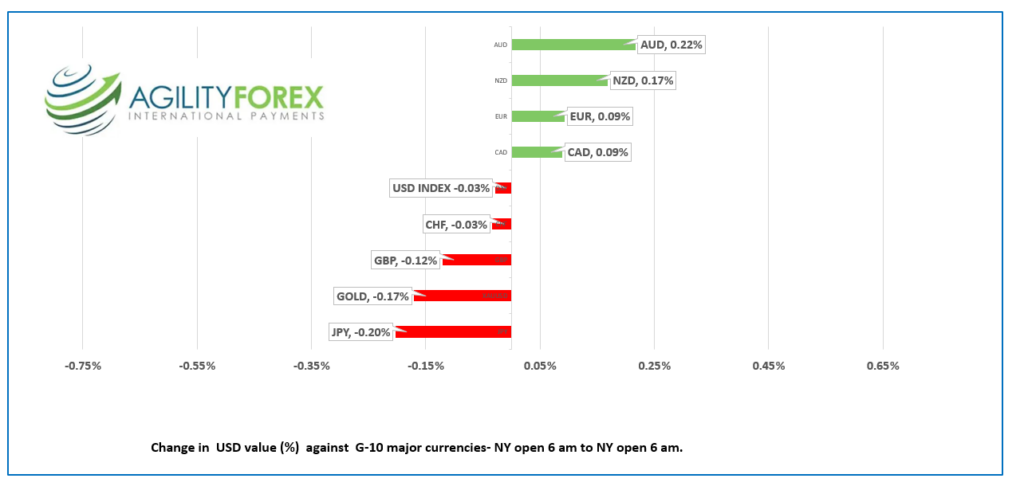

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3432-36, overnight range: 1.3431-1.3465, close 1.3449

USDCAD dropped to 1.3381 from 1.3442 following the hotter-than-expected Canadian inflation report yesterday (actual CPI 4.0% y/y vs. forecast 3.8%, July 3.3%). More importantly, the Bank of Canada’s preferred measures, CPI-Trim and CPI-median, rose on average to 4.0% from 3.8% in July.

The results have convinced JPMorgan economists that the BoC will hike rates to 5.25% in October. However, this isn’t the message the BoC wants consumers to hear. Deputy Governor Sharon Kozicki dismissed the CPI data, stating that “ups and downs” are not that unusual.

WTI oil prices retreated from yesterday’s peak of $91.62 and dropped to $88.97/b overnight before rebounding to $89.70/b in early NY.

USDCAD is expected to trade sideways until the FOMC meeting.

USDCAD Technicals

The intraday USDCAD technicals are bearish while trading below 1.3480. Yesterday’s breech of the 1.3430-40 support area is looking inconclusive after prices rallied back to 1.3465 and then closed at 1.3449. A “false-break will be confirmed on a rally above 1.3480, which would argue for more 1.3400-1.3600 consolidation.

The RSI studies show USDCAD remains oversold and vulnerable to a further correction.

For today, USDCAD support is at 1.3400 and 1.3360. Resistance is at 1.3460 and 1.3490. Today’s range 1.3390-1.3490

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

In 1980, Pat Benatar asked a former love interest, “Hit me with your best shot,” and today, traders are echoing a similar sentiment, urging the Federal Reserve to take its best shot. The Fed is widely expected to leave rates unchanged at today’s meeting, but the statement and the latest Summary of Economic Projections, which includes the “dot-plots,” will determine the Fed’s degree of hawkishness.

Analysts suggest that the dot-plot will reflect another rate hike in 2023 and in 2024, with no rate cuts until 2025. Place your bets—the window closes at 2:00 pm EDT. Asian equity indexes followed Wall Street’s lead and closed with losses. Japan’s Nikkei 225 dropped 0.66%, while Australia’s ASX 200 lost 0.465%. European bourses are trading positively after lower-than-expected UK inflation data lifted the FTSE 100 index by 0.74%. S&P 500 futures are 0.21% higher, gold is close to unchanged, and WTI is down 0.63%.

EURUSD drifted in a 1.0673-1.0718 range, supported by hopes that the Fed leaves rates unchanged. However, gains are limited by fears the statement, dot-plot forecast, and Powell’s press conference may be more hawkish than anticipated.

GBPUSD dropped to 1.2334 from 1.2398 after lower-than-expected inflation lowered the risk of another Bank of England rate hike. Headline CPI fell to 6.7% in August (July 6.8% y/y), while Core-CPI dropped to 6.2% from 6.9%. The Bank of England monetary policy meeting is tomorrow, and on the heels of the inflation data, money market traders cut the odds of a rate hike to 55% from 80% yesterday. Prices have recovered to 1.2365 in early NY.

USDJPY climbed to 148.17 from 147.69 due to fears that the Fed outlook is hawkish and because the US 10-year yield is trading at 4.34%.

AUDUSD traded narrowly in a 0.6448-0.6482 range, supported by higher commodity prices and yesterday’s hawkish RBA minutes.

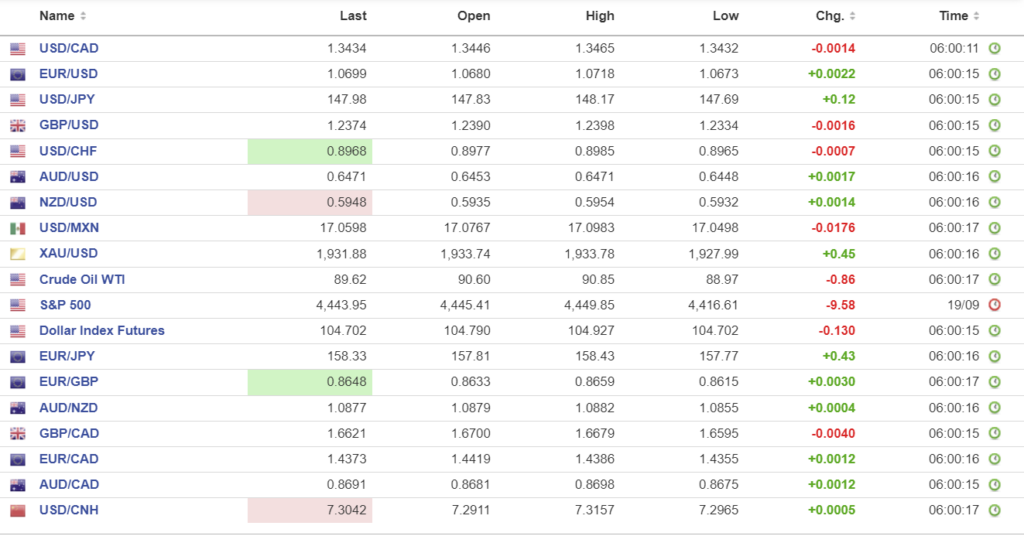

FX high, low, open

Source: Investing.com

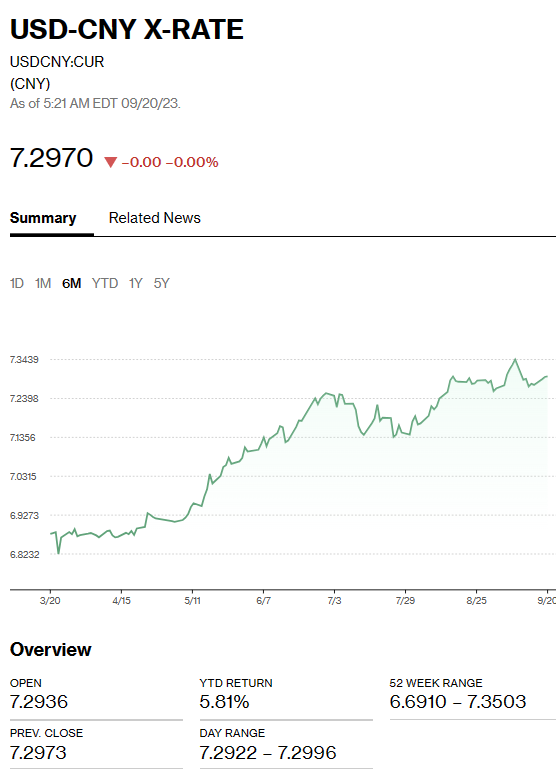

China Snapshot

Bank of China Fix: today 7.1732, expected 7.2926, previous 7.1733.

Shanghai Shenzhen CSI 300 fell 0.40% to 3705.69.

PboC economist Zhou Xiaochuan said they will pay more attention to yuan changes vs a basket of currencies and will resolutely correct one-side behaviour in the exchange rate.

Chart: USDCNY 1 month

Source: Bloomberg