Image by DALL-E

November 15, 2023

- US Retail Sales & PPI data support Fed cut hopes.

- S&P 500 futures add to gains.

- US dollar consolidating yesterday’s losses.

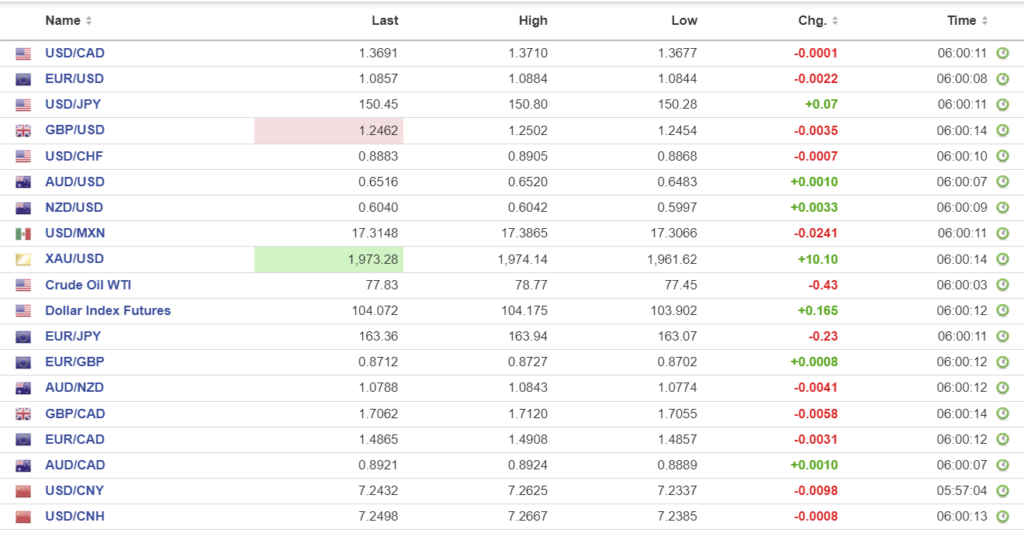

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3689-93, overnight range 1.3660-1.3710, close 1.3694

Yesterday, USDCAD dropped like Trudeau’s polling numbers when it was sideswiped by widespread US dollar selling in the aftermath of the lower than expected US inflation numbers. Bond traders wrapped their arms around the idea that not only have US interest rates peaked, the first cut of the easing cycle may occur as soon as May 2024. Treasury yields plunged, the greenback tanked, and equities soared.

Today’s US Retail Sales and Producer Price data did not cause the same kind of stir. The US dollar dipped but quickly reversed, however S&P Futures added to overnight gains while Treasury yields barely budged.

A modest rise in oil prices also weighed on USDCAD as WTI climbed to $78.77 before dropping to $77.44/b in NY trading today. The American Petroleum Institute reported by crude stocks rose by 1.33 million barrels last week which helped to slightly offset bullish sentiment after the International Energy Agency (IEA) predicted higher demand in 2024.

USDCAD direction continues to be a US dollar story and domestic data is largely irrelevant to price action.

Manufacturing Sales and Wholesale Sales rose 0.4% but were not a factor in USDCAD trading.

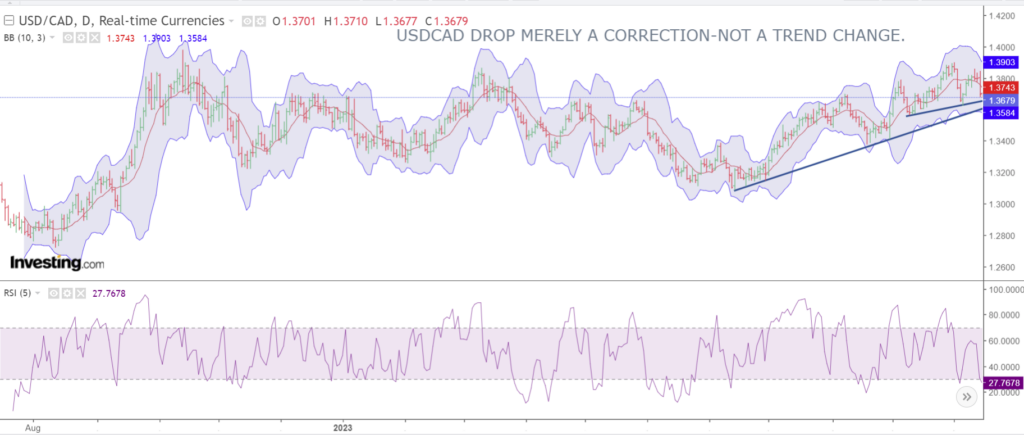

USDCAD Technicals:

The intraday technicals are bearish below 1.3705 (hourly chart) and looking for a break below 1.3670 to test minor support from this week’s rally which is at 1.3650. A break above 1.3705 puts 1.3760 in play.

Longer-term, yesterday’s sell-off is merely a correction. Bollinger band and RSI studies suggest USDCAD is oversold. The July uptrend line is intact above 1.3580, which is guarded by intraweek support at 1.3640.

For today, USDCAD support at 1.3660 and 1.3640. Resistance at 1.3705 and 1.3750. Today’s expected range is 1.3640-1.3740.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Yesterday, traders got an early “Black Friday” deal when US headline, core, and super-core inflation numbers were lower than expected. It may be far too early for the Fed to declare victory in the fight against inflation, but it didn’t stop bond traders from reacting like they did.

The US 10-year Treasury yield plunged from 4.63% to 4.41% by the end of Tuesday, before inching back to 4.460% in early NY trading. Bloomberg’s John Authers explained the move by pointing out the Bank of America fund manager survey suggested traders were just looking for an excuse to buy bonds, and the CPI data did the trick.

Equity traders were holding hands, dancing in a circle, and singing “ding dong, inflation is dead,” and scrambled to buy stocks. The NASDAQ led the charge and rose 2.37% while the S&P 500 gained 1.9%.

The US dollar plunged with the US dollar index (DXY) free-falling from 105.62 in Europe to 103.86 yesterday, then consolidating overnight in a 103.90-104.18 range

There won’t be a similar move today. Retail Sales fell 0.1% m/m in October (forecast -0.3) and the ex-auto’s component rose 0.1% (forecast unchanged). Also, the PPI index rose less than expected. Both reports support calls for the Fed to begin easing in May.

Meanwhile, US politicians are on a path to avoid shutting down the government next week after the House passed another stop-gap spending bill. President Biden and China’s Xi Jinping meet in San Francisco today, which is raising hopes that US/China relations will improve.

EURUSD rallied after the CPI data then consolidated the gains in a 1.044-1.0884 range overnight. Euro gains were limited by weak economic data. Euro area Industrial production fell 1.1% m/m and 6.9% y/y, with the yearly number the worst since June 2020 when Covid raged. The EURUSD technicals are bullish above 1.0680, looking for a break of 1.0890 to extend gains to 1.0950.

GBPUSD soared yesterday then traded in a 1.2454-1.2502 range overnight. UK Inflation rose just 4.6% y/y in October, down from 6.7% in September, which served to ease fears of further Bank of England rate hikes. The data supported the earlier Morgan Stanley prediction that the BoE will cut rates by 25 bps in May 2024. GBPUSD technicals are bullish above 1.2320, looking for a break above 1.2550 to target 1.2750.

USDJPY dropped in tandem with falling US Treasury yields and traded in a 150.28-150.80 range. Weaker than expected Japanese GDP data (Q3 -2.1% y/y vs forecast -0.6%).

AUDUSD is at the top of its 0.6483-0.6522 overnight range due to the improved risk sentiment following the US data and better than expected Chinese Retail Sales numbers

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1768, expected 7.2564, previous 7.1768.

Shanghai Shenzhen CSI 300 rose 0.70% to 3607.25.

October Retail Sales rose 7.6% y/y (forecast 7.0%, September 5.5%), Industrial Production rose 4.6% y/y vs 4.5% in September. Analysts say that despite the better than expected data, the underlying economy remains weak.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com