Source: HDclipartall.com

- US CPI rises 7.5% y/y in January, Core rises to 6.0%

- ECB downgrades growth forecast

- US dollar opens mixed, commodity bloc modestly higher

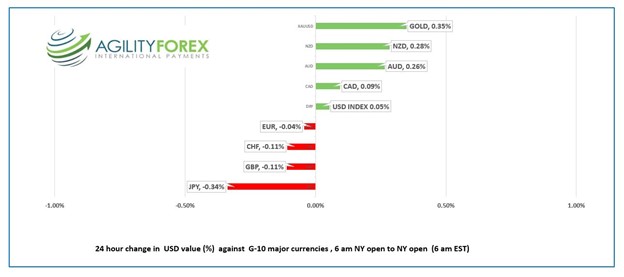

FX at a Glance

Source: IFXA Ltd/RP

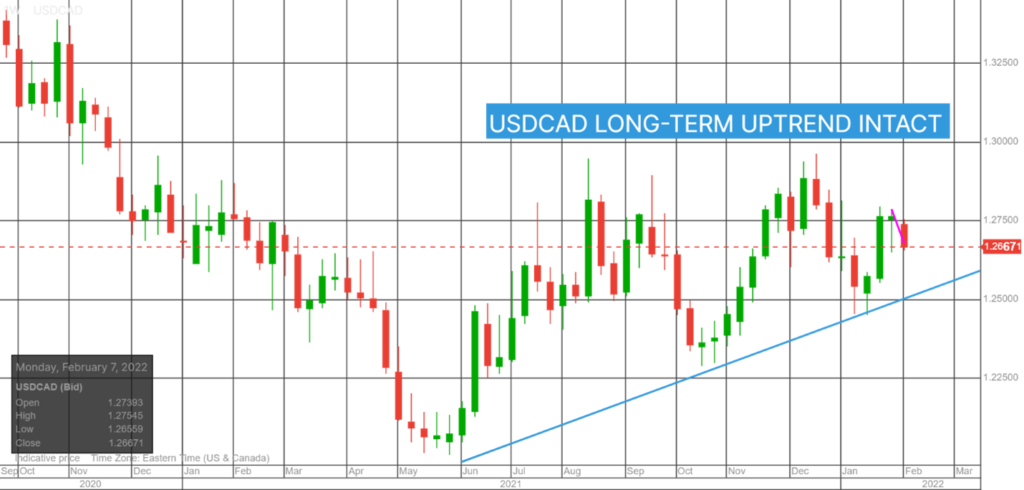

USDCAD Snapshot: Open 1.2672-76, Overnight Range-1.2667-1.2713, previous close 1.2673

USDCAD flat-lined overnight ahead of today’s US inflation report, trading in a narrow 1.2667-1.2685 range. Prices surged to 1.2713 after US headline and core CPI were higher than expected.

However, topside resistance is reinforced by steady to firm oil prices. WTI is trading at 90.60/barrel, above the overnight high but still below the Feb 4 peak of $93.05/b. Yesterday, the EIA reported US crude inventories declined 4.75 million barrels, however ongoing geopolitical tensions offset any negative sentiment. Oil traders still expect a post pandemic, resurgence in demand to propel prices above $100.00/b

USDCAD gains are also limited because the Bank of Canada is expected to match, and even outdo US rate hikes.

Technical view: The intraday USDCAD technicals snapped a minor downtrend when prices jumped to 1.2713 after the CPI report. The move suggests additional 1.2640-1.2790 consolidation. A break either side of that band suggests a test of 1.2500 or 1.3000. Longer term, the weekly chart shows the USDCAD uptrend is intact above 1.2500.

For today, USDCAD support is at 1.2660 and 1.2630. Resistance is at 1.2720 and 1.2760. Today’s Range 1.2660-1.2730

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FX markets traded quietly in an uneventful overnight session ahead of this morning’s US inflation data.

US inflation was hotter than expected, with monthly headline and core CPI rising 0.6% m/m. The annual rate of 7.5% y/y was last seen in 1982.

The results will empower those believing the Fed will be forced to act aggressively in March and raise rates 0.50%.

Other analysts suggest Fed officials will prefer to see more data before such a move. Cleveland Fed President Loretta Mester is one of them. Yesterday she said, “I don’t think there’s any compelling case to start with a 50-basis-point” rate increase.”

US weekly jobless claims were better than expected, falling 15,000 to 223,000 in the week ending February 4.

European bourses flipped from positive to negative after the US data. S&P 500 futures are down over 1.0% as the US 10-year Treasury yield jumped from 1.94% to 2.00%. WTI rallied while gold inched lower.

EURUSD traded defensively in a 1.1414-1.1446 range, then dropped to 1.1383 post-US CPI. The single currency is pressured by the ECB’s downward revisions to growth forecasts. The ECB predicts GDP will be 4.0% in 2022 compared to their 4.3% y/y forecast in November. They expect inflation to rise to 3.5% y/y (November forecast 2.2%). Even ECB policymakers are unimpressed with the forecasts. Bloomberg reports that several governors caution against depending too much on them as the actual results are far different from projections.

GBPUSD retreated from its 1.3579 peak and dropped to its overnight low of 1.3525. The prospect of more aggressive Fed contrasts with BoE Chief Economist Huw Pill cautioning against an “aggressive” approach to rates.

USDJPY spiked to 116.23 from an Asia low of 115.49 following the surge in the 10-year Treasury yield to 2.00%. News that the BoJ would buy “unlimited” JGB’s at 0.25% on February 14 to re-enforce their Yield Curve Control policy added to USDJPY demand.

AUDUSD and NZDUSD gave back overnight gains after the data.

Chart of the Day: USDJPY hourly

Source: Saxo Bank

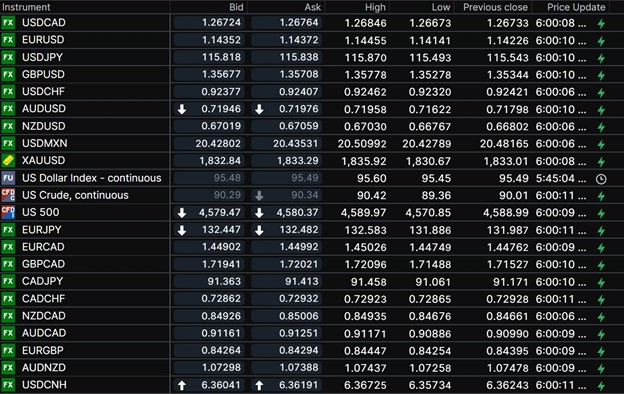

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

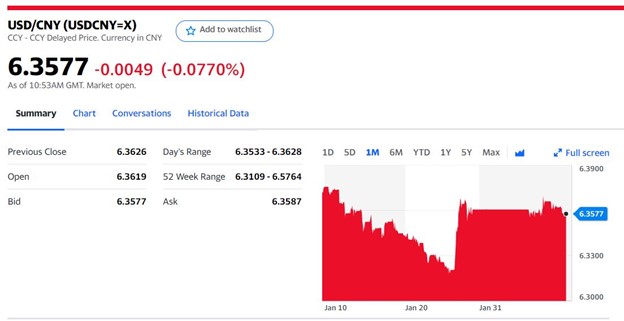

China Snapshot

Today’s Bank of China Fix 6.3599, previous 6.3653

Shanghai Shenzhen CSI 300 fell 0.26% to 4639.86

China market regulator setting sights on iron ore market, in attempt to ensure price stability

Chart: USDCNY one month

Source: Saxo Bank