Photo: HDClipartAll.com

January 12, 2023

- CPI fails to live up to the hype

- Trader’s betting on BoJ policy tweaks next week

- US dollar opens mixed-JPY soars

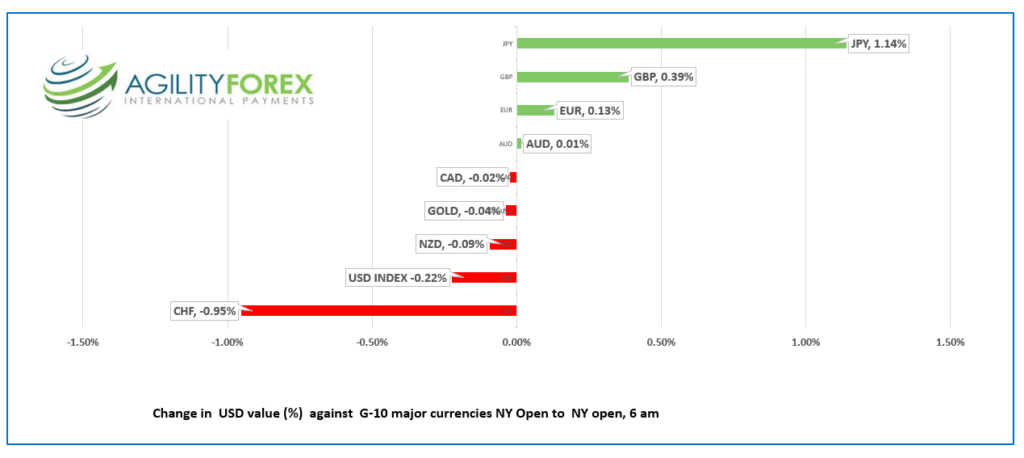

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3424-28, overnight range 1.3357-1.3447, close 1.3425

USDCAD slid following today’s CPI report which came in as forecast and is continuing to slide as this is being written.

USDCAD is closely tracking US dollar moves and general risk sentiment, while deriving a bit of additional support from higher crude prices. The perception that the BoC is more dovish than the Fed may be challenged after today’s CPI data which fueled speculation the Fed will only hike rates 25 bps on February 1.

WTI rallied from an Asia low of $74.33/b yesterday to $79.01/b post-CPI. Prices are supported by the weaker US dollar which offset negative sentiment after the EIA reported US crude stocks rose sharply, from -2.24 million barrels two weeks ago to 18..962 million barrels last week. Traders continue to expect sharply higher demand as the reopening of China’s economy gains traction.

USDCAD technical outlook.

The USDCAD technicals are bearish below 1.3650 (downtrend line from October) looking for a move below 1.3350 (uptrend line from June 2022) to extend losses and test the June 2022 uptrend line at 1.32401

For today, USDCAD support is at 1.3350 and 1.3310. Resistance is at 1.3450 and 1.3490.

Today’s range 1.3320-1.3420

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The highly anticipated US inflation report failed to deliver the drama that was expected. Headline and Core-CPI readings were lower than the November results, and exactly as forecast. Headline CPI rose 6.5% y/y, down from 7.1% y/y in November. Core-CPI rose 5.7% compared to 6.0% y/y previously.

It has been quite some time since markets have become this lathered up over a data point which means the reaction to day’s result should be volatile.

Markets were position for a weaker than expected result and when they didn’t get it, S&P 500 futures dropped 1.05%, and EURUSD plunged. Those moves didn’t last. S&P 500 futures are now 0.38% higher, and EURUSD has punched above 1.0800

The market is convinced the Fed will only hike rates by 25 bps on February 1.

European bourses are still in positive territory following the US data but are below their best levels The UK FTSE 100 index is up 0.66% and the German Dax has gained 0.33%. S&P 500 futures are close to unchanged.

EURUSD is bid, rising from a post-CPI low of 1.0731 to 1.0838 in NY. Prices are rallying due to the prospect of sharply higher ECB rates and hopes for a more dovish Fed.

ECB Consumer Inflation expectations over the next 12 months decreased from 5.4% to 5.0%, while expectations for inflation three years ahead edged down from 3.0% to 2.9%.

GBPUSD dropped to 1.2093 post-CPI then rebounded to 1.2239 as traders look ahead to a more dovish Fed.

USDJPY plunged from 132.48 to 130.82 overnight, due to rampant speculation that the BoJ will tighten again next week. Prices plunged further in the wake of the US inflation data and are testing support in the 129.50 area.

AUDUSD jumped to 0.6982 from a post-CPI low of 0.6878 as traders upgraded the odds that the Fed will pause rate hikes sooner than expected.

US weekly jobless claims fell 10,000 to 205,000

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

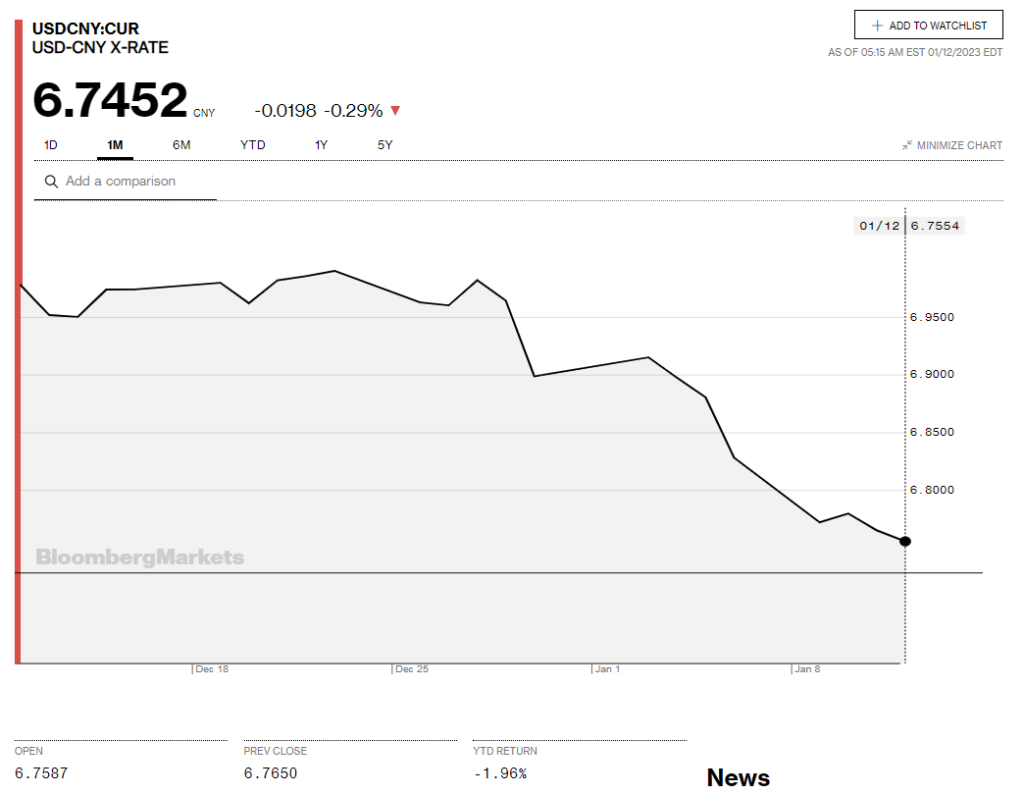

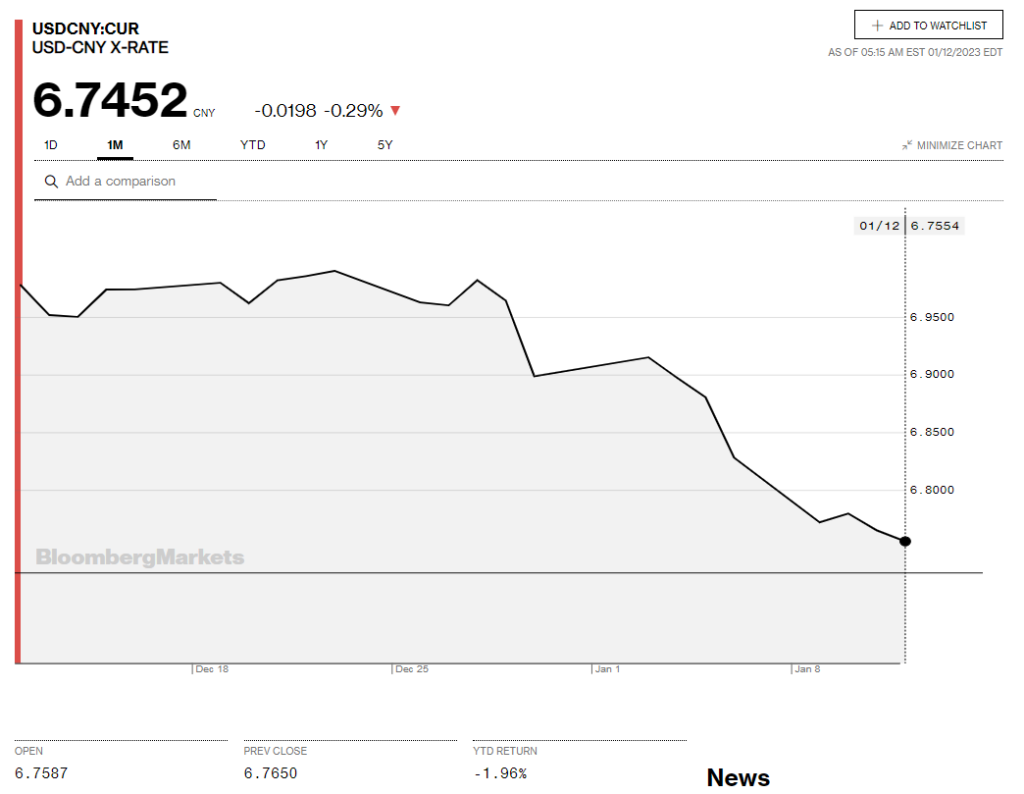

China Snapshot

Today’s Bank of China Fix: 6.7680, previous 6.7756

Shanghai Shenzhen CSI 300 rose 0.20% to 4017.87

December CPI 1.8% y/y, as expected, December PPI -0.7%y/y (forecast -0.1% y/y)

Reuters poll forecast GDP at 4.9% in 2023 (October forecast 5.0%), CPI at 2.3%

PboC expected to cut Loan Prime Rate by 5 bps in Q1

Chart: USDCNY one month

Source: Bloomberg